Private credit offers distinct advantages and appeal in a low return environment, but investors should be aware that behind the name is a diverse array of strategies, some more familiar to institutional investors than others, each with idiosyncratic risks. The diverse strategies that fall under private credit can be implemented with different orientations, preferences, and biases, complicating comparisons and requiring thorough and expert diligence.

The proliferation of private credit managers offers investors new ways to generate returns ranging from the mid-single digits to more than 20%, but assessing the return target of a prospective credit strategy is not enough—investors must examine the nature of the investing activity generating those returns. To assess these opportunities, targeted return, risk, and liquidity (including current yield, which, we believe, is a form of limited liquidity) are the three most important considerations. Investors need to decide whether

they want to prioritize minimizing risk or maximizing return, as private credit strategies offer the opportunity to achieve either objective with differing degrees of liquidity.

In this report, we describe the broad array of private credit strategies and position them along the risk/return spectrum, review the investment process, discuss expectations for the performance of these strategies in various parts of the economic cycle, and highlight some key risks for investors to consider.

Defining Private Credit

Broadly defined, a private credit fund targets the ownership of higher yielding corporate, physical (excluding real estate), or financial assets held within a private “lock-up” fund partnership structure. Credit exposure can be either corporate (repayment comes from cash flows generated by an operating company) or asset (repayment comes from cash flows generated by a physical or esoteric asset).

Strategies included under the private credit umbrella can generally be categorized as either “capital preservation” or “return maximization.” Capital preservation strategies, like traditional sponsor-focused mezzanine and senior debt funds, seek to deliver predictable returns while protecting against losses. These portfolios tend to be negatively skewed, with few losses and even fewer unexpected gains. Return-maximizing strategies include distressed corporate credit funds and funds that focus on capital appreciation. These funds offer the prospect of larger gains and often have normally distributed to positively skewed portfolios.

Strategies that don’t easily fall into one of these categories are either opportunistic (investing across the credit spectrum as market opportunities permit) or niche/specialty finance strategies, like aviation finance or health care royalties. Opportunistic and specialty finance strategies must be evaluated individually to determine the appropriate expectations for risk and return.

Figure 1 illustrates how private credit compares to more liquid credit strategies and other private investment opportunities, with targeted investment-level gross returns for select private credit strategies broken out.

FIGURE 1 RETURN SPECTRUM: PRIVATE CREDIT VS LIQUID CREDIT AND PRIVATE EQUITY STRATEGIES

Source: Cambridge Associates LLC.

Note: Returns for investment-grade and high-yield bonds represent arithmetic return assumptions in equilibrium.

Given the various strategies, private credit can reside in different parts of investor portfolios. Strategies with greater expected upside, like distressed credit or capital appreciation, might be found in private equity allocations. Strategies expected to return slightly less, like credit opportunities or traditional mezzanine, may sit in “special situations” or “opportunistic” buckets. The lower-yielding strategies, like senior debt, may sit in fixed income or alternative credit. Interestingly, senior debt allocations are increasingly being defined as an independent, standalone asset class in many portfolios. In short, private credit strategies can be used to enhance or diversify traditional allocations such as fixed income or private equity. At the same time, private credit can be an excellent standalone allocation in a portfolio because its different strategies offer a range of risks and returns broader than some other private asset classes.

Capital Preservation Strategies

Capital preservation strategies include sponsor-oriented mezzanine funds and senior debt. The vast majority of managers in this space finance private equity–led leveraged buyouts and exhibit a client service posture, emphasizing the cultivation of personal relationships as a means of differentiation. Returns flow primarily from current pay coupons and some fees; equity participation is a less important driver of returns. Loss mitigation is absolutely essential as the possibility of outsized gains is limited.

Mezzanine

“Traditional” mezzanine refers to those managers that seek to develop relationships with private equity sponsors and senior lenders to provide junior capital to finance buyouts or acquisitions. Mezzanine managers tend to make subordinated loans to lower-middle-market and upper-middle-market borrowers and generate most of their return from current cash pay coupons in excess of 10%. These funds also generate returns from prepayment penalties and paid-in-kind (PIK) interest, although to a much lesser extent than funds pursuing capital appreciation strategies. Mezzanine managers can also capture equity exposure through purchased equity or warrants, as well as penny warrants. Their ability to negotiate documentation is constrained by the demands of equity owners and senior lenders, and pricing frequently takes a strong cue from the market.

A primary risk for these managers is that credit losses overwhelm gains from equity exposures. In theory, equity gains from the rest of the portfolio should compensate the investor for limited credit losses, but this is not always the case. Targeted gross returns hover around the mid- to upper-teens, depending on market conditions. Mezzanine funds usually have eight- to ten-year lock-up periods with limited liquidity from current pay interest.

Senior Debt

Senior debt funds, commonly referred to as direct lenders, are most closely related to traditional mezzanine lenders in their investment approach. The vast majority of these managers pursue a sponsor coverage model, developing relationships with private equity managers to finance their buyouts and platform company expansions. They generate most of their returns from current cash pay coupons composed of a fixed credit spread and a fixed reference rate (usually Libor).

Although senior debt funds take senior risk, investors should be careful to closely identify the true risk of the underlying loans. For example, some senior lenders refer to second-lien loans as “senior” because they enjoy priority over all but first-lien lenders. Similarly, a split-lien loan secured only by a priority pledge of intellectual property may be a second lien in disguise if another lender to the same borrower has secured working capital, fixed assets, and machinery and equipment. Further, the advent of the unitranche loan enables lenders to remain the senior lender of record while retaining only a last-out tranche of the original instrument after selling a first-out piece to another lender. Thus, an investment described as “senior” may be riskier than it sounds.

Senior debt funds can be levered or unlevered at the fund level, and investors should focus on the overall level of leverage and the use of synthetic leverage, as well as the permanence and potential manipulation of leverage lines. Unlevered gross returns tend to be around 6% to 10%; levered gross returns may reach 15%. Risks confronting direct lenders include underlying portfolio credit risk as well as the risks attending any sponsor-oriented business model. These may include reliance on a limited number of sponsors and on the merger & acquisition (M&A) cycle generally, as well as general competition that first (often surreptitiously) erodes terms and, ultimately, depresses yields.

Return-Maximizing Strategies

Return-maximizing credit strategies seek to generate more private equity–like returns through purchasing either performing or distressed credit instruments. Distressed credit investors and their strategy of buying discounted loans or bonds in the hope of a par refinancing or a return-enhancing negotiated settlement are very familiar to many institutional investors. Perhaps less familiar are certain types of subordinated debt and preferred equity strategies that seek capital appreciation and that provide an alternative to dilutive private equity. Business owners seeking liquidity to grow or plan succession may wish to retain control of their companies—a wish many control-oriented private equity funds would be unwilling to grant. Return-maximizing strategies provide the desired liquidity without acquiring control of the business through instruments crafted to protect the lender.

Capital Appreciation Strategies

Capital appreciation strategies tend to be either par debt or equity-like instruments that frequently function as a replacement for private equity. Firms owned by entrepreneurs or families seeking capital but reluctant to surrender control will turn to structured equity or subordinated capital appreciation providers to meet their financing needs. Originating these types of investments is not easy and requires a broad network of professional services advisors and others that can help identify family-owned businesses, fund-less sponsors, and others seeking to grow their companies without private equity. These investors must exhibit great creativity in structuring bespoke instruments that meet the specific needs of each borrower.

These managers typically originate direct investments to unsponsored, lower-middle-market companies. Instruments are usually subordinated debt or preferred equity, which neither threaten senior creditors nor dilute common equity. In the capital structure, they fit comfortably between ownership and senior lenders to provide growth or acquisition capital to owners willing to pay a high coupon to avoid dilution. Capital appreciation managers may exhibit a preference for either debt- or equity-like exposures, but most will have some of both.

Debt-like instruments frequently retain more muscular creditor rights than structured equity in the form of covenants, liens, and other measures. The differentiating attribute of this strategy is its relatively higher reliance on high coupons to de-risk and generate return. Asset-level returns should be slightly below those of equity-like strategies but greater than traditional mezzanine. On the other hand, equity-like instruments frequently have a range of coupons, fees, and equity-like components. It is not uncommon to see these managers derive much of their returns from liquidation preferences, PIK interest, success fees, repayment penalties, and similar terms and conditions.

One risk of these strategies is the dispersion of outcomes. Expected gross returns should bottom out in the mid-teens, while the upside can reach into the twenties; liquidity is also low, with fund lives ranging from eight to ten years. Current yield depends on the individual manager’s preference. Together with distressed credit managers, capital appreciation managers’ risks, returns, and liquidity, especially at the riskier end of the spectrum, most closely resemble those of private equity; as a result, these riskier strategies can often be found in either the private equity or private credit allocations within investors’ portfolios.

Distressed Credit

Distressed corporate credit managers typically target middle- to large-capitalization companies and purchase deeply discounted debt securities, either in the market or bilaterally. What they do with these securities helps differentiate managers. Most endeavor to generate returns through negotiation, using whatever leverage is afforded them as creditors under the governing document and the prevailing bankruptcy code. A minority tend to be “pull-to-par” investors, basing returns on their view of a company’s fundamental valuation. These investors rely on catalysts such as an upcoming refinancing or a change in economic prospects to improve asset prices. “Negotiator” investors tend to create their own catalysts through restructurings or tailored financings to extract value.

Distressed credit managers are expert financial analysts with deep expertise in legal documentation. Their returns come from the accurate assessment of borrower enterprise value; a creative and co-operative approach to form coaliltions, obtain consensus, and craft constructive outcomes; and a thorough understanding of their rights and remedies enshrined in the relevant documentation. Returns are frequently generated through a combination of a very high current contractual yield component relative to par strategies (because instruments are purchased at a discount) and capital gain (driven by a “pull-to-par” from refinancing or settlement). Targeted gross internal rates of return (IRRs) typically exceed the mid-teens.

The primary risk attending these strategies lies in the many parties involved in a restructuring. Investments can pay off handsomely if negotiations go as planned. Alternatively, they can quickly underperform if other creditors, company management, ownership, or even a local bankruptcy court judge becomes uncooperative—soft power and personalities matter. Liquidity can vary, and some managers pursue very similar distressed strategies through liquid hedge funds as well as lock-up vehicles.

Opportunistic and Niche Strategies

Beyond the strategies that can be more easily classified as either generating returns or protecting capital lie a wide array of other credit strategies that would need to be evaluated individually to determine whether they are more oriented toward return maximization, capital preservation, or a mix of both. Under very broad headings, investors may find funds that could be called “credit opportunities” or “specialty finance.”

Credit Opportunities

This strategy seeks to deploy debt capital opportunistically wherever market liquidity is lowest or value is greatest. It can include rescue financings (which help borrowers stave off a liquidity crisis, upcoming maturity, etc.), specialty lending, regular-way credit in hung syndications, and distressed credit. Frequently, the most attractive opportunities for this strategy arise at the beginning of a distressed cycle, making these managers first cousins of distressed credit managers.

Moreover, credit opportunities funds differ from distressed funds in their ability to source, structure, manage, and exit par instruments across a broad array of industries and markets. It would not be surprising to find capital appreciation specialty finance, structured equity, or even senior debt in a credit opportunities portfolio. One might even conclude that the breadth of mandate is the defining attribute of a credit opportunities manager. However, mandate breadth varies. Credit opportunities funds can focus on corporate credit, or only middle market, etc.

The chief risk for narrower-mandate managers is that their target niche may attract increased attention, encounter a decreased opportunity set, or both. Broader-mandate managers, on the other hand, are at risk of miscalculating the risk of a new and unfamiliar opportunity. Targeted gross IRRs typically exceed the mid-teens and vehicles tend to be locked up to afford the time to identify, execute, and exit illiquid opportunities.

Specialty Finance

Specialty finance managers pursue a very broad array of niche strategies. These managers tend to target one small industry, requiring highly specialized expertise. Within this category, the most capital has flowed to funds that purchase nonperforming loans (NPLs). More recently, pharmaceutical and music royalties, rediscount lenders, and funds specializing in life settlements, catastrophe bonds, and trade finance have come to market.

The highly specialized nature of these strategies makes them among the most difficult to perform due diligence on because each strategy requires unique lines of inquiry. Is a music royalty manager purchasing publishing rights, songwriter rights, or both? Is a pharmaceutical royalty manager purchasing the rights to a drug, or lending to a company but taking those rights as collateral?

Targeted gross returns for this fund type tend to begin in the mid-single digits and can range into the upper-teens and higher, but most strategies generally offer less upside potential. Fund structures also tend to be longer term and locked up. Yet of all private credit strategies, specialty finance holds some of the most liquid sub-strategies. We have encountered rediscount lenders and consumer finance strategies with two-year investment periods and five-year fund lives with no recycling of interest.

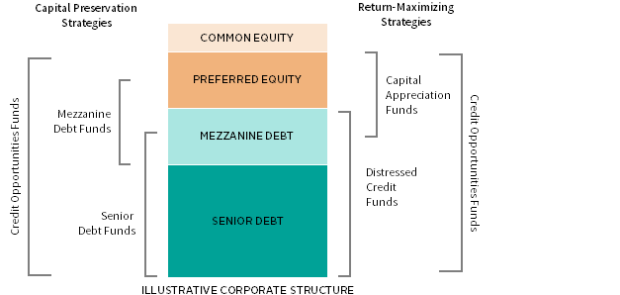

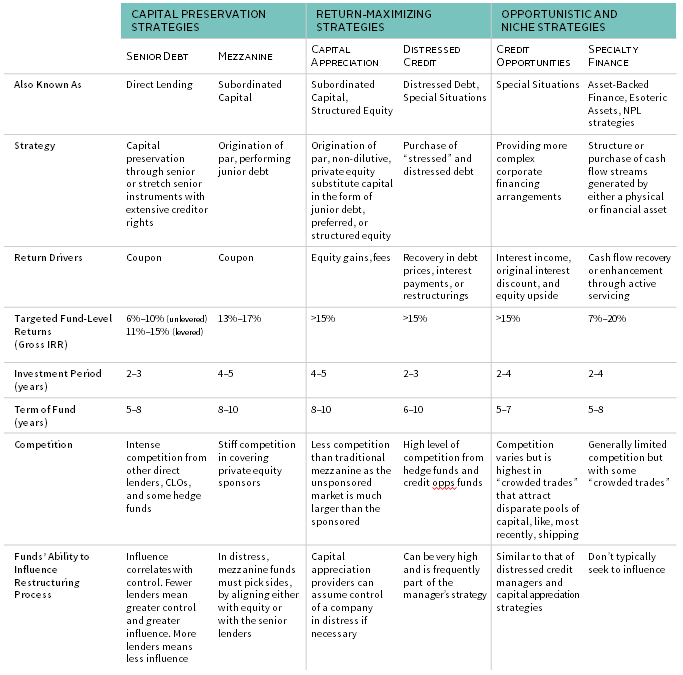

To summarize all the strategies we’ve discussed, Figure 2 shows where in the capital stack funds tend to invest, and Figure 3 outlines key characteristics of each strategy.

FIGURE 2 WHERE PRIVATE CREDIT STRATEGIES TYPICALLY PLAY IN THE CAPITAL STACK

FIGURE 3 CHARACTERISTICS OF PRIVATE CREDIT STRATEGIES

Source: Cambridge Associates LLC.

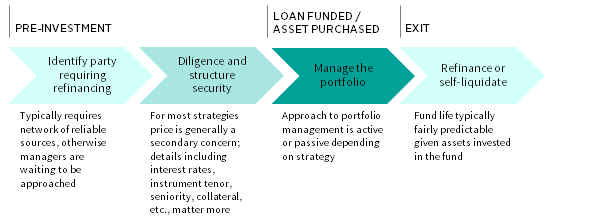

Investment Process

We show a simplified version of the investment process in Figure 4, as private credit managers’ investment processes depend entirely on the type of strategy. Though the initial stages are similar, they begin to diverge after the funding of a loan or the purchase of an asset.

FIGURE 4 SIMPLIFIED ILLUSTRATION OF PRIVATE CREDIT INVESTMENT PROCESS

Source: Cambridge Associates LLC.

All private credit managers, except distressed credit managers,[1]Distressed managers tend to seek out assets first, and then their holders. first identify the party requiring financing. The vast majority of private credit managers cannot identify specific opportunities a priori, but must instead await asset holders (future borrowers or sellers) to approach them. Unlike distressed credit investors, whose investable universe is usually published on Bloomberg, other private credit managers must be more active in their sourcing. This usually requires maintaining a network of reliable sources of financing opportunities through frequent personal interaction and constant contact. Whether a manager is looking for a borrower, a hung syndication, or a pool of NPLs, the first step is to identify the private equity fund, the syndication agent, or the seller of the NPLs.

Private credit managers then enter a due diligence phase during which they evaluate the risks attending their financing. This phase also includes the structuring of the security. In contrast to the typical private equity fund that buys common shares and therefore focuses the majority of its discussions on price, many private credit managers must consider such details as cash or PIK interest rates, instrument tenor, seniority, collateral, advance rates, amortization, covenants, and so on. At the same time, some private credit strategies fret most about price. These include distressed credit managers, NPL purchasers, and royalty stream purchasers.

Once the loan is funded or the asset purchased, the process begins to diverge even more dramatically. Mezzanine managers and senior debt managers hope to take a passive approach to portfolio management as only troubled borrowers require frequent attention. Distressed credit managers specializing in negotiated solutions embark on a series of long discussions with other lenders and company management to arrive at a profitable outcome. NPL managers employ their own or third-party servicers that execute the mundane task of calling delinquent debtors directly to negotiate a new payment plan or asset sale. Some royalty managers even have teams of marketing professionals tasked with placing songs whose rights the fund owns in new movies, television commercials, and other media to increase the revenue stream.

After this divergence in portfolio management, the processes reunite in the typical exits for private credit managers: refinance or self-liquidate. Virtually all of the strategies we have described will be exposed to assets that have either a finite life or a clear stream of cash flows that should predictably recoup principal and generate return. A healthy loan has a maturity date and coupon payments, an NPL pool will have negotiated payments, and royalties have statistically predictable streams. This feature differentiates private credit from other private alternative strategies.

Expectations for Strategy Performance in the Economic Cycle

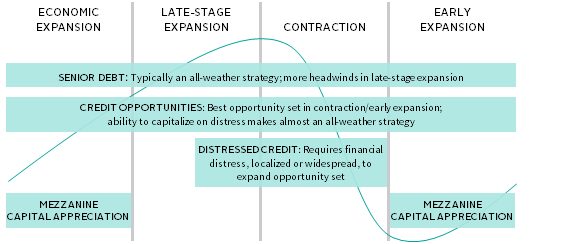

No analysis of private credit strategies would be complete without a reference to the economic cycle (summarized in Figure 5). The strategy most sensitive to the economic cycle is distressed credit because it requires an increase in financial distress, either localized or widespread, to expand the opportunity set. Similarly, credit opportunities managers that frequently allocate to distressed assets are also well served during a credit crunch. Their broader mandate, however, makes them less sensitive to the cycle than their cousins in the distressed space.

FIGURE 5 PRIVATE CREDIT STRATEGIES ACROSS THE ECONOMIC CYCLE

Source: Cambridge Associates LLC.

Notes: Illustration does not take into account relative value across credit, or relative value between credit and other asset classes. Specialty finance strategies will have different experiences during the credit cycle depending on the type of asset in which they are invested. Committing to draw-down strategies requires a longer investment horizon than investing in open-ended strategies that allow for immediate capital deployment and regular liquidity.

When distressed managers are most excited, mezzanine managers will probably be very worried. Rising defaults, higher leverage, and the economic malaise that set distressed managers’ pulses racing usually spell bad news for holders of junior, unsecured obligations issued at par. Moreover, their loans tend to have fixed coupons, creating pain in a rising rate environment. Similarly, equity-style gains targeted by capital appreciation managers can come under pressure during a cyclical downturn. However, those with sufficient dry powder at the beginning of a cycle can invest profitably by providing liquidity to struggling companies or even growth capital in the very early stages of a recovery when lenders are still rationing capital.

Senior debt funds are not immune to a downturn in the economic cycle. However, they are likely to be less worried than the mezzanine lenders that sit below them in the capital structure, if only because those managers will take the first loss after equity is compromised. But beyond that, senior lenders have (or should have) prudent structures and the benevolent hand of the US bankruptcy code behind them to support their recovery efforts. Moreover, their loans are usually floating rate, insulating them in a rising rate environment. Their ability to protect the downside makes them the closest to an all-weather strategy in corporate credit. Credit opportunities funds come in a close second, not because of their ability to mitigate losses, but because of their ability to capitalize on distress.

Specialty finance managers’ performance in the cycle depends entirely on the strategy. Purchasers of consumer debt are likely to suffer during widespread, rising unemployment. But unless the economic cycle changes music tastes or the need for certain drugs, music and health care royalty managers are unlikely to experience a change in cash flows.

Risks

Investors should consider the business risks of different private credit strategies, many of which we discussed earlier. Looking across these strategies, some act less like traditional investors and more like structured vehicles or finance companies. For example, a fund specializing in credit card receivables carries a unique regulatory risk surrounding the collection of those receivables. Further, some consumer finance fund managers are now buying not just financial assets but call centers, rate cards, and other appurtenances that make them look more like leasing or integrated operating companies than traditional investment funds. Of the many risks to consider, we highlight three: scale, leverage, and jurisdiction.

Scale

Strategies like senior debt and some niche/specialty funds tend to scale at a faster rate than traditional private equity funds. Scale requires formalized processes, clear reporting lines, and internal checks and balances that are not as imperative for a typical private equity fund with perhaps a few hundred million dollars in assets under management (AUM) and a handful of professionals executing one or two deals a year.

Scale is most commonly driven either by the need for diversification or high fixed costs. Senior debt lenders face asymmetric returns and so prioritize diversification, which is best achieved through greater AUM. More AUM, in turn, requires organization and specialization. In contrast, certain specialty finance strategies require highly specialized, costly capabilities. Consider purchasers of European or Asian real estate NPLs that need sophisticated servicing, legal counsel with expertise in different jurisdictions, native language speakers, real estate experts, and more. These forms of incremental overhead require either economies of scale or an above-market management fee. The impetus toward scale is evident: building on our two previous examples, the European real estate NPL market is dominated by a handful of fund managers, and most people familiar with the US senior debt space can name the largest players.

Investors should therefore consider scale when evaluating a credit strategy. Small distressed credit and capital appreciation managers can succeed handsomely. Similarly, senior debt funds that focus on unsponsored originations are naturally limited in achieving scale because of the accessibility of their opportunity set. However, managers pursuing scale must institute a more formal and expansive organizational and operational infrastructure that addresses factors such as reporting, managerial talent, growth, and employee retention, which should all be added to an investor’s

diligence list.

Leverage

Leverage is another operating risk that investors must analyze. Although subscription lines to bridge capital calls have been around for years, some managers now use them to enhance fund returns. More permanent fund-level leverage tends to be used primarily by senior debt funds originating predominantly senior, secured loans, as few leverage providers have the willingness to finance subordinated, uncollateralized loans (and certainly not at a reasonable borrowing rate to the fund manager).

Leverage is a very effective tool to turn a loan with an 8% current pay coupon into a 14% yielding asset. As a result, virtually every senior debt fund currently in the market offers a levered option, with many eschewing unlevered portfolios altogether. Although the performance of private credit funds’ assets in a downturn causes handwringing in the investor community, the other side of the balance sheet may hold ominous auguries. The challenge with assessing the risk of leverage lies in its permanence. Leverage that can be pulled quickly and at the leveraged lender’s discretion can lead to the forced sale of fund assets or the calling of capital to refinance the lender.

Jurisdiction

Because credit investing, almost by definition, relies to some extent on creditor rights, the prevailing legal framework providing these rights can be extremely important. Moreover, not all jurisdictions are equally favorable for creditors. Investors tend to agree that Australia, Canada, Sweden, the United Kingdom, and the United States offer some of the most powerful protections for creditors. At the same time, less favorable jurisdictions, notably in the emerging markets, should not be avoided altogether. In fact, some fund managers have grown adept at working within seemingly less favorable jurisdictions through creative structuring, greater selectivity, and more consensual workouts.

Conclusion

Private credit is a big tent that offers investors various options for preserving capital, generating current yield, or benefiting from capital appreciation. Private credit strategies can range in size and scale from niche specialty finance managers investing in royalties raising $400 million funds all the way up to senior debt managers that typically target corporate borrowers with $40 million to $200 million in EBITDA and raise funds as large as several billion dollars.

When building private credit portfolios, investors must balance their risk tolerance with their return objectives and current pay requirements. Arriving at an optimal allocation requires consideration of the context of the entire portfolio’s allocation to broader alternative and traditional long-only assets.

Tod Trabocco, Managing Director

Other contributors to this report include Rich Carson, Walter Murphy, and Anne Richardson.

Footnotes