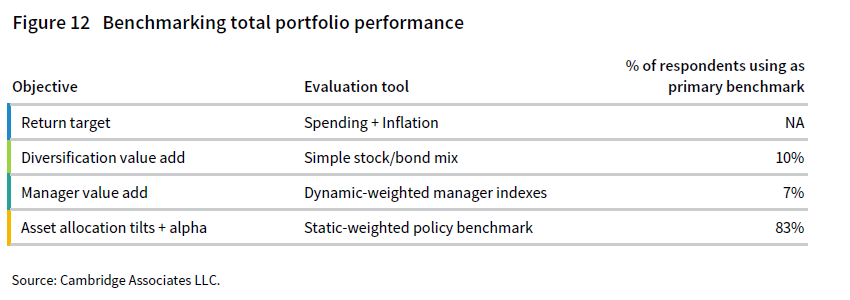

Summary of policy benchmarking approaches

Benchmarking investment performance is an essential piece of an endowment’s well-functioning governance process. When selecting a benchmark, it is important for institutions to understand what types of questions they are seeking to answer (Figure 12). There is no single benchmark that can assess every single aspect of portfolio management. Consequently, it is not uncommon for institutions to use multiple benchmarks in their performance evaluation process. In our survey, we asked respondents to provide both the real return objective for the endowment and the primary benchmark used to evaluate investment performance at the total portfolio level.

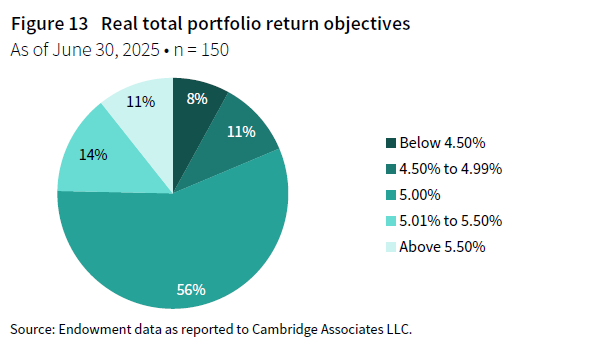

A fundamental part of an endowment’s investment policy is the return objective. Most endowments use a spending policy that is connected in some way to an annual spending rate. That percentage rate serves as the basis for establishing a minimum return target that endowments aim to earn over the long term. If an endowment can generate an investment return that exceeds the sum of its spending rate and inflation, it can maintain or grow the purchasing power of its assets over time. The most common real (i.e., inflation-adjusted) return objective among endowments continues to be 5% (Figure 13).

In the Investment Portfolio Returns section, we cited the performance of a blended index weighted 70% to the MSCI ACWI and 30% to the Bloomberg Aggregate Bond Index. For endowments that are diversified across alternative asset classes, this type of benchmark helps to evaluate whether the decision to diversify the portfolio added value. Our comparisons of median endowment performance versus the 70/30 benchmark show how the peer universe in general measured up to a simple, passive investment option.

In practice, just 10% of respondents reported that a simple blended index was the primary benchmark used for their total portfolio return. The most common approach among this subgroup was to use a blend weighted 70% to an equity component and 30% to a bond component. However, some reported equity weightings as low as 60%, while others reported weightings as high as 85%. The most appropriate benchmark weighting should align with the portfolio’s target risk profile. In fact, nine of the 29 institutions in this cohort also used only two categories in their target asset allocation policy, and the weightings of the equity and bond indexes matched their policy targets to the equity/growth and bond categories in their policy structure.

The remaining peers in the universe used a policy benchmark with three or more components. The vast majority (83%) used a blend of indexes with static weightings that align exactly or closely with the asset classes and target percentages specified in their asset allocation policies. This type of benchmark helps an institution evaluate how its endowment performed relative to the blended index that represents its default or normative position. A small percentage of respondents (7%) used a blend of manager-specific indexes, where the weightings update frequently (e.g., monthly) to match each manager’s allocation in the portfolio. This type of benchmark is intended to focus on manager selection decisions and neutralizes the effects of over/underweights of the actual asset allocation versus policy targets. The figures that follow provide more detail on benchmarks for the endowments that used a dynamic-weighted or static-weighted policy benchmark.

Components of policy portfolio benchmarks

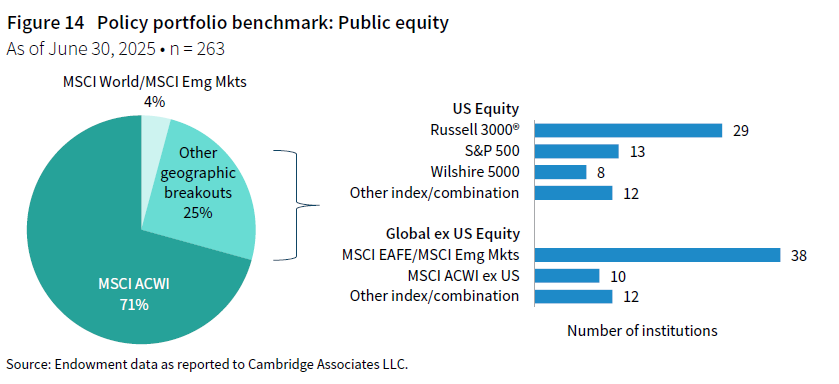

The MSCI ACWI continues to be the most common benchmark for public equities. In fiscal year 2025, 71% of the respondent group used this index to represent their entire public equity allocation in the policy portfolio benchmark (Figure 14). This was up slightly from the 69% of institutions that cited the index in last year’s study. The remaining respondents use a combination of indexes that are more geographically defined. For those that use a US-focused benchmark, the Russell 3000® Index was by far the most prevalent. For global ex US equities, a combination of the MSCI EAFE Index and the MSCI Emerging Markets Index was cited most often.

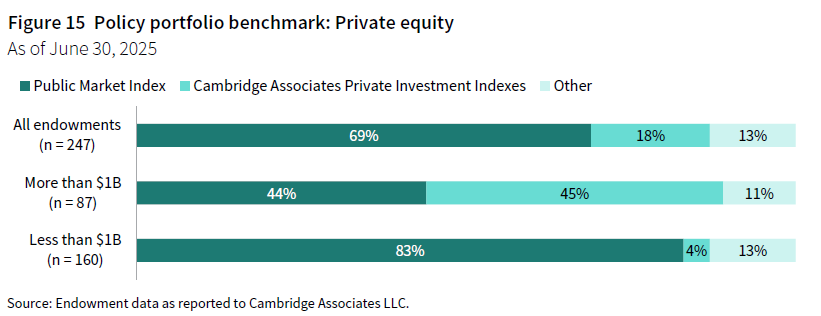

When evaluating PE/VC in the policy benchmark, a majority of the overall universe (69%) used a public index (Figure 15). The rationale for using a public index is that the public equity bucket in the portfolio was the funding source for private equity allocations; if the portfolio did not invest in private equity, that capital would have remained with the public equity allocation. The use of a public index primarily evaluates whether the decision to invest in private markets paid off for the portfolio.

There are some shortcomings to using a public index to benchmark private equities. Most notably, the public stock market is not a universe of securities that is representative of private equity investments. Consequently, in periods where there are large differentials between public equity and private equity performance, the spread between the portfolio return and the benchmark return can be more reflective of those market dynamics than of how well the management team implemented the private portion of the portfolio. Approximately 18% of endowments instead used the CA private investment indexes to represent private equity in the policy benchmark. These indexes do not meet the ideal properties of benchmark as they are not transparent or investable. However, they are a universe of institutional-quality private investment funds that are more representative of the asset class compared to a public index.

The survey responses from fiscal year 2025 looked almost identical to the year prior. There continued to be a stark difference in practices between smaller and larger endowments. For endowments less than $1 billion, a public index was by far the most common practice. In contrast, approaches were more mixed among endowments more than $1 billion—the percentage of respondents using the CA benchmarks was almost identical to the percentage using a public index. The private investment indexes can be custom weighted by vintage year and exposure across different strategies, which helps to evaluate fund selection. It is likely for this reason that the approach continued to be prevalent among larger endowments, as many have performance-based incentive compensation programs for their investment staff.

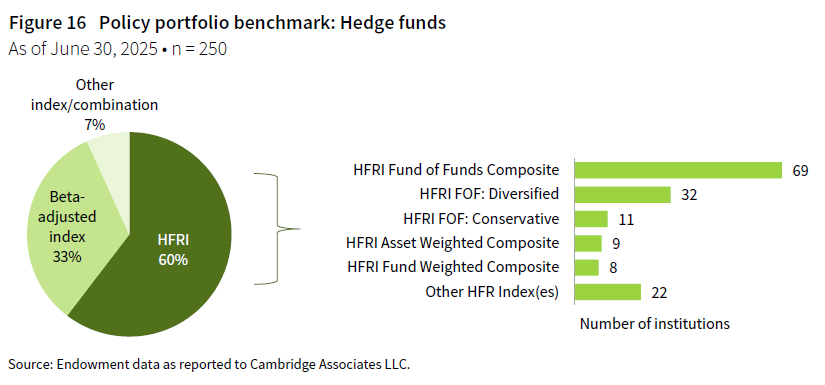

Endowments also face similar challenges of selecting an appropriate index when accounting for hedge fund allocations in the policy benchmark. Most respondents continued to use one or more indexes produced by Hedge Fund Research® (HFR), which tracks hedge fund managers that report to their database (Figure 16). Within this family of indexes, the HFRI Fund of Funds Composite was most often cited. Other approaches included a beta-adjusted benchmark, although the exact method varied across a few different options. Most respondents using this type of benchmark used either a blended public equity/bond index or a blended public equity/91-Day T-Bill return stream. In both instances, the MSCI ACWI with a 0.3 beta was the most common approach.

Benchmarking practices tended to be even more unique across the respondent group in other strategies. With bonds, the Bloomberg Aggregate Bond Index was used by 40% of institutions. The remaining participants chose benchmarks more specific to sector, maturity range, and/or geographic exposures. Benchmark combinations for real assets were even more unique across the respondent group due to the variety of strategies and exposures across those categories. Finally, while a majority of the universe had allocations to private credit strategies, only a small percentage of those endowments had a dedicated benchmark to private credit in the policy benchmark.

The choice of PE/VC benchmark has had a significant impact on performance evaluation in recent years

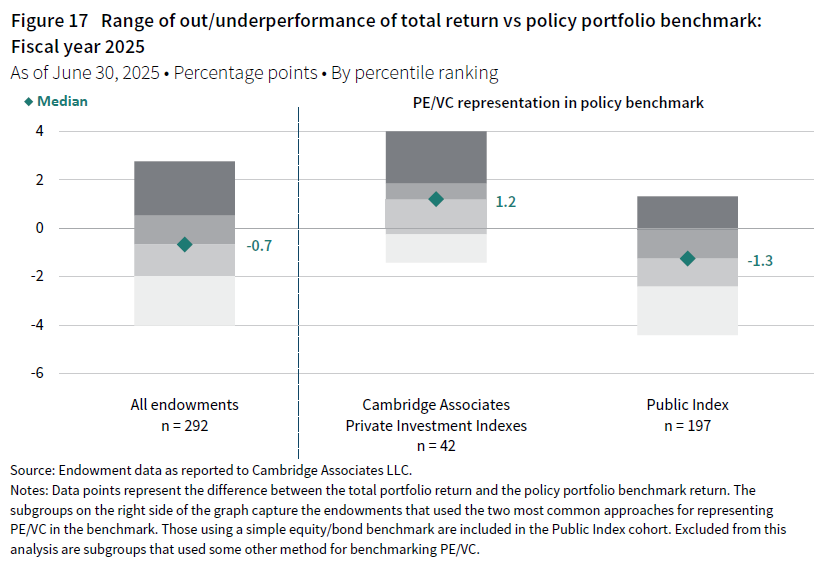

A majority (64%) of responding endowments fell short of their policy portfolio benchmark in 2025. When considering the spread between the portfolio return and the benchmark, the median across the respondent group was -70 bps for the fiscal year. Outcomes varied widely across endowments, ranging from 280 bps of outperformance at the top 5th percentile mark of the universe to underperformance of 400 bps at the bottom 5th percentile (Figure 17).

When further dissecting the peer universe, it is clear that the type of benchmark used for PE/VC was a big factor in how well an endowment performed versus its overall policy benchmark in 2025. For endowments that used the CA private investment indexes, the median value add was positive at 120 bps. More than two-thirds of the institutions in this cohort actually outperformed their policy benchmark over the past year. In contrast, the median value add for endowments using a public index was significantly lower at -130 bps. Just 24% of endowments in this subgroup outperformed their policy benchmark in 2025.

The different experiences of these two subgroups tie back to the relationship between public equity and private equity index returns in 2025. The one-year horizon IRR of the CA Private Equity and Venture Capital Index was considerably lower than the mPME version of the MSCI ACWI (10% versus 16%). Therefore, an endowment using a public market index would calculate a higher benchmark return than it would if using a private equity–specific index. With most endowments in the peer universe having 20% or more of their portfolios invested in PE/VC, the index choice is quite consequential in the policy benchmark calculation.

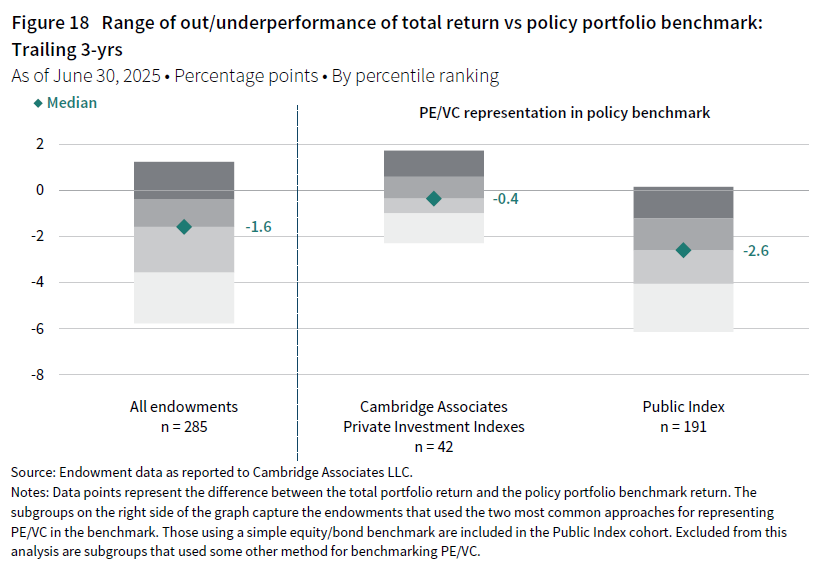

Endowments using the public index for PE/VC also have worse relative performance against their policy benchmarks over the trailing three-year period (Figure 18). This was not a surprise, given it was the third straight year where private equity trailed public equity market performance. However, the task of beating the benchmark was even more challenging than it was in 2025 for all endowments regardless of the choice of benchmark, with the median value add being negative for both cohorts. The median value add for the overall universe (-160 bps) was the lowest trailing three-year figure we have ever calculated in the decade-plus timeframe that we have been collecting this data. Further, just 7% of the public index group and 33% of the CA index group outperformed their policy benchmark for this period.

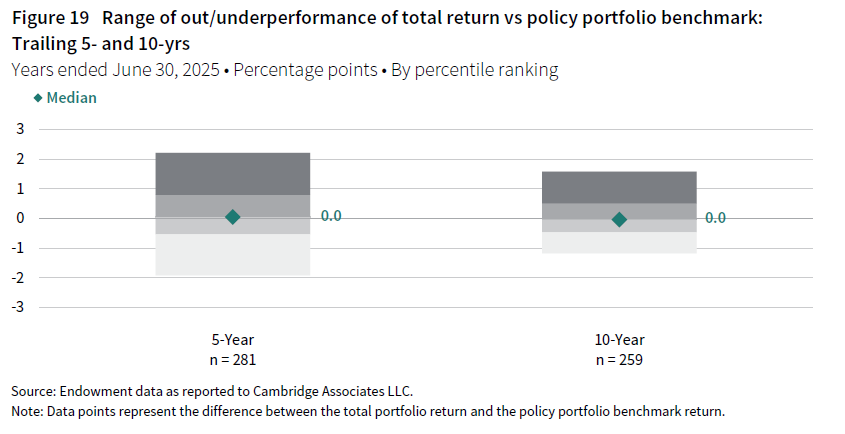

The differences in benchmarking approaches were less impactful on the value-add statistics for the trailing five- and ten-year periods (Figure 19). The distribution of value adds across peers was similar for both subgroups. A little more than half of respondents (51%) outperformed their benchmark over the five-year period, while a slightly smaller percentage (48%) beat their benchmark for the trailing ten-year period.