Over periods of prolonged prosperity, the economy transits from financial relations that make for a stable system to financial relations that make for an unstable system.

—Hyman Minsky, “The Financial Instability Hypothesis,” May 1992

Stability Is Destabilizing

—Minsky T-shirt

Over the past several years, one of the most interesting market developments has been the virtual absence of volatility despite a steady stream of high-profile events that would, in prior periods, likely have led to significant market turmoil. However, in recent months this preternatural calm has begun to crack, as a number of asset classes have suffered violent bouts of paroxysm, often on little or no news.

We would trace both these developments to the extraordinary measures undertaken by global central banks to “manage” markets (and by extension the economy). Such measures have the effect of suppressing volatility for long stretches of time, as investors come not only to expect and rely on central banks to “rescue” markets when things get bumpy, but also to sow the seeds for sudden eruptions of volatility. Once everyone has come to rely on said measures, they are by definition positioned much the same, and thus small events—or even no event at all—can lead to mass selling or buying.

Indeed, market history is replete with such events: the 1929 and 1987 equity market crashes, the 1986 collapse in oil (when the price dropped some 67% in a mere four months), the 1997 Asian crisis and 1998 Russian/LTCM crisis, the 2000 tech crash, and the 2008 global financial crisis. This is, of course, a highly selective list—we could, for example, also include 1914, when global bond and equity markets traded serenely right up until the point they closed for several months—but the point is that in each case, while the problems that unfolded seem obvious in retrospect, prior to things coming unglued the majority of investors saw blue skies ahead.

There is, unfortunately, little way to protect one’s portfolio against this type of environment. While it now seems clear, for example, that oil prices at $100/barrel were vulnerable to a sharp price decline, we know of no one who predicted the rout in advance. In fact, many observers—ourselves included—were at the time more worried about the price of US equities, which have since risen to record levels as oil prices have sunk.

The best defense, in our view, is to maintain a portfolio diversified among different economic bases of return—high-yield bonds and equities, for example, are classified as separate asset classes, but offer similar risk-reward exposures—and rebalance assiduously. Since one cannot know how long such periods of calm will last, nor how far the eventual crack-up will go, it seems best to hedge one’s bets by spreading risk around and not letting exposures stray too far from targets.

Stable … Until It’s Not

There have been at least three high-profile examples of volatility exploding in a previously quiescent asset in recent months:

- Oil prices

- The October 15 “flash crash” in US Treasuries

- The Swiss National Bank’s (SNB) January 15 removal of the CHF/EUR “floor”

For additional context, please see Sean McLaughlin et al., Oil Prices Can’t Find Their Footing, Even Amid Geopolitical Turmoil, Cambridge Associates Research Brief, October 30, 2014.

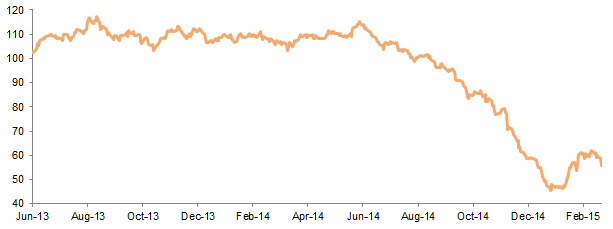

The collapse in oil prices (Figure 1) has been arguably the biggest market event since the global financial crisis. And yet, not only did no one predict it (that we know of), but even once people started paying attention to the decline in late summer, virtually everyone was shocked at how quickly it escalated. Even now there is no agreed-upon explanation for the decline—among the theories are that the Saudis caused it (either to shut down US fracking or to punish Russia, or both), it represents a supply shock caused by fracking, it is a market reaction to secular shifts in supply and demand, and that it is a harbinger, à la 2008, of a coming global economic slowdown/collapse.

Figure 1. Brent Crude Oil Price

June 30, 2014 – March 10, 2015 • US$ per Barrel

Similarly, while the October flash-crash in US Treasuries (Figure 2) continues to spawn explanatory theories—including that it was an epic short squeeze caused by deflationary data and Ebola fears, it was caused and/or exacerbated by new regulatory restrictions imposed by the Dodd-Frank Act and the Basel III Accords, and that high-frequency traders “did it”—none of them seem completely satisfactory.

Figure 2. Ten-Year US Government Bond Yields

October 8, 2014 – October 22, 2014

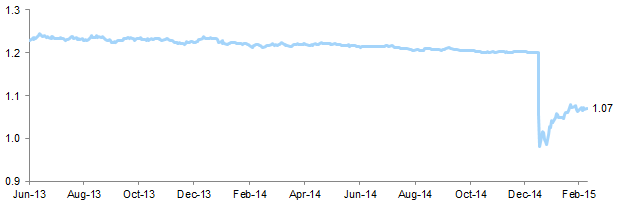

The SNB’s removal of the CHF/EUR floor (Figure 3), meanwhile, took virtually everyone[1]With the notable exception of Jim Grant, editor of Grant’s Interest Rate Observer, who predicted just such an outcome in a September 19, 2014, piece “The Balance Sheet That Ate Switzerland.” by surprise, partly because it came a mere two days after SNB Vice President Jean-Pierre Danthine said the floor “must remain the pillar of our monetary policy.” Anecdotally, we heard of several hedge funds that had put on a trade (basically a modified put spread) when the floor was first announced in September 2011, where they were short the CHF/EUR pair at €1.20, and long two times as much at €1.17, based on the expectation that while the floor would hold for a while, it would eventually break in dramatic fashion. Unfortunately most of them eventually grew tired of holding (and paying for) the position.

Figure 3. Foreign Exchange Rates: Swiss Franc/Euro

June 30, 2013 – March 10, 2015

The common theme among these events, of course, is that all represented very significant, violent moves in major asset classes that were somewhat understandable in retrospect, but which few saw coming beforehand. Further, all have an element of government involvement, both in the initial stability and the subsequent volatility.

What’s Next?

The obvious question is what asset class looks similar to the others prior to their comeuppance. Unfortunately this is easier asked than answered. Investor reaction—or perhaps lack of reaction would be a better term—to the current Greek “crisis” is instructive in this regard. One wag tagged it “the world’s most boring crisis,” and it is hard to argue the point, as weeks of breathless commentary about the imminent dissolution of the European Union and/or collapse of the Greek economy was met by … mostly yawns. Indeed, as of late February the best-performing asset class in the world year-to-date was Greek government debt, despite the absence of any real progress on reforms.

One fairly obvious candidate for a sudden bout of volatility would be equities, and particularly the US equity market, which has (measured by the S&P 500) now gone nearly three-and-a-half years without a 10% drop, the third-longest stretch in our post-1927 dataset (Figure 4). Given that the top two periods were the 1990–97 and 2003–07 rallies, one might ask whether this means equity markets have become more resilient in recent years … or whether investors should brace for another 1997–98 or 2008–09 type event. Or perhaps, à la Hyman Minsky, the former will bring about the latter.

Figure 4. Longest Number of Days Without a 10% Drop in the S&P 500

February 20, 1928 – February 26, 2015

In fact, US equities have bounced back so strongly from their recent drops (in October and January) that it seems many investors see any decline, no matter how brief, as an opportunity to buy. Again, this could be interpreted two ways, and is what makes predicting a sudden outbreak of volatility so difficult; one must be right not only on the particulars—as, for example with the hedge funds betting on the breaking of the CHF/EUR floor—but also on the timing.

The Bottom Line

It certainly appears that the recent era of low volatility is coming to a close, as a number of quiescent asset classes have suffered sudden outbreaks of volatility for what remain obscure reasons. This seems likely to continue, particularly given the fact that so many investors remain on similar sides of the boat thanks to the promise of virtually endless central bank interventions.

That said, investors are on the same side for good reason—those that have, for example, aggressively bought US equity dips over the past few years have been handsomely rewarded. The same is true for many other asset classes, including high-yield bonds, peripheral European debt, and even US Treasuries.

In sum, many markets are likely less stable than they appear, but predicting when this will matter is a fool’s errand. The best approach is to remain diversified among assets with different economic bases of return, and rebalance back to policy targets frequently and assiduously.

Contributors

Eric Winig, Managing Director

Alex Jones, Senior Investment Associate

Michelle Wu, Investment Associate

Exhibit Notes

Brent Crude Oil Price

Source: Thomson Reuters Datastream.

Note: Data are daily.

Ten-Year US Government Bond Yields

Sources: Federal Reserve and Thomson Reuters Datastream.

Note: Please note that 10/11/14 and 10/12/14 are excluded.

Foreign Exchange Rates: Swiss Franc/Euro

Source: Thomson Reuters Datastream.

Note: Data are daily.

Longest Number of Days Without a 10% Drop in the S&P 500

Source: Ned Davis Research, Inc.

Note: From April 2, 2012, to June 1, 2012, the S&P 500 fell 9.6% on a total return basis (9.9% on a price return basis). Starting the count from June 2, 2012, the current cycle has lasted 999 days through February 26, 2015.

Footnotes