The launch of the new Treasury floating rate notes has been a successful venture

- The initial auction for Treasury FRNs saw aggressive participation, with a high bid-to-cover ratio. The ratio came down slightly in subsequent auctions.

- Quarterly issuance has so far exceeded early predictions, and these securities have already assumed an important place in the panoply of Treasury offerings.

- With $82 billion of Treasury FRNs currently outstanding, issuance is on track to outpace corporate floating rate note issuance in each of the last five years.

- Three classes of participants have dominated auction allotments: bank and non-bank brokers and dealers, investment funds, and foreign and international entities.

- Two indexes launched in the first quarter to track Treasury FRNs exclusively. Two ETFs presently are benchmarked against these indexes.

Several days before the first Treasury floating rate note (FRN) auction in late January 2014, we published the market commentary Treasury Floats a Noteworthy Idea. Now, with six auctions in the books and $82 billion of FRNs in circulation, we take a moment to review how the market has received the Treasury’s first new security in 17 years.

The First Auction

When the Treasury announced on January 23, 2014, that the first FRN auction would be $15 billion—the high end of the range expected by the market—the market didn’t flinch. In the immediate aftermath of the announcement, the premium to 91-day T-bills in “when issued” (WI) trading was an aggressive 5 bps to 6 bps compared with the Treasury Borrowing Advisory Committee’s (TBAC) expectations of a 10 bp to 15 bp spread. The trading range then broadened out to a discount margin of 3 bps to 6.25 bps; the bid/offer at the end of the day was +5.0 bps/+4.75 bps. One market participant we spoke with estimated that some $500 million traded in the WI cash market on the first day. On January 27 the Treasury held a 91-day T-bill auction, which established the “index rate” for the first FRN auction and resulted in a market clearing (“high”) rate of 0.055%. This became the index rate for the auction of $15 billion of FRNs two days later.

For a summary of selected terms, please see Treasury Floats a Noteworthy Idea.

In the January 29 FRN auction itself, the “stop” or high discount margin was 4.5 bps, reflecting aggressive participation by both dealers and customers. This 4.5 bps became the “spread” that, when added to the 5.5 bp index rate, established the “interest rate” or coupon for the issue. For the balance of the life of the issue, this same 4.5 bps will be added to the weekly 91-day T-bill high rate to determine the interest rate for the issue. Primary dealers clearly stepped up to support the Treasury in this initial auction. The bid-to-cover (BTC) ratio—the amount of bids received relative to the amount of securities offered—in the first FRN auction was high, at 5.67 times. That compares more closely to BTC ratios for T-bills than those for two-year notes or ten-year Treasury Inflation-Protected Securities (TIPS)(Figure 1). Among the competitive bids received, primary dealers took down $7.9 billion (53.2% of the competitively bid securities), customers placing bids through dealers (“indirect bidders”) took down $5.6 billion (37.8%), and non-primary dealers (“direct bidders”) took down $1.3 billion (8.9%). Non-competitive tenders were just $74.5 million, less than 1% of the total.

Figure 1. Bid-to-Cover Ratios of Selected Treasury Issues at 2014 Auction Dates

January 1, 2014 – June 30, 2014

Reopening Auctions and the Second Primary Auction

Two reopening auctions were held at the end of February and March. Each was sized at $13 billion, and this seems to have set the pattern for $41 billion in quarterly Treasury FRN issuance, at least for the first year.[1]Smaller reopenings of $10 billion and $12 billion had been projected by TBAC and the Treasury, respectively, on February 5, 2014. By the next TBAC meeting on April 30, 2014, both were projecting a … Continue reading Given earlier expectations of $35 billion in quarterly issuance, this is a positive sign for the market. Following the first primary auction, the spread/discount margin increased from its initial 4.5 bp “spread” to a 6.4 bp discount margin in the reopening at the end of February and to a 6.9 bp discount margin in the March reopening.

The second primary Treasury FRN auction occurred on April 29. It was bid against an index rate of 0.030%, as determined in the 91-day T-bill auction on April 21, and resulted in a 6.9 bp spread, equivalent to the discount margin in the March reopening. By the May reopening, the discount margin had closed slightly to 0.063%, resulting in a premium dollar price of 100.011671. Figure 2 traces the pricing of the first six auctions by showing their component parts: the index rate, the spread, the interest rate (“coupon”), the discount margin, and the price. According to a just-published report from the Government Accountability Office,[2]US Government Accountability Office, Debt Management: Floating Rate Notes Can Help Treasury Meet Borrowing Goals, but Additional Actions Are Needed to Help Manage Risk (June 2014) (GAO-14-535). the closeness of the rates quoted in the WI market to those in the first three auctions indicates the “price discovery mechanism of the market was functioning well for FRNs and that the market embraces and understands the security, which in turn indicates strong current and continuing demand that helps Treasury borrow at lower cost over time.”

Figure 2. Treasury FRN Auction Results and Pricing

As the discount margin for Treasury FRNs has generally trended upward, the BTC ratio has trended lower. Both measures reflect slightly more relaxed demand for these securities, perhaps as a result of the rally in longer duration Treasuries. The BTC ratio, initially 5.67, slid to 5.29 in February and has hovered since March in a narrow range between 4.43 and 4.69. Figure 1 illustrates that the market has bid as strongly for Treasury FRNs as for 91-day T-bills, and more strongly than for two-year Treasury notes and ten-year TIPS. Treasury FRN yields likewise generally move in tandem with those of 91-day T-Bills, as FRNs are priced off of them (Figure 3).

Figure 3. Yield Comparison

January 27, 2014 – June 30, 2014

Non-competitive tenders have trended downwards since the initial auction. In fact, the total of such tenders in the subsequent five auctions totaled $78.1 million, just a tad more than the $74.5 million seen in January. On average, non-competitive tenders for the first Treasury FRN in the first quarter represented 0.2% of FRNs auctioned, compared to 0.5% for two-year notes, and 1.5% for 13-week T-bills. This may reflect that the retail market is less developed for Treasury FRNs, given their recent rollout.

The Market Today: Size and Participants

There are now $82 billion of Treasury FRNs outstanding.[3]As we go to press, the Treasury has just auctioned its third FRN. This $15 billion FRN, which has a July 31 settlement date, has virtually the same spread (7 bps versus 6.9 bps) as on the second … Continue reading At the current pace of issuance this figure will rise to $164 billion by the end of 2014, which is higher than the $154.1 billion in floating rate notes issued by US corporations last year and more than US corporate issuance of floating rate notes in each of the last five—and nine of the last 18—years (Figure 4).

Figure 4. Annual US Issuance of Floating Rate Notes

1996–2014

Floating rate notes’ tiny fraction of outstanding Treasury issuance should not obscure this security’s prominent role since inception. Treasury FRN issuance replaced $55 billion of 13-week T-bill issuance in the first quarter and accounted for fully 20% of net coupon issuance. Issuance during the first six months of the year was slightly higher than that of TIPS ($82 billion versus $75 billion)—and just under that of 30-year Treasuries ($84 billion); Treasury FRNs represented 7.3% of total coupon (note and bond) issuance. The relative importance of Treasury FRNs should also increase over the next couple of years as the Treasury is now overfunded and has been decreasing auction sizes for two- and three-year nominal Treasuries. Three classes of participants have dominated allotments: bank and non-bank brokers and dealers, investment funds, and “foreign and international” entities that participated either directly or through the Federal Reserve Bank of New York. This appears consistent with the TBAC’s expectation, outlined in our January paper, of strong participation from Treasury money market mutual funds and foreign central banks in addition to the primary dealer community (Figure 5). A recent GAO survey found that “respondents anticipate that money market mutual funds, corporate treasuries, and foreign central banks are likely to have the most demand for two-year FRNs. Survey respondents noted a number of reasons why Treasury FRNs are an attractive investment option, including the interest rate risk protection they provide the purchaser, their price stability, their use as a cash management tool, their consistency with investment guidelines and regulatory requirements, and the liquidity of the securities.”[4]US Government Accountability Office, Debt Management: Floating Rate Notes Can Help Treasury Meet Borrowing Goals, but Additional Actions Are Needed to Help Manage Risk (June 2014) (GAO-14-535)

Figure 5. Auction Allotments by Investor Class for Two-Year Treasury Floating Rate Notes

Prior to the first auction there was a school of thought in the dealer community that Treasury money market funds might participate more in the two reopening auctions than in the January 29 auction because the FRNs would mature in 23 months and 22 months, respectively, and therefore wouldn’t have as large an impact on the weighted-average portfolio life of the funds under rule 2a-7. This may indeed have been the case, as allotments to investment funds were greater in the first two reopening auctions than in the first primary auction. However, that did not seem to be the case in the May and June reopening auctions, so it is hard to conclude at this stage whether the slightly shorter maturity was the cause in the first two reopening auctions or if portfolio managers just sat on the sidelines in the first primary auction to see if the process would run smoothly, knowing there would be plenty of supply in subsequent months. More broadly, the dollar-weighted average portfolio life (DWAL) rule does not appear to have significantly hindered Treasury money market fund purchases in the first quarter, although it is possible the drop-off in demand in the May and June reopenings hints at capacity constraints at current DWALs.

Indexes and Investment Vehicles

The Barclays US Dollar Treasury Floating Rate Note Index (Barclays Treasury FRN Index) and the Bloomberg US Treasury Floating Rate Bond Index (Bloomberg Treasury FRN Index) were launched in the first quarter and track Treasury FRNs exclusively. Figure 6 compares these two new indexes to the three indexes that represent the broader floating rate note universe provided by Barclays, J.P. Morgan, and Market Vectors. The three broader indexes include exposure to entities outside the United States and a range of investment-grade fixed income by quality and, as discussed in our January paper, have a heavy weighting to financials.

Figure 6. Floating Rate Note Indexes

As of June 30, 2014

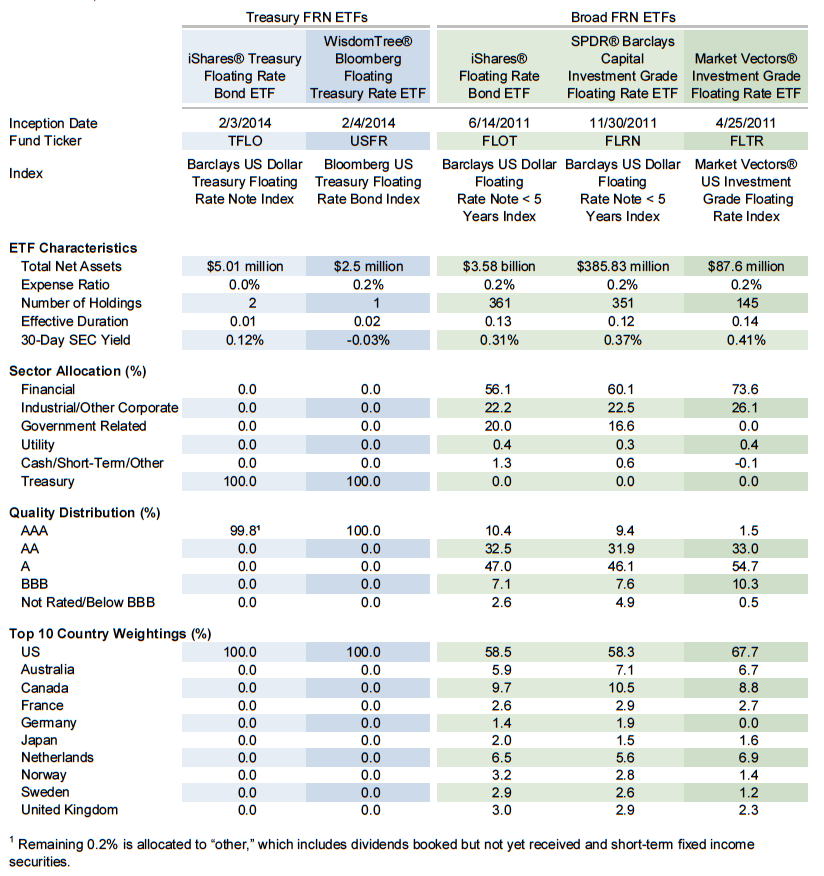

The Barclays Treasury FRN Index is priced very close to par and has exhibited very stable price behavior relative to other Barclays bond indexes. However, it is a bit more volatile than the Barclays US Floating Rate Note Index owing to its lack of diversification (it contains only two securities at this writing) and to the weekly reset feature of the underlying index (Figure 3). The Bloomberg Treasury FRN Index generally tracks the Barclays Treasury FRN Index closely. As for exchange-traded funds (ETFs), WisdomTree will benchmark its WisdomTree Bloomberg Floating Treasury Rate Fund ETF, which trades on the NYSE, against the Bloomberg Treasury FRN Index. iShares will use the Barclays Treasury FRN Index as the benchmark for its iShares Treasury Floating Rate Bond ETF. A comparison of these two new ETFs with three ETFs for non-Treasury floating rate notes (Figure 7) shows the same differences in the underlying assets reflected in Figure 6. Both ETFs are still tiny, with available data showing the iShares ETF with $5.0 million in assets and WisdomTree with $2.5 million. A third ETF provider has filed for a Treasury FRN ETF to be based on the Barclays index, but continues to assess demand from prospective investors.

Figure 7. Floating Rate Note ETFs

As of June 30, 2014

Conclusion

By almost all visible measures, the launch of this new security has been a successful venture for Treasury. Issuance is at the high end of expectations, the auctions have gone smoothly, pricing has been tighter than predicted, and investor interest appears to be as anticipated. Moreover, all this has occurred during a period in which the yield on the ten-year Treasury has declined. On the demand side, one area to watch is whether the ETF market for Treasury FRNs develops in parallel with the market itself, or if investors will be content to invest directly in one or more notes. And on the supply side, it remains to be seen if the Treasury will eventually extend the maturity of the FRNs it issues from two years to five or even ten years. But, it is already clear that Treasury FRNs have become an important offering among the panoply of securities used to finance the US government, and will likely be of particular interest to long-term investors in periods of actual or anticipated increases in interest rates.

Contributors

Sandy Smith, Managing Director

Seth Hurwitz, Managing Director

Alexandra Meyer, Senior Investment Associate

Exhibit Notes

Bid-to-Cover Ratios of Selected Treasury Issues at 2014 Auction Dates

Source: Bloomberg L.P.

Treasury FRN Auction Results and Pricing

Source: US Department of Treasury.

Yield Comparison

Sources: Barclays and Thomson Reuters Datastream.

Notes: Data are daily. Barclays indexes reflect yield-to-worst. The 91-day T-bill reflects bond equivalent yields.

Annual US Issuance of Floating Rate Notes

Source: Securities Industry and Financial Markets Association (SIFMA).

Notes: Floating rate note total includes callable and non-callable bonds. Data for 2014 through June 30.

Auction Allotments by Investor Class for Two-Year Treasury Floating Rate Notes

Source: US Treasury.

Note: The Federal Reserve Banks’ System Open Market Account and Depository Institutions are not included as they have an auction allotment of less than 0.1%.

Floating Rate Note Indexes

Sources: Barclays, Bloomberg L.P., J.P. Morgan Securities, Inc., and Van Eck Global.

Notes: Totals may not sum to 100% due to rounding. J.P. Morgan’s 62.0% financial sector allocation includes 19% to US banks; 29% to Yankee Banks; 14% to financial services; and 1% to insurance. Market Vectors’ 27.7% industrial/other corporate sector allocation includes 6% to communications; 5% to technology; 9% to energy; 3% to consumer, non-cyclical; 2% to consumer, cyclical; 0.4% to basic materials; and 0.5% to industrial. Barclays quality distribution is based on Moody’s ratings, J.P. Morgan on S&P ratings, and Bloomberg and Market Vectors on an evenly weighted blend of DBRS, Fitch, Moody’s, and S&P ratings.

Floating Rate Note ETFs

Sources: Barclays, Bloomberg L.P., iShares, Morningstar, SSGA, WisdomTree, and Van Eck Global.

Notes: ETF characteristics data are as of dates between June 30 and July 10. SPDR expense ratio is gross. Sector allocations for SPDR ETF as of March 31. Totals may not sum to 100% due to rounding. Market Vectors’ 26.1% industrial/other corporate sector allocation includes 6.9% to communications; 5.7% to technology; 8.4% to energy; 2.7% to consumer, non-cyclical; 1.6% to consumer, cyclical; 0.6% to basic materials; and 0.2% to industrial. iShares ETF quality distribution is based on S&P Ratings, SPDR on Moody’s ratings, and Market Vectors and WisdomTree on an evenly weighted blend of DBRS, Fitch, Moody’s, and S&P ratings.

Footnotes