New Zealand’s economy is well positioned compared to other major economies, and especially relative to Australia, but external factors will likely impact the local economy and markets

- New Zealand equities are within our fair value range, though they are getting more expensive. Investors should maintain neutral allocations and, in their foreign equity exposure, overweight European and Asian equities at the expense of US and Australia.

- New Zealand fixed income offers better yields than other global markets and investors should maintain exposure to New Zealand bonds and cash. The New Zealand dollar should remain weak versus the US dollar but not necessarily other currencies, including the Australian dollar. Investors should maintain partial hedges while ensuring they do not underweight the US dollar.

- Asset class volatility is likely to rise in 2015. New Zealand–based investors should take advantage of the strong returns to local assets in 2014 to rebalance portfolios.

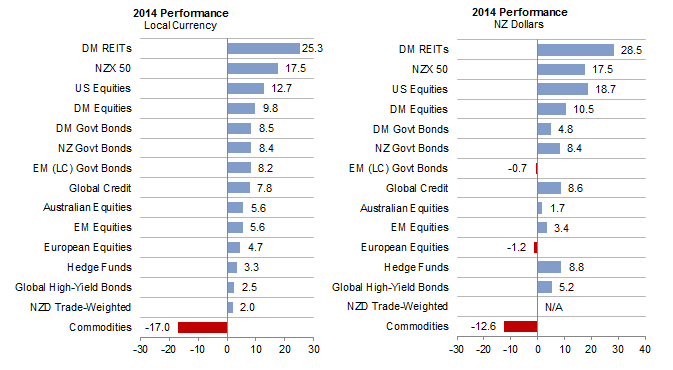

Investors in New Zealand assets had a good year in 2014 (Figure 1). Local equities outperformed global markets, local bonds rallied, and the property market remained buoyant. While the New Zealand dollar fell versus the US dollar, the kiwi appreciated versus most other currencies, including the Australian dollar, making local asset class performance look even stronger in NZD terms.

Figure 1. 2014 Performance

As of 31 December 2014 • Percent (%)

Can the good times last? For now, it seems so. The outlook for the economy is generally positive and New Zealand is experiencing rising positive net migration, a reversal of a longstanding trend. We expect the economic divergence between New Zealand and most of the developed world, including Australia, to continue.

However, this doesn’t mean there won’t be any bumps in the road for investors, especially given that New Zealand, as a small open economy, is still at the mercy of global trends. The combination of a slowing Chinese economy, probable tightening by the US Federal Reserve, and a rising US dollar will likely create rising market volatility that will weigh on most asset classes in 2015.

For New Zealand–based investors, the run-up in local asset prices means some rebalancing of portfolios may be in order to prepare for rising market volatility. New Zealand equities are fairly valued but becoming more expensive, and a repeat of last year’s strong performance is unlikely. New Zealand government bonds are also becoming a bit stretched given the recent tumble in yields, but remain attractive on a global basis. We expect the New Zealand dollar to remain weak versus the US dollar, but supported versus other currencies.

Global Developments Remain Key to Domestic Economic Growth

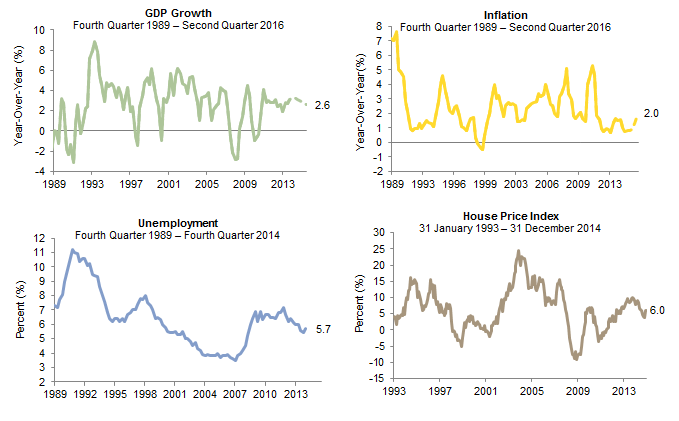

The macro outlook for New Zealand is rather benign. After growing at an estimated 3.3% pace in 2014, economic growth is expected to only slow modestly to 2.9% by the end of 2015 and then to 2.6% in mid-2016 (Figure 2). Steady growth is predicated on continuing strength in the labor market and only a modest impact from waning earthquake rebuilding efforts in Christchurch. Net migration is also expected to continue to provide a boost.[1]Although it should be noted that not all migrants are employable skilled laborers or high wage earners. Inflation was already low before the recent tumble in global commodity prices and finished the year at only 0.8%. Consensus forecasts see inflation rising modestly to 1.3% by year-end 2015 and rising to 2.0% by second quarter 2016 (Figure 2). Inflation is set to remain low going forward, both due to lower commodity prices but also larger slack in the economy than previously understood. Recent revisions to GDP data revealed the economy to be growing more slowly than initially reported in 2014, helping to explain why seemingly high GDP growth at the time and a tightening labor market were not feeding through to higher inflation. The Reserve Bank of New Zealand (RBNZ) acknowledged the lack of inflation pressures in the economy in January 2015, signaling to the markets it is not in a rush to raise rates, with the central bank expected to remain on hold for the rest of the year.

Figure 2. New Zealand Economic Indicators

In some regards, the only “problem” facing New Zealand’s economy is the housing market, which is heating up again. Given the RBNZ is reluctant to raise rates, the central bank will likely undertake more “macro-prudential measures” to cool the housing market, such as increasing down payments and curtailing lending to property investors (as opposed to owner-occupiers).

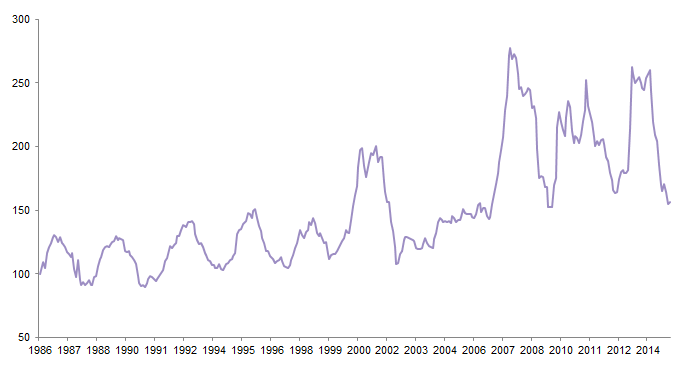

While there seem to be few problems on the domestic front, several key risks come from outside of New Zealand. Global dairy prices tumbled 39% in NZD terms in 2014 and will result in lower farm profits (Figure 3). The impact is expected to be transitory as dairy prices are expected to stabilise and rise going forward. Yet continued dairy price weakness amid rising global production would pose more of a headwind to the economy than currently expected.

Figure 3. ANZ Dairy Price Index

31 January 1986 – 31 January 2015 • New Zealand Dollar Terms

The timing and magnitude of interest rate hikes in the United States is another risk. The most likely scenario is that the Fed will begin to hike rates later this year, but not by much. The markets expect roughly 50 bps of tightening, which seems reasonable. The Fed will assess the impact of a strong dollar and weak oil prices on the US economy, and also gauge the impact of small rate hikes on financial markets before proceeding further. At the same time, the lack of obvious inflationary pressures in the United States implies little need for the Fed to aggressively hike rates. If the Fed does tighten, currency and financial market volatility could increase, which may weigh on global growth, especially with growth in Europe and Japan remaining lackluster.

See Aaron Costello et al., “China: Prepare for Stress,” Cambridge Associates Research Note, October 2014, and Jason Widjaja et al., “Australia Outlook 2015: Still Cautious,” Cambridge Associates Research Note, February 2015.

Given the significant linkages between China, Australia, and New Zealand (China and Australia account for 40% of New Zealand’s exports), the prospect of a slowing China and the weak outlook for the Australian economy also need to be considered. Although we do not expect a hard landing for China or Australia in 2015, we are not optimistic on the outlook for either economy, and see growth continuing to slow. Weakness in China and Australia will likely have some spillover effects on New Zealand, but the economic divergence between New Zealand and Australia looks set to continue, as New Zealand is a net beneficiary of China’s economic rebalancing away from investment-driven growth.

Put simply, New Zealand sells what China needs going forward (agricultural and soft commodities), while Australia sells what China needs less of (industrial commodities). If Australia was among the big winners of the previous cycle (alongside other hard commodity exporters and investment plays), New Zealand should be among the winners this cycle.

In the near term, New Zealand should benefit more from the fall in global oil prices than Australia, given that falling oil prices will also impact the price of liquid natural gas, a sector that Australia had hoped would offset reduced mining exports.

At the same time, households in New Zealand are not as leveraged as their Australian cousins, nor is the New Zealand housing market as overvalued (at least not yet). A key part of Australia’s resilience over the past few years amid a slowing China has been rising household debt and a booming housing market, both of which seem to have hit their limits. New Zealand still has scope for the household sector to support the economy even amid a sluggish external environment.

Mixed Outlook for the New Zealand Dollar

The outlook for the New Zealand dollar is mixed, especially after January’s 7% fall versus the US dollar, which was triggered by the RBNZ changing its outlook on interest rates. The currency is back to its lowest level since late 2010. A case could be made that the New Zealand dollar is oversold and will rally in the near term. Yet on a longer-term basis the currency still appears expensive and with US rates set to rise and the RBNZ on hold, the path of least resistance for the New Zealand dollar is down (Figure 4).

Figure 4. New Zealand Dollar Valuations

Yet while the New Zealand dollar may weaken versus the greenback, the currency may be supported versus other developed markets currencies due to high relative interest rates and quantitative easing in Europe and Japan. The New Zealand dollar actually rose 2% in trade-weighted terms in 2014, despite falling 5% versus the US dollar. We expect this trend to continue, unless global dairy prices fall lower, which would weigh heavily on the kiwi.

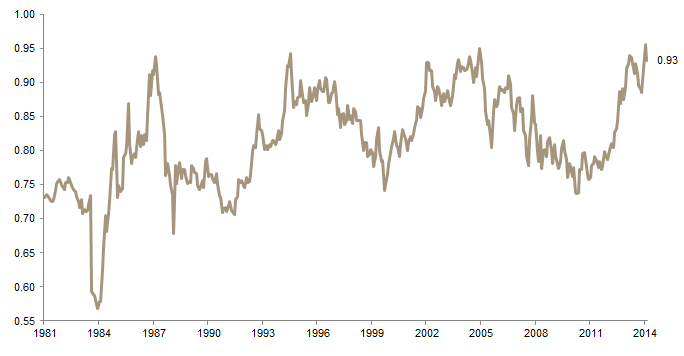

But what about the NZD/AUD exchange rate, which is currently near all-time highs (Figure 5)? Historically this rate has been very cyclical, with an easy rule-of-thumb to sell the New Zealand dollar when it approaches 0.95 and buy when it approaches 0.75. At the risk of saying “this time is different” (the most dangerous phrase in finance), we expect the New Zealand dollar to remain strong versus the Australian dollar. Both dairy and iron ore prices have fallen sharply, but we view the weakness in global dairy prices as largely cyclical and the collapse in iron ore prices as much more structural. Thus, New Zealand’s terms of trade can continue to rise versus Australia’s, even if New Zealand’s terms remain weak on an absolute basis. We would not be surprised to see the NZD/AUD exchange rate hit parity in the near term, especially if Australia is forced to cut rates further while the RBNZ remains on hold.

Figure 5. NZD/AUS Exchange Rate

31 December 1981 – 31 January 2015

What does this mean for hedging policies? We have advocated NZD-based investors maintain 50% hedge ratios given the overvaluation of the currency. We still feel 50% hedge ratios are appropriate, given lingering downside to the New Zealand dollar. While this assumes investors forego additional carry earned by a fully hedged strategy, we see the benefits of partial hedging today as greater, especially if rising US rates narrow the carry spread. Also, given the US dollar’s tendency to rally sharply amid periods of market stress, partial hedging will reduce the need to settle currency hedges amid depressed portfolio values. In short, a 50% hedge ratio minimizes regret amid an uncertain outlook for the currency.

New Zealand Equities Are Looking Vulnerable

New Zealand equities had another strong year in 2014, outperforming global benchmarks with the NZX 50 Index returning 17.5% and the MSCI New Zealand Investable Market Index returning 19.2%. The outperformance was driven mainly by high dividend sectors, a theme seen globally in 2014 and highlighted in the strong performance of REITs and infrastructure plays, which have benefited from falling global bond yields.

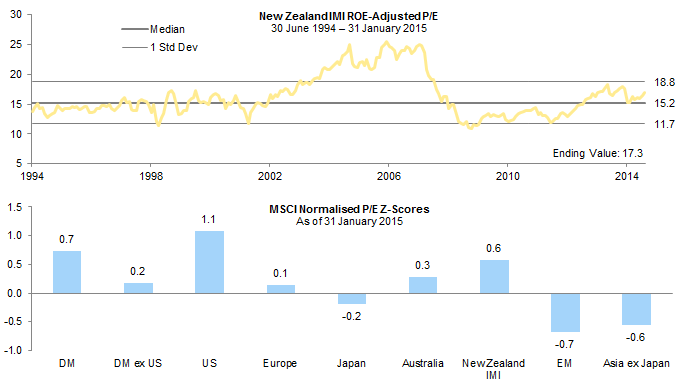

Given the strong performance, New Zealand equities are becoming more expensive, but still fall within our fair value range (Figure 6). The valuation picture is complex, given dispersion among different valuation metrics. For instance, at the end of January the market was 30% overvalued on a forward price-earnings (P/E) basis and 14% overvalued on a price-to–book value basis, but only 5% above historical norms on a dividend yield basis. Looking across six different valuation metrics, the New Zealand market has a median overvaluation of 14%, similar to what’s implied by our return on equity–adjusted P/E metric. There is always uncertainty over the “true” valuation of any stock market, but it seems clear that New Zealand equities are no longer cheap and are vulnerable to a pull back. This is especially the case if rising rates in the United States temporarily lessen demand for yield plays, similar to what occurred in 2013.

Figure 6. New Zealand ROE-Adjusted P/E and Z-Scores for Various Markets

Looking outside of New Zealand, valuations for developed markets equities also appear a bit expensive, but this is concentrated in US equities, which we view as overvalued (Figure 6). Indeed, New Zealand equities still appear relatively attractive compared to US equities on our metrics, but expensive relative to others.

New Zealand investors should modestly underweight US equities in favor of non-US markets. We are neutral on Australian equities, and do not see a compelling reason for New Zealand investors to overweight that market as it is not particularly cheap. A case can be made for overweights to European and Japanese equities, given valuations and ongoing quantitative easing, which could boost stock markets in these regions despite lackluster economic growth.

See Celia Dallas, “VantagePoint,” Cambridge Associates, First Quarter 2015.

Emerging markets equities offer the most attractive valuations globally, but are a tricky call for New Zealand investors. The lack of a clear catalyst and the risks posed by the potential for rising US rates and a strong US dollar make emerging markets equities unappealing. Still, holding what is cheap pays off over the long run, and today Cambridge favors small overweights to Asia ex Japan equities, given that Asia is a net beneficiary of weaker oil and commodity prices, and Asian currencies have stronger fundamentals compared to other emerging markets. Yet New Zealand–based investors already have fundamental economic exposure to Asia based on trade flows. Ultimately, we think modest tilts toward Asia are reasonable for New Zealand–based investors, and recommend maintaining neutral portfolio weights to New Zealand equities (which we assume to be larger than their weights in global benchmarks) and modest underweights to US and Australian equities in favor of Europe, Japan, and Asia ex Japan.

The Search for Yield Stops in New Zealand

New Zealand government bonds returned over 8% in 2014, in line with other developed markets, and have continued to rally in early 2015 as global bond yields tumble amid deflation concerns and the anticipated impact of expanded quantitative easing by the European Central Bank and Bank of Japan. The decision by the RBNZ to remove its “tightening bias” in January has also helped New Zealand yields rally further.

Given the 150 bp point drop in yields since the end of 2013, New Zealand government bonds are starting to look expensive on the metrics we track. Yet we still view New Zealand bonds as relatively attractive, as yields remain high in real terms and relative to global yields (Figure 7).

Figure 7. New Zealand Yields and Global Yields

With the yield curve now inverted, the case for holding duration is greatly diminished, although bond yields could rally more if global growth concerns intensify, especially if China slows sharply or US growth begins to stall.

We see little reason for New Zealand investors to search for yield offshore, given that global investment-grade bond yields at 2.8% remain 90 bps below those of New Zealand bank bills. New Zealand–based investors should maintain policy weights to domestic fixed income, including government bonds, given the lack of inflation risks. However, reducing bonds and holding some extra cash may be advisable, given concerns over the liquidity of the local bond market.

Conclusion

New Zealand’s economy is well positioned compared to other major economies, and especially relative to Australia, but external factors will likely impact the local economy and markets.

New Zealand asset classes had a strong 2014, and are unlikely to fare quite so well in 2015. New Zealand equities, which outperformed in 2014, are growing more expensive but are still within our fair value range. We advise investors to maintain neutral allocations to New Zealand equities, and in their foreign equity exposure to overweight Europe, Japan, and Asia ex Japan equities at the expense of US and Australian equities. Investors should also maintain neutral allocations to New Zealand fixed income (including cash), which offers better yields than other global markets. The New Zealand dollar should remain weak versus the US dollar but not necessarily other currencies, including the Australian dollar. Investors should retain partial hedges while at the same time ensuring they are not underweight the US dollar. This could entail leaving US equity allocations unhedged.

All in all, asset class volatility is likely to rise in 2015 amid a strengthening US dollar and rising US interest rates. Investors should take advantage of the strong returns to local assets in 2014 to rebalance portfolios.

Contributors

Aaron Costello, Managing Director

Jason Widjaja, Senior Investment Associate

Exhibit Notes

2014 Performance

Sources: Barclays, Bloomberg L.P., BofA Merrill Lynch, Citigroup Global Markets, Hedge Fund Research, Inc., J.P. Morgan Securities, Inc., MSCI Inc., and Thomson Reuters Datastream. MSCI data provided “as is” without any express or implied warranties.

Notes: “DM REITs” represents the MSCI World REITs Index. “US Equities” represents the MSCI US Index. “DM Equities” represents the MSCI World Index. “DM Govt Bonds” represents the Citigroup World Government Bond Index. “NZ Govt Bonds” represents the J.P. Morgan GBI New Zealand Index. “EM (LC) Govt Bonds” represents the J.P. Morgan Government Bond Index Emerging Markets Global Diversified. “Global Credit” represents the BofA Merrill Lynch Global Broad Corporate Bond Index. “Australian Equities” represents the MSCI Australia Index. “EM Equities” represents the MSCI Emerging Markets Index. “European Equities” represents the MSCI Europe Index. “Hedge Funds” represents the Hedge Fund Research Fund of Funds Composite Index. “Global High-Yield Bonds” represents the BofA Merrill Lynch Global High Yield Bond Index. “NZD Trade-Weighted” represents the J.P. Morgan Trade-Weighted NZD Index. “Commodities” represents the Bloomberg Commodity Index.

New Zealand Economic Indicators

Sources: Bloomberg L.P. and Thomson Reuters Datastream.

Note: Dashed lines represent Bloomberg median analyst forecasts.

ANZ Dairy Price Index

Source: Thomson Reuters Datastream.

New Zealand Dollar Valuations

Sources: Bank for International Settlements, The Economist, Goldman, Sachs & Co., International Monetary Fund (IMF), J.P. Morgan Securities, MSCI Inc., and Thomson Reuters Datastream. MSCI data provided “as is” without any express or implied warranties.

Notes: Real effective exchange rate (REER) is as of 31 December 2014 and expressed as percent change over long-term average. PPP-implied exchange rates are based on relative price levels between countries, with the assumption that a basket of identical goods should cost the same across countries. Average PPP estimates reflect a simple average using IMF and The Economist data, which are based on consumer prices. Fair value model estimates are derived from econometric models that take into account several variables such as PPP, interest rate differentials, fund flows, etc., to produce an equilibrium exchange rate. These fair value estimates differ from currency forecasts, as it is not always assumed that currencies revert to fair value over the forecast horizon. Average fair value model estimates reflect a simple average using Goldman Sachs and J.P. Morgan data.

NZD/AUS Exchange Rate

Sources: MSCI Inc. and Thomson Reuters Datastream. MSCI data provided “as is” without any express or implied warranties.

New Zealand ROE-Adjusted P/E and Z-Scores for Various Markets

Sources: MSCI Inc. and Thomson Reuters Datastream. MSCI data provided “as is” without any express or implied warranties.

Notes: The composite normalised price-earnings (P/E) ratio is calculated by dividing the inflation-adjusted index price by the simple average of three normalised earnings metrics: ten-year average real earnings (i.e., Shiller earnings), trend-line earnings, and return on equity (ROE)–adjusted earnings. We have removed the bubble years 1998–2000 from our mean and standard deviation calculations. Japan equity valuation is based on price-to-book ratio. Asia ex Japan and New Zealand equity valuations are based only on the ROE-adjusted P/E. Valuations for all other markets are based on the composite normalised P/E. All data are monthly.

New Zealand Yields and Global Yields

Source: Thomson Reuters Datastream.

Note: Top graph is based on daily data; bottom is based on monthly.

Footnotes