Most endowed institutions seek to provide continued (or growing) financial support for their operations while at the same time preserving the endowment’s value for the future. At its core, a spending policy is designed to balance the needs of both current and future generations, though getting the right balance can be a challenge. The precipitous decline of markets in 2008 and continued economic uncertainty have pushed institutions to reconsider how to properly maintain intergenerational equity. Our 2010 report, The Sober Future of Endowment Spending, explored the challenge of supporting a typical 5% spending rate given asset returns and urged institutions to develop spending contingency plans.

In 2012, we surveyed institutions on a variety of spending topics including spending rule types, target spending rates, floors, caps, collars, treatment of gifts, and recent policy changes under consideration. This report is a follow up to that study, incorporating spending policy practices in 2013, as well as information on endowment reliance and support of operations. We received survey responses from 190 institutions including 134 colleges and universities; 28 cultural and environmental institutions; 19 independent schools; and nine other nonprofit institution types (Exhibit 1). Foundations were excluded from the survey group as their spending policies are influenced by government regulations.

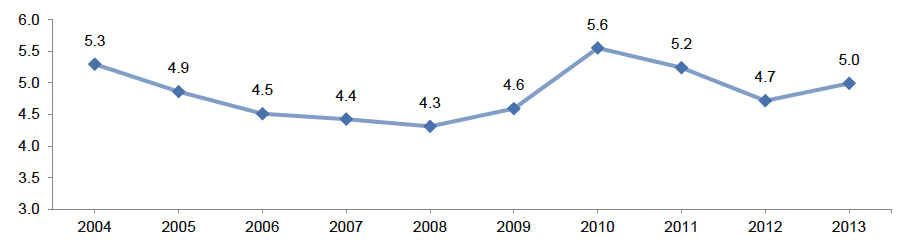

Mean Annual Effective Spending Rate

2004–13

Source: Spending policy data as reported to Cambridge Associates LLC.

Note: Data represent the average of 115 institutions that provided effective spending rates for each year from 2004 to 2013.

Exhibit 1: Profile of Participating Institutions

2013

Source: Spending policy data as reported to Cambridge Associates LLC.

Spending Policy Types

Exhibits 2–5 show summary responses to our questions on spending policy types. The three most common spending policies can be broadly characterized as market value–based policies, constant growth policies, and hybrid policies.

Market Value–Based Policies

The majority (72%) of responding institutions use a market value–based policy, which dictates spending a percentage of a moving average of endowment market values (Exhibit 2). The majority of institutions (87%) citing this rule type use a prespecified target rate while the remaining institutions allow some discretion by setting a prespecified percentage range within which the target spending rate may fall. For the purposes of analyzing target spending rates, the midpoint is used for institutions that specified a discretionary range. A target spending rate of 5% was used by 43% of institutions with a market value–based policy. A nearly equal proportion of institutions (40%) use a target rate below 5% while the remaining institutions use a rate above 5% (Exhibit 3).

Exhibit 2: Spending Policy Types

2013

Source: Spending policy data as reported to Cambridge Associates LLC.

Notes: Market value–based spending policies base spending on a prespecified percentage of a moving average of market values. Constant growth policies increase prior year’s spending by a prespecified percentage. Hybrid policies are those that incorporate a weighted average of a constant growth rule and a percentage of market value rule. “Other” policies are those that cannot be classified as market value–based, constant growth, or hybrid policies.

Exhibit 3: Characteristics of Market Value–Based Spending Policies

2013

Source: Spending policy data as reported to Cambridge Associates LLC.

Notes: Market value–based spending policies base spending on a prespecified percentage of a moving average of market values. Graph reflects data for the 134 institutions that provided detailed data on their target spending rate. If a range was provided, the target spending rate was calculated using the midpoint of the range.

Exhibit 3 (continued). Characteristics of Market Value–Based Spending Policies

2013

Source: Spending policy data as reported to Cambridge Associates LLC.

Notes: Market value–based spending policies base spending on a prespecified percentage of a moving average of market values. Unit of time measurement indicates whether spending is calculated using monthly, quarterly, or yearly market values. Graph reflects data for the 130 institutions using a market value–based spending policy that provided the unit of time measurement in their spending calculation.

Institutions employ a variety of smoothing periods to determine the average endowment market value used in the spending calculation. Smoothing periods range from one to seven years and the time interval (i.e., monthly, quarterly, or annual market values) can vary (Exhibit 3). The most common unit of time measurement is 12 quarters (45% of those with a market value–based policy).

Despite the smoothed average market value component, there is a risk that the policy calculation would dictate a spending cut during prolonged periods of endowment value declines. Cutting endowment spending can be difficult during market downturns, as they often coincide with an economic environment where other revenue sources of the institution are at risk of weakening. This may be particularly problematic for institutions with high fixed costs. A floor that prevents spending from falling below the prior year’s dollar amount would ease budgetary concerns during these periods, but at the cost of reducing the likelihood that purchasing power will be preserved over the long term. Using a cap along with a floor, however, can better balance the impact on future generations by limiting spending increases when endowment growth is particularly strong. Only nine of the 136 institutions that spend a prespecified target rate use a floor and/or a cap to further contain spending during volatile periods (Exhibit 3).

An additional 17 institutions are allowed to set a rate within a discretionary range of percentages and have more flexibility to maintain the level of spending in down markets and contain spending increases when endowment growth rates are high.

Constant Growth Policies

Constant growth spending policies increase the prior year’s spending amount by a measure of inflation and/or a prespecified percentage. Twenty-two respondents (12%) have a constant growth spending policy (Exhibit 2). Of these 22 institutions, 11 use a prespecified percentage growth rate; eight, an inflation-index growth rate; and three, an inflation-index growth rate plus a prespecified percentage (Exhibit 4).

Exhibit 4: Characteristics of Constant Growth Spending Policies

2013

Source: Spending policy data as reported to Cambridge Associates LLC.

Note: Constant growth policies increase prior year’s spending by a prespecified percentage.

The great advantage of a constant growth policy is the predictable spending stream from the endowment to the institution; however, constant growth policies have notable shortcomings. Increasing spending during prolonged periods of asset declines risks permanent impairment of the endowment. Conversely, some endowment constituencies might protest if they perceive the fund as grossly underspending in periods when it earns exceptional returns. In practice, institutions with constant growth spending policies mitigate these concerns and moderate spending by imposing a spending cap and floor based on a percentage of market value, or a moving average of market values (Exhibit 4).

Hybrid Policies

Hybrid spending policies are used by 25 responding institutions, or 13% (Exhibit 2). This policy type blends the predictable spending element of a constant growth policy with the asset preservation principle of a market value–based policy and allows an institution to set the appropriate mix that best meets its needs. Hybrid spending policies essentially have the effect of spending a prespecified percentage of an exponentially weighted average market value. The rule is expressed as a weighted average of a constant growth rule and a percentage-of-market-value (or average market value over a period of time) rule, with the greater weighting usually applied to the constant growth component. A plurality of respondents (48%) assign a 70% weighting to the constant growth portion and a 30% weighting to the market value–based portion. Inputs to the calculation of both the constant growth and market value–based components are shown in Exhibit 5.

Exhibit 5: Characteristics of Hybrid Spending Policies

2013

Source: Spending policy data as reported to Cambridge Associates LLC.

Notes: Hybrid policies essentially have the effect of spending a prespecified percentage of an exponentially weighted average market value (MV). The rule is expressed as a weighted average of a constant growth policy and a percentage of market value policy. Of the 25 institutions that use a hybrid spending policy, 19 do not use a collar, cap, or floor to contain year-to-year spending.

Exhibit 5 (continued): Characteristics of Hybrid Spending Policies

2013

Recent and Contemplated Spending Policy Changes

A total of 31 institutions are considering future changes to their spending policy. Most respondents indicated that changes would be made to spending rule mechanics (e.g., change the prespecified spending rate, institute a cap, etc.), with a smaller percentage (19%) considering changing their spending rule type (Exhibit 6).

Exhibit 6: Future Changes to Spending Policies

2014 and Beyond

Source: Spending policy data as reported to Cambridge Associates LLC.

For institutions that provided data, the most common changes being made or under consideration are changes to the target spending rates or discretionary target spending ranges of market value–based policies. Of the 11 institutions that have approved changes to their target rate or discretionary range, seven decreased the target spending rate, one is lowering the ceiling of its discretionary range, and one is transitioning from a discretionary range to a lower target spending rate. Two institutions did not indicate whether the changes under consideration would increase or decrease the rate. In all cases where lower target rates have been implemented or are under consideration, the new target rate would be at 5% or below.

Additional changes that have been made or are being considered include changes to market value smoothing periods, spending caps and floors, and other components of policy.

Effective Spending Rates and Support of Operations

Annual spending distributions are withdrawn from endowment assets to fund a variety of expenses including supplementing student financial aid, covering operating expenses, or funding capital projects. Spending distributions are also used to cover administrative costs, investment oversight costs, and to service outstanding debt. The effective spending rate in this study is calculated as the annual spending distribution as a percentage of the beginning market value of the long-term investment portfolio.

For the 115 institutions that provided effective spending rates over the trailing ten-year period, rates averaged 5.0% in 2013. As the graph below shows, the average effective spending rate was 27 bps above 2012, but below the rates reported in 2010 and 2011.

Support of Operations. The range of long-term investment portfolio support varies considerably among the institutions in this study. Public college and university institutions, which generally receive substantial financial support from state appropriations, generally rely less on endowment payout to fund the operating budget compared to private college and university institutions and other nonprofits. For the 30 public college and university institutions that provided data, support from the long-term investment portfolio as a percentage of operating expenses averaged 2.8% in 2013. Average support for private colleges and university institutions was 15.2% (Exhibit 7).

Exhibit 7: Long-Term Investment Portfolio (LTIP) Support of Operations

2013

Source: Spending policy data as reported to Cambridge Associates LLC.

Note: LTIP support of operations is the proportion of the operating budget that is funded from LTIP payout. For the four other nonprofit institutions that provided data, the LTIP support of operations averaged 17.1%.

Among cultural and environmental institutions and independent schools, reliance on the long-term investment portfolio is higher, as support of the operating budget averaged 33.5% and 26.3%, respectively. Although some institutions’ reliance on long-term investment portfolio support is low, for others, it is the single largest source of revenue.

Participating Institutions

Colleges and Universities

Allegheny College

American University

Amherst College

Baylor University

Bentley University

Berkeley Endowment Management Company

Boston College

Bowdoin College

Brandeis University

Brown University

Bryant University

Bryn Mawr College

University of California

California Institute of Technology

Carleton College

Carnegie Mellon University

Case Western Reserve University

Chapman University

The University of Chicago

The City University of New York

Claremont McKenna College

Clemson University Foundation

Colby College

Colgate University

Columbia University

Connecticut College

Cornell University

Dartmouth College

Davidson College

University of Delaware

Duke University

Emory & Henry College

Emory University

Florida State University Foundation Inc.

University of Florida Investment Corporation

Georgetown University

The George Washington University

Georgia Tech Foundation Inc.

Gettysburg College

Goucher College

Grand Valley State University

Hampton University

Harvard Management Company, Inc.

Harvey Mudd College

Haverford College

University of Hawaii Foundation

College of the Holy Cross

Hope College

Houston Baptist University

University of Illinois Foundation

Indiana University Foundation

Johns Hopkins University

Kalamazoo College

Kansas State University Foundation

KU Endowment

Lafayette College

Lebanese American University

Lehigh University

Lewis and Clark College

University of Louisville

Lycoming College

Macalester College

University of Maine Foundation

Maryland Institute College of Art

University of Miami

University of Michigan

Michigan State University

MIT Investment Management Company

Mount Holyoke College

Nevada System of Higher Education

New York University

Northeastern University

Northwestern University

Norwich University

University of Notre Dame

Oberlin College

Occidental College

Ohio State University

University of Oklahoma Foundation

Oklahoma State University Foundation

University of Oregon Foundation

Oregon Health and Science University Foundation

University of Pennsylvania

Pennsylvania State University

Pepperdine University

University of Pittsburgh

Princeton University

The Principia Corporation

Providence College

Purdue University

Randolph-Macon College

Rensselaer Polytechnic Institute

University of Rhode Island Foundation

Rice University

University of Rochester

The Rockefeller University

Roger Williams University

College of Saint Benedict

University of San Diego

Santa Clara University

Scripps College

Siena College

Simmons College

University of Southern California

Spelman College

Stanford University

University of St. Thomas

Swarthmore College

Temple University

University of Tennessee

Texas A&M Foundation

The University of Texas Investment Management Company

University of Toronto Asset Management Corporation

Trinity University

The UCLA Foundation

UNCG Endowment Partners, LP

UNC Management Company, Inc.

Vanderbilt University

The University of Vermont

Villanova University

University of Virginia

Virginia Tech Foundation

University of Washington

Washington College

Washington and Jefferson College

Washington University in St. Louis

Wellesley College

Wesleyan University

Western New England University

Wheelock College

College of William & Mary Foundation

Williams College

Yale University

Yeshiva University

Cultural and Environmental

Atlanta Historical Society

The Vivian Beaumont Theater, Inc.

Boston Symphony Orchestra Inc.

The Brookings Institution

California Academy of Sciences

Chemical Heritage Foundation

Cypress Lawn Endowment Care Trust

The Edison Institute

Isabella Stewart Gardner Museum

Hagley Museum and Library

Linda Hall Library Trusts

Honolulu Museum of Art

Indianapolis Museum of Art Inc.

Kennedy Center for the Performing Arts

Longwood Gardens, Inc.

Minnesota Orchestral Association

Museum of Fine Arts, Boston

Museum of Fine Arts, Houston

National Geographic Society

The New York Public Library

Philadelphia Museum of Art

Santa Fe Opera Foundation

Scenic Hudson Land Trust Inc.

The School of American Ballet

Seattle Art Museum

George Washington’s Mount Vernon

White House Historical Association – Endowment Trust

The Henry Francis duPont Winterthur Museum, Inc.

Independent Schools

Auditory Learning Foundation

Brunswick School

Buckingham Browne & Nichols School

Hockaday School

The Hotchkiss School

Kamehameha Schools

Lakeside School

The Lawrenceville School

The Loomis Institute

The Madeira School

Park Tudor Trust

Phillips Exeter Academy

Pingry School

The Roxbury Latin School

Salisbury School

Shady Hill School

The Webb Schools

Western Reserve Academy

The Winsor School

Other Nonprofits

American College of Surgeons

American Red Cross

Armenian Church Endowment Fund

Catholic Church Extension Society

The First Church of Christ Scientist

Billy Graham Evangelistic Association

Mission Diocese Fund

Old South Church

Xaverian Brothers USA

Contributors

Jeremy Parsels, Manager

Grant Steele, Director