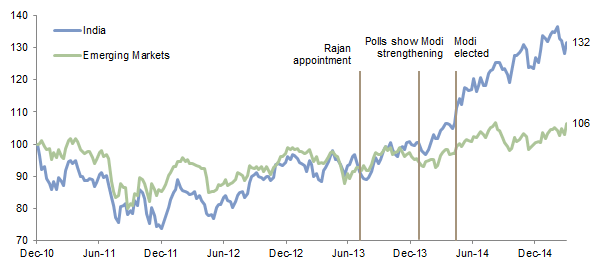

Over the past two years, India has come full circle, moving from a member of the so-called Fragile Five economies with poor macro fundamentals to one of the few emerging markets with a positive macro story. India was among the best-performing equity markets in 2014, returning 24% in US$ terms, compared to -1.8% for emerging markets equities and 14% for US equities. So far this year India remains a solid performer, up 5% in US$ terms at the end of March.

Can the bull market continue? To date, a primary driver has been hope of things to come from a new government that has achieved some small victories. Valuations have run up on the back of these hopes, and a period of consolidation seems overdue. While the market appears vulnerable in the near term, the intermediate-term outlook for Indian equities is positive, provided Prime Minister Narendra Modi can continue to implement reforms focused on making the government, and thereby the economy, more efficient.

The Modi Effect

The catalyst for the resurgence of the Indian equity market was the 2014 electoral victory of the Bharatiya Janata party (BJP) led by Modi, a known reformer who promised greater government efficiency, increased spending on infrastructure, and a clampdown on corruption following five years of increasingly ineffective and dysfunctional government by the Congress party. Indian equities began outperforming broader emerging markets equities in early 2014 as it became increasingly clear that Modi would win the election, and surged after the announcement of a landslide victory that gave the BJP a majority in parliament.

MSCI Emerging Markets and India Price Levels

31 December 2010 – 3 April 2015 • 31 December 2010 = 100 • Local Currency

The market’s euphoria over Modi’s election has not been matched by major economic or political reforms. Instead, Modi has focused more on whipping into shape India’s notoriously inefficient bureaucracy and achieving a rash of small but meaningful initiatives.[1]Examples include implementing electronic recordkeeping, online submission of permits with approval tracking, slashing the number of forms/approvals required for certain permits, and requiring … Continue reading This has set the tone that his administration can and will get things done, triggering widespread optimism among the business and investment community. In short, the market has rallied on the hope of more to come rather than on big results—although cynics would argue getting the Indian government to do anything is a major accomplishment.

A case in point is the most recent budget, unveiled on February 28, 2015. The market reaction was quite muted, having already priced in much of what was announced. Specifically, the proposed budget calls for slowing the pace of fiscal consolidation to allow for increasing infrastructure spending by 25%. The budget also announced the goal of implementing a nationwide sales tax system by April 2016, which will eliminate a host of overlapping state-level taxes and hopefully lower the costs of doing business within India. Corporate tax rates will also be cut from 30% to 25% over the next four years. While the budget itself does not amount to a “big-bang” reform agenda, if implemented successfully, these initiatives and Modi’s overall goal of increasing government efficiency should provide a boost to India’s economy.

The Rajan Effect

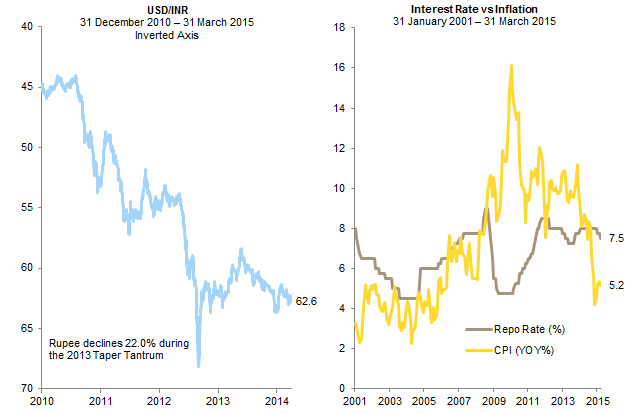

While headlines have focused more on Modi, the 2013 appointment of Raghuram Rajan as governor of the Reserve Bank of India (RBI) is arguably of equal importance as a turning point for the Indian economy and markets. Rajan’s decisive actions and rate hikes helped to stabilize the Indian rupee following the 2013 “Taper Tantrum” and fight painfully high inflation in India.

Inflationary pressures have recently subsided as commodity prices have tumbled, pulling inflation in India down from around 10% in 2013 to 5% at the end of February. This has allowed the RBI to cut its target lending rate by 25 bps in both January and March. The prospect of additional rate cuts by the RBI is bullish for the Indian economy, as lower borrowing costs are needed to restart an investment cycle crippled by double-digit borrowing costs.

In March the RBI announced its plan to adopt a formal inflation-targeting framework starting in 2017, comprising an inflation target of 4% with a band of plus or minus 2%. While not yet codified into law (and thus subject to change), an inflation-targeting framework would help make the RBI truly independent from the government, a major achievement for Rajan and future macro stability.

The Indian Rupee, Interest Rate, and Inflation

The Oil Effect

The fall in the price of oil has been unambiguously bullish for India. As mentioned earlier, lower oil prices have contributed to lower inflation and thus allowed the central bank to begin easing monetary policy. Oil imports are one of the biggest contributors to India’s current account deficit, which has improved dramatically, shrinking from -5% of GDP in 2013 to -1% in 2014, with some analysts forecasting India could run a modest current account surplus at some point in 2015. Improvement in the current account should continue to provide support to the rupee, which has gained year-to-date versus the US dollar despite RBI rate cuts.

The fall in oil prices also allowed Modi to cut fuel subsidies with minimal backlash from the Indian population. Since fuel subsidies account for around 25% of total subsidies, eliminating them frees up funds that can be spent in more impactful ways, such as improving the country’s infrastructure.

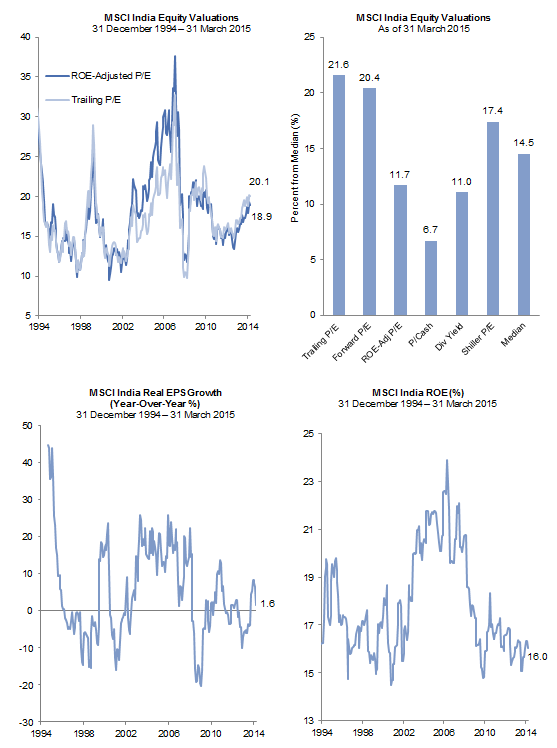

Valuations Are Becoming Stretched

While there are many reasons to be bullish on the economic outlook for India, there is growing concern over equity valuations given the powerful rally. At the end of March, the market was 20% overvalued on both a trailing and forward price-earnings (P/E) basis, with these metrics back to early-2007 levels. The market is less expensive on a return on equity (ROE)–adjusted P/E basis[2]The ROE-adjusted P/E adjusts the current P/E (based on trailing 12-month EPS) by the ratio of current ROE to long-term ROE to account for the cyclicality of earnings. This is useful in markets with … Continue reading (our standard metric for emerging markets valuations) at 11.7% above its post-1994 median. Looking across six different valuations metrics, the median indicator shows Indian equities are 15% overvalued. Valuations are even more stretched for small and mid caps. Still, valuations are far from the very overvalued levels seen in late 2007 when the market was between 50% and 100% overvalued.

Weak earnings growth is behind part of the dispersion across valuation metrics. Based on MSCI data, growth in real earnings per share (EPS) has slowed to just 1.9% over the 12 months to March (despite the sharp fall in inflation). At the same time, Indian banks suffer from large non-performing loans and depressed ROE, which may be impacting the ROE-adjusted P/E ratio. With underlying profits still depressed, the entirety of the recent rally has been driven by valuation expansion on the assumption that profits will come roaring back, similar to 2004 –07. To date, corporate profits have not yet rebounded as the hoped-for capex and investment cycle has not yet gotten underway.

With valuations becoming more stretched, the next phase of the rally will require tangible proof of economic growth and improving corporate profits. The market’s lackluster response to the recent budget unveiling and the RBI rate cut suggest the need for a period of consolidation to let fundamentals catch up.

MSCI India Valuations and Fundamentals

What’s in a Number?

India’s recent revisions to how it calculates GDP further cloud the picture. In February the statistics ministry updated the base year used for GDP calculations from 2005 to 2012 and switched to using market prices rather than factor costs.

The new methodology shows that the Indian economy grew by 6.6% in 2013 and 7.5% in 2014, both 200 bps higher than the old methodology. While the new methodology is more in line with international standards, the new figures have been greeted with widespread skepticism, with several economists (including the RBI) commenting that the much higher growth rates do not accord with other indicators pointing to a weak Indian economy over the past few years.

Whether GDP grew at 5.5% or 7.5% in 2014, the fact remains the economy is not growing at the almost 9% average pace seen over the 2004 –10 period (under the old methodology). Yet 9% growth seems to be what the equity markets are priced for and what the economy must deliver to justify current valuations.

Real GDP Growth

Second Quarter 2005 – Fourth Quarter 2014 • Year-Over-Year (%)

Moving in the Right Direction, But More Reforms Needed

The macro backdrop in India has improved, with a sustained fall in the price of oil a “game changer” for the economy. Yet a lower price of oil is cyclical in nature; what India needs most are supply-side reforms and infrastructure that improves the allocation of capital and distribution of goods, resulting in structurally lower inflation and interest rates. Lower interest rates should trigger a classic boom based on a virtuous circle of increased investment spending and consumption. But absent structural supply-side improvements, any cyclical rebound in growth will be self-limiting as inflation returns. The most recent budget is a step in the right direction, but the big issues of labor, land, tax, and bankruptcy reforms—as well as the privatization of state-owned enterprises—have yet to be tackled in earnest and will take time and political will to achieve. The “honeymoon” phase for Modi and the markets may be drawing to a close, and the tough task of implementing is next.

The Bottom Line

A period of consolidation for Indian equities is overdue. Corporate earnings must pick up over the coming months or the rally will falter. A rebound in the price of oil, a surprise rise in inflation, or general market unease over potential Federal Reserve rate hikes could be the catalyst for a market pullback. However, given that India is still near the bottom of the economic and earnings cycle, investors should give the market the benefit of the doubt over the intermediate term, provided Modi can continue to implement reforms focused on making the government, and thereby the economy, more efficient. A shakeout in the market that cools expectations and improves valuations will offer a better buying opportunity.

Aaron Costello, Managing Director

Jason Widjaja, Senior Investment Associate

Exhibit Notes

MSCI Emerging Markets and India Price Levels

Sources: MSCI Inc. and Thomson Reuters Datastream. MSCI data provided “as is” without any express or implied warranties.

Note: Price levels are weekly.

The Indian Rupee, Interest Rate, and Inflation

Sources: MSCI Inc., Reserve Bank of India, and Thomson Reuters Datastream. MSCI data provided “as is” without any express or implied warranties.

MSCI India Valuations and Fundamentals

Sources: MSCI Inc. and Thomson Reuters Datastream. MSCI data provided “as is” without any express or implied warranties.

Note: Year-over-year real EPS growth starts 31 August 1995.

Real GDP Growth

Sources: Central Statistical Organization, India, and Thomson Reuters Datastream.

Notes: In February the statistics ministry updated the base year used for GDP calculations from 2005 to 2012 and switched to using market prices rather than factor costs. Real GDP data for fourth quarter 2014 are based on Oxford Economics forecasts.

Footnotes