Michael Lewis’ new book Flash Boys has sparked a fierce debate on the practice known as high-frequency trading (HFT), with Lewis and his supporters claiming markets are “rigged” by high-frequency traders who front-run other market participants and engage in a number of other unsavory activities.

Unfortunately the truth is more mundane. HFT—the name given to organizations that employ superfast[1]For example, in one millisecond (a thousandth of a second), the most actively traded stocks can reportedly experience roughly 500 quote changes and 150 trades. computer algorithms that allow their traders to “make” markets in equities (i.e., stand ready to buy and sell from other investors at any given time)—has been in existence for more than 20 years, but has become ubiquitous in recent years, spurred on in the United States by Regulation National Market System (Reg NMS), passed in 2005, which established the National Best Bid and Offer (NBBO), requiring that investors receive the best price available across all exchanges for their order. As with any innovation, there are pros and cons and winners and losers, but in our view the (largely realized) benefits of HFT outweigh the (mostly theoretical) negatives.

In fact, Lewis’ book does much to discredit his theory. Flash Boys opens with a story about a trader who spent upwards of $300 million constructing a super-secret fiber-optic tunnel from Chicago to New York to shave tiny fractions of a second off his execution time, so he could arbitrage market variances faster than others. This is presented as vaguely nefarious and obviously unfair. However, the book closes with a mystery of sorts—it appears someone is now using microwave signals to send data even faster than the tunnel! Or as Lewis puts it, “another incredible but true Wall Street story of hypocrisy and secrecy and the endless quest by human beings to gain a certain edge in an uncertain world” [emphasis added]. In other words, when we strip away the Lewis hyperbole, the real story is that rapidly advancing technology may have already rendered the tunnel obsolete.

HFT Benefits

Broadly speaking, HFT has made markets deeper and more efficient, driving down costs for the majority of investors by compressing bid/offer spreads and vastly increasing execution speeds. In simple terms, most trades are now completed faster, with tighter spreads, than ever before, thus benefiting individual investors who buy and sell in reasonably small sizes. The relative losers, meanwhile, are big institutional traders who need to buy and sell large blocks of stock; however, such trades have always been difficult to complete.

In terms of the general functioning of equity markets on a day-to-day basis, it is hard to argue HFT has been anything but a boon.

HFT Problems and Risks

The negatives most often brought up with regard to HFT are, first, that these traders engage in behavior designed mainly to profit from their speed advantages, as opposed to operating as liquidity providers, and second, that HFT’s very nature actually makes markets less stable, and could prove extremely disruptive during a period of market volatility.

The most notable charge with regard to the first is high-frequency traders’ capacity to “see” a large order at one exchange and then race ahead to other exchanges, buy up available stock, and sell it to the original buyer at a (very small) profit. Another variant on this theme is “spoofing,” in which high-frequency traders place “phantom” bids and offers to affect other prices, but pull them before any trades can be transacted. High-frequency traders also compete with “quant” funds in a variety of strategies such as momentum and trading on news headlines.

High-Frequency Trading Strategies

We agree such activities do not appear to be “useful” … but so what? Most traders in markets (indeed, most firms under a capitalist system) are primarily interested in finding an edge over others in their field. As with most “useful” inventions, the liquidity provided by high-frequency traders arose as a consequence of their profit-seeking, not from some selfless sense of public service.[2]The founders of IEX are in fact portrayed as having precisely these public-spirited motives in Flash Boys, and for all we know this is accurate. But if true, we would view it as the exception that … Continue reading

Two additional points are worth noting. First, such activities have been around as long as markets—Nathan Rothschild’s brilliant use of his early knowledge of the outcome of the Battle of Waterloo being perhaps the most famous example of the importance of speed—and second, so far as we or anyone else is aware,[3]As of this writing several investigations have been launched into HFT, but no one has been charged with a crime. everything high-frequency traders do is not only within the letter of the law, but most of their activities were actively encouraged by Reg NMS and NBBO. As Joseph Saluzzi and Sal Arnuk put it in their book Broken Markets, “Reg NMS commoditized trading destinations. Speed of execution became paramount.”[4]While the authors speculate that interested parties were instrumental in crafting the legislation to achieve this goal—as they put it, “you can’t help but wonder whether the changed market … Continue reading

What About the Next Crash?

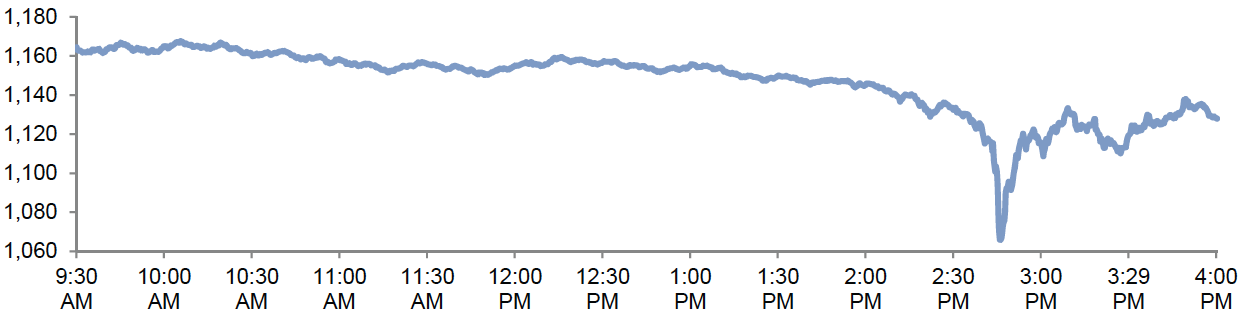

Some have also argued that while high-frequency traders typically function as liquidity providers in “normal” markets, they will actually turn around and drain liquidity in the next market panic. And the prospect of rogue computers crashing markets is one which must be taken seriously. The May 6, 2010, “flash crash” has never been satisfactorily explained, and many have rightly pointed out that it would likely have had more serious effects had it occurred toward the market close rather than in the middle of the day.

Flash Crash: S&P 500 Index Level on May 6, 2010

However, such risks seem no greater than those posed by, for example, “quant” strategies, momentum traders, or even good old human panic (see 1929 and 1987). Finally, the complaint that the liquidity provided by high-frequency traders is ephemeral (i.e., that they will vanish in a market panic) seems to us to miss the point—all liquidity is ephemeral. As one observer quipped, “During the 1987 crash the NYSE specialist wasn’t standing on the floor of the exchange; he was hiding in the bathroom.”

HFT acquitted itself very well during the 2008 crash; equity market liquidity was remarkably strong during this period, with few instances of “bids wanted” such as those seen in prior panics. While past need not be prologue—and again, we agree HFT could play a role in a future crash—2008 must be counted a success for HFT.

Fighting the Last War

Much of the outrage over HFT appears to stem from the perception that such trading is a growing influence on markets, with profits to match. But the numbers tell a much different story. According to one widely cited study from Rosenblatt Securities, high-frequency traders’ share of US equity trades has fallen over the past few years from roughly two-thirds to about half, and their daily trade volume has fallen from 3.25 billion shares a day in 2009 to about 1.6 billion in 2012. Average profits, meanwhile, have fallen from about a tenth of a penny per share to a twentieth of a penny, with profits for the entire HFT industry plunging from $4.9 billion in 2009 to $810 million in 2012.

None of this is particularly surprising given the nature of competition and the formerly easy profits made by high-frequency traders.

The Bottom Line

High-frequency traders have driven down costs for the majority of investors by making markets deeper and spreads tighter. While some also engage in behavior designed for their own profit, such activities are not only perfectly legal, but were mainly developed as a direct response to recent regulations; profits, meanwhile, appear to be shriveling as competition erodes the advantage of first movers.

Worries about HFT causing or contributing to another crash are legitimate, but must also be weighed in comparison both to the prior state of the system—which did not prevent or seemingly even mitigate crashes—and the plethora of other risks inherent in markets today, be they unprecedented central bank policy, geopolitical risk … or simply high valuations stacked on historically wide profit margins.

Contributors

Eric Winig, Managing Director

Ramin Sobhany, Investment Associate

Exhibit Notes

High-Frequency Trading Strategies

Sources: Blackrock and Securities Exchange Commission.

Flash Crash: S&P 500 Index Level on May 6, 2010

Source: Tick Data.

Footnotes