In this Edition

- Regulators across the globe begin developing requirements for dark pools trading systems

- US regulators discourage highly leveraged transactions by banks

- OTC derivatives rules continue to roll out in the US and Europe

- FATCA’s debut means more paperwork for funds, investors, and financial institutions

Come into the Light

Dark pools get more scrutiny even as global regulators look at changing market structure

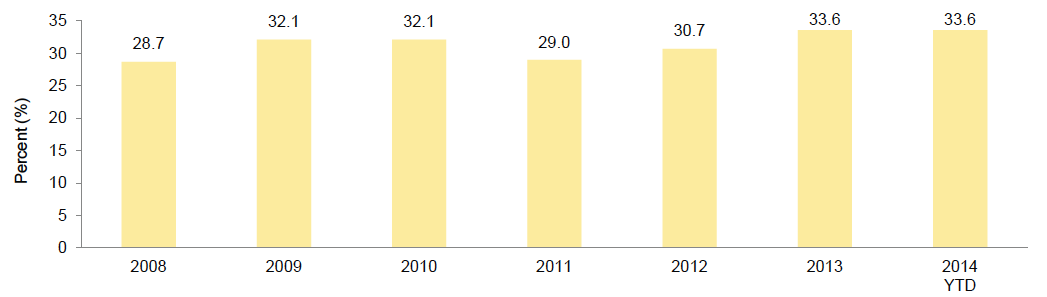

In June, the US Financial Industry Regulatory Authority (FINRA) announced that it would be making dark pool trading volume information available to the public in a bid to improve investor confidence. Dark pools are off-exchange trading systems that have grown significantly over the last decade and off-exchange trading more broadly is thought to now make up about one-third of trading volume in the United States (Figure 1). The pools allow participants to transact privately, thereby avoiding market impact and allowing participants to avoid exchange fees. While these are benefits to investors, global regulators and others are increasingly raising questions about the pools’ pricing policies, the level of transparency, brokers’ incentives to use the pools, and the impact on pricing on “lit” exchanges.

Figure 1. US Off-Exchange Volumes as a Percentage of Total US Volume

2008–14

Source: Bloomberg L.P.

Note: Data for 2014 are through June 30.

In the United States, trades are required to be executed at the best available bid or offer, whether on or off exchange, and prices are fed into a consolidated tape. Despite this, regulators have identified issues with dark pool pricing lagging the market, resulting in losses to investors. A lack of transparency is also at the heart of a lawsuit by New York State officials who charged a dark pool operator with lying to buy-side customers about the prevalence of high-speed traders in its pool as well as with allocating virtually all trades to its pool regardless of pricing. Regulators have stepped up the pressure with calls for further investigation of dark pools and for more transparency. In addition to FINRA’s announcement, SEC Chair Mary Jo White announced in June that SEC staff was working on rules to require the pools to disclose how they operate. And some market commentators note that the SEC may consider a requirement that the dark pools execute trades only if the price is better than on exchange; this “trade-at” rule is said to be desired by the exchanges.

Outside of the United States, dark pools are thought to make up a smaller part of the market: 10% to 11% in the European Union by one estimate, but regulators are concerned about similar issues. Under EU rules, dark pools are not required to report prices to a consolidated tape, increasing pricing opacity. In a bid to push more trades onto exchanges, the pending Europe Markets in Financial Instruments Directive 2 (MiFID 2) includes a proposal that under some circumstances caps the amount of trading by a single platform in any single security. Australian and Canadian regulators have taken a different approach, adopting rules requiring the pools to show that they can provide a better price than the exchanges for smaller trades (similar to the “trade-at” approach) while allowing block trades without a price improvement in an attempt to improve market functioning. Hong Kong officials are said to be considering a similar approach to dark pool regulation in their market.

It’s Too Risky

US regulators tell banks to stop lending

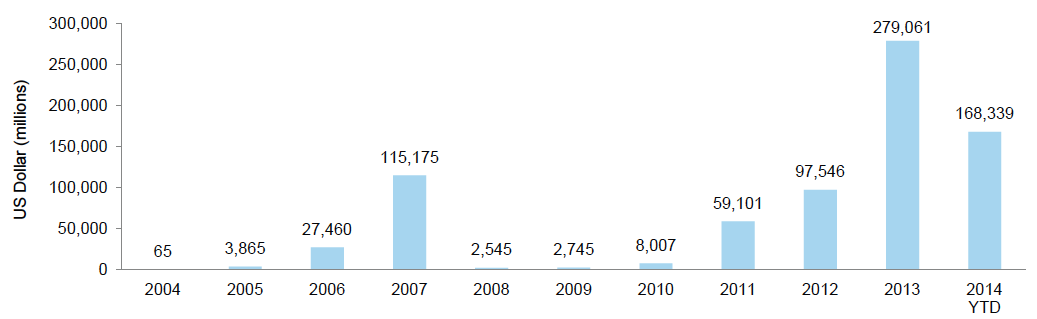

Last year US bank regulators the FDIC, the Federal Reserve, and the Office of the Comptroller of the Currency (OCC) issued guidance intended to encourage banks to reduce their exposure to highly leveraged transactions. In the guidance, regulators discouraged banks from lending to support takeover deals where the company’s debt would exceed 6.0 times EBITDA (earnings before interest, taxes, depreciation, and amortization). More recently, in its semi-annual “risk perspective” report[1]“Semiannual Risk Perspective,” National Risk Committee, Office of the Comptroller of the Currency, Spring 2014., the OCC highlighted its concern with the level of issuance of covenant-lite loans—according to the regulator the volume of new-issue covenant-lite loans in 2013 in the United States approached the total cumulative amount issued from 1997 to 2012. A similar trend can be observed looking at global issuance of dollar-based bonds (Figure 2).

Figure 2. New Issuance of Covenant-Lite Leveraged Loans

2004–14

Sources: BofA Merrill Lynch Global Research and Standard & Poor’s LCD.

Notes: Data for 2014 through June 30. Data reflect global issuers with loans issued in US dollars.

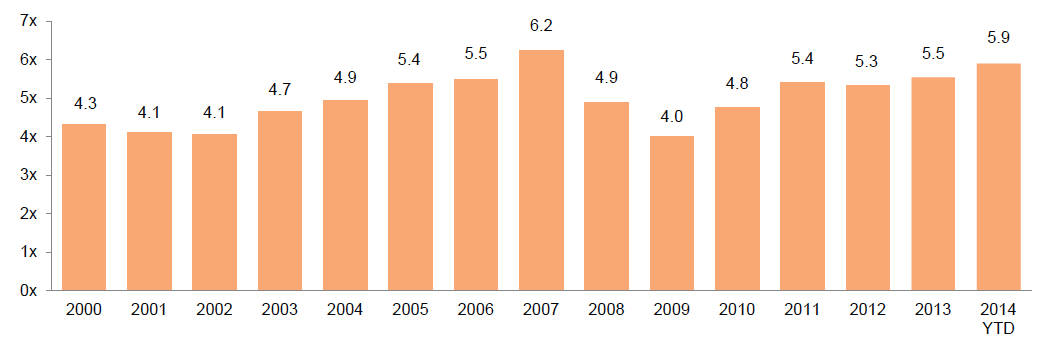

The leveraged loan market has been a significant source of fee revenue to banks, and a strong deal market offers the prospect of continued growth in the revenue stream. Seemingly despite the regulators’ guidance, banks continued to accommodate private equity buyers at deteriorating standards. During 2013 more than a quarter of all new US buyout deals had a debt-to-EBITDA ratio greater than 6x[2]“Banks Sit Out Riskier Deals as Regulators Apply Pressure,” The Wall Street Journal, January 21, 2014. and debt-to-EBITDA for large deals across the market edged up accordingly (Figure 3). Regulators announced earlier this year that underwriting standards appeared to continue to deteriorate during 2014. According to press reports[3]For example, Reuters PE Hub, “Buyout Loan Trends May Reflect Fed, OCC Disparities: TRLPC,” July 2, 2014. during the second quarter, two-thirds of large buyout deals (involving more than $500 million in debt) were higher than the 6x debt-to-EBITDA level targeted by regulators.

Figure 3. US Debt/EBITDA Multiples for Large Corporate LBOs

2000–14

Source: Standard & Poor’s LCD.

Notes: Data for 2014 are through June 30. Defined as issuers with EBITDA of more than $50 million.

Regulators have stepped up the pressure, demanding that banks comply with the standards and threatening fines or other action for those out of compliance. Commentators have noted that the OCC and the Fed have taken different approaches to this issue, with the OCC pursuing the issue more aggressively than the Fed, and that this may have given foreign banks an advantage in underwriting recent deals. As support for this idea, observers point out that the top underwriters for the most recent quarter were all foreign banks, a significant shift in the “league tables” over last year. Credit Suisse, Barclays, and Deutsche Bank took the top-three loan underwriting positions, respectively, for large US corporate leveraged buyout deals in the second quarter, LPC data shows. Another beneficiary: non-bank lenders that are not subject to banking regulator oversight. While several large US banks declined to participate in a recent KKR-led buyout that would have exceeded the 6x leverage guidance, broker-dealer Jefferies Group took a lead role in the financing. Other market participants such as direct lending operations within buyout firms and other private fund managers or publicly traded business development companies stand to gain as well, effectively moving this financing activity into the realm of “shadow banking.”[4]“Henry Kravis, Still Shaking Wall Street, Steers KKR Into Lending,” Bloomberg L.P., June 17, 2014.

Swaps Regulations

The rollout continues with more rules on the horizon both in Europe and the United States

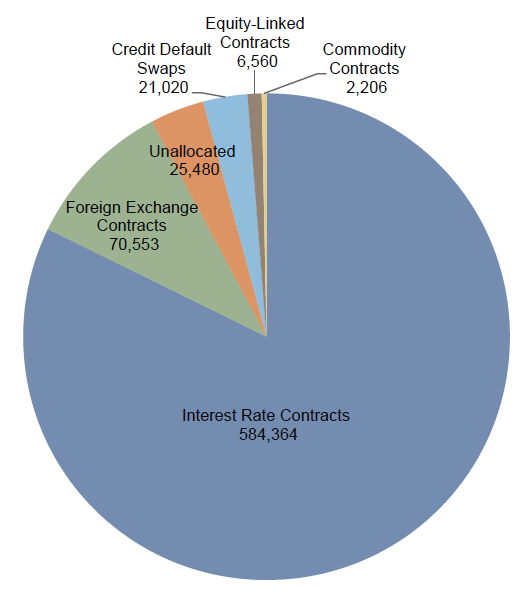

Coming out of the 2008 credit crisis, regulators focused on improved reporting of over-the-counter (OTC) derivatives exposures and on increasing the use of central counterparties as a way to reduce counterparty exposure. In the United States both the SEC and the Commodity Futures Trading Commission (CFTC) have responsibility for the regulation of OTC derivatives. The CFTC is responsible for the lion’s share of these derivatives, with the commodity, credit index, foreign exchange, and rates markets under its supervision. Together, these markets make up the vast majority of all OTC derivatives, a $710 trillion global market (Figure 4). The SEC is responsible for security-based swaps, a much smaller piece of the market. While the new regulatory regime has not been fully implemented, this is an area that is changing rapidly, as new regulations are rolled out and market participants adjust to the new landscape.

Figure 4. Notional Amounts Outstanding:

Global OTC Derivatives Market

As of December 31, 2013 • US Dollar (billions)

Source: Bank for International Settlements.

While the US CFTC has been quite active in rolling out a new regulatory structure for the OTC derivatives under its regulatory umbrella, the SEC has been much slower. During second quarter, the SEC released proposed regulations addressing recordkeeping, notice, and reporting requirements for security-based swaps. The proposed regulations are focused on requirements for registered security-based swaps dealers and major (a defined term) security-based swaps participants and thus should not have a significant near-term impact on other market participants. Nonetheless, this gets the ball rolling for security-based swap regulation in the United States.

Requirements under European Regulation on Derivative Transactions, Central Counterparties, and Trade Repositories (EMIR) continue to be rolled out. In July, the scope of firms required to report derivatives transactions under EMIR will expand. Starting July 22, non-EU-based investment funds managed by EU firms that are authorized under the Alternative Investment Fund Managers Directive (AIFMD) will be subject to EMIR’s reporting obligations. Meanwhile, EU established entities will be subject to additional reporting requirements for OTC and exchange-traded derivatives beginning in early August 2014.

Recently released statistics provided some color on the continuing impact of regulation on the OTC derivatives markets globally. According to the Bank for International Settlements, centrally cleared credit default swaps accounted for 26% of all contracts by year-end 2013, up from less than 10% in 2010. The statistical survey also noted that the use of central counterparties has contributed to reduced counterparty exposure through the prevalence of netting agreements. The Chicago Mercantile Exchange, which offers an alternative to swaps in the form of deliverable swap futures, continues to see interest in the space. It recently announced a product extension into euro rates swaps. Both products are intended to reduce the total margin requirements associated with trading swaps and other futures through risk offsets against other futures and options.

FATCA’s Debut

Sharpen your pencils and get ready to fill out yet more forms

July 1 marked another milestone for implementation of the US Foreign Account Tax and Compliance Act (FATCA). While FATCA became law in 2010, it has proven complex to implement and regulatory deadlines had been repeatedly extended. The July 1 deadline required FATCA-compliant financial institutions to have adopted and implemented new FATCA-compliant account opening procedures. Institutions have phased-in requirements to complete due diligence on existing accountholders beginning at year-end 2014 and extending into 2016 (for small account holders).

What is FATCA? FATCA seeks to reduce tax evasion by identifying and gathering information on US taxpayers that hold non-US accounts. This US law in effect makes foreign financial institutions (FFIs) responsible for compliance in that it imposes an obligation on them to: establish due diligence requirements intended to identify US account holders, report annually regarding US accounts, agree to comply with other Internal Revenue Service (IRS) information requests, and agree to withhold on payments to “recalcitrant” account holders (i.e., FFI owners that will not identify their beneficial owners). To ensure compliance, FATCA imposes a 30% withholding tax on any US-source payments (including gross proceeds, not just net gain) to a non-US entity that does not agree to comply with FATCA’s account identification, reporting, and withholding rules.

FFIs that register with the IRS receive an identification number, called a global intermediary identification number (GIIN), that provides proof of registration to other withholding agents. As of early June, the IRS posted a list of registered FFIs and their GIINs. According to the IRS, withholding agents are permitted to rely on the published FFI list to validate an FFI’s claim of FATCA registration status. For institutions that wish to confirm the registration status of an entity, having their GIIN number appears to be key. While the IRS “search and download tool” allows one to search by entity name, we have found the most efficient way to search is by registration number, given that names of individual entities can be quite similar across an investment platform.

As noted in previous editions of our regulatory update, investors should expect an increased number of document requests from managers and others as everyone adapts to these evolving requirements. And not all of the document requests will be relevant: we have fielded questions from US tax-exempt clients that have received requests from managers for their GIINs. Adding to the complexity: the “crown jewel of FATCA Forms,”[5]Plante Moran International Tax Alert, “Doing Business With Foreign Entities? Say Hello to Form W-8BEN-E,” May 2014. Form W-8BEN-E, was only recently released in final form with instructions by the IRS. The new form is intended to document the US tax status of foreign entities[6]IRS Form W-8BEN is the equivalent form for foreign individuals., including for FATCA purposes, and thus will be a significant piece of compliance documentation for FFIs and other US withholding agents. Foreign entities and individuals will be required to complete new Forms W-8 (whether W-8BEN-E or other versions) over the next cycle as part of the drive for tax compliance. Institutions subscribing to non-US-domiciled funds will see new FATCA-driven disclosures making their way into fund documents. However, not all funds are required to have new account opening procedures in place yet; the FATCA implementation timeline varies based upon the domicile of the offshore fund. Some domiciles have reached agreements (intergovernmental agreements, or IGAs) with the United States or are in the process of completing new agreements. Compliance timelines vary based upon IGA type, which complicates the process of confirming fund compliance for investors.

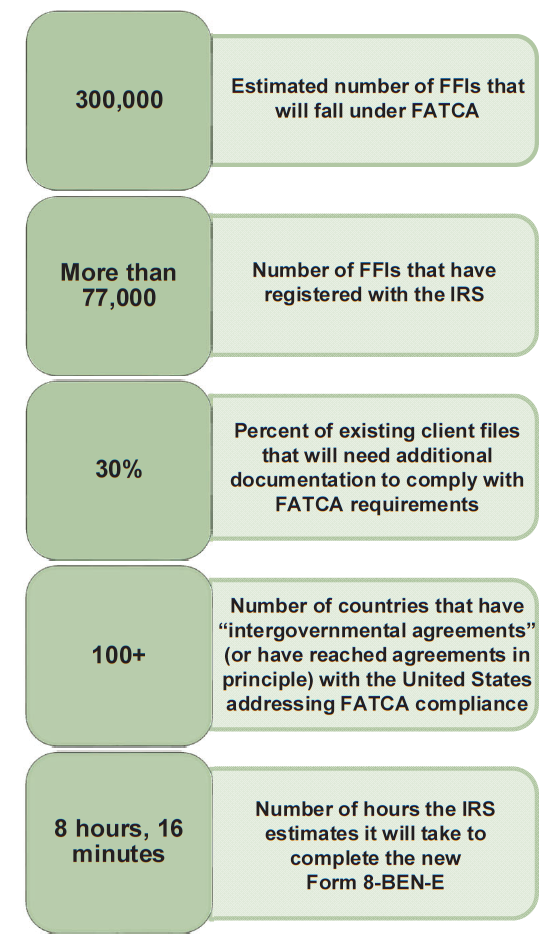

FATCA by the Numbers

Sources: The Economist, FinOps, US Department of the Treasury, US Department of Treasury – Internal Revenue Service.

Note: The number of countries with intergovernmental agreements with the United States is as of June 30, 2014.

Despite all of the delays, FATCA implementation remains a significant challenge and will likely require some action on the part of most investors save perhaps US-based investors exclusively invested in US-domiciled vehicles, an increasingly rare bird today.

— Mary Cove, Managing Director

Footnotes