A number of worries dog municipal bonds today, but for high-bracket taxable investors they remain a solid option

- While tax reform is a concern for muni investors, it would take a radical drop in tax rates to materially reduce munis’ after-tax appeal.

- Pension underfunding is a more serious risk for muni bond investors, who should prepare for pension-related volatility by diversifying across both states and issues and ensuring their managers are actively managing the portfolio.

- With relative appeal intact and absolute valuations at fair value, municipal bonds continue to have a role to play as ballast in taxable investors’ portfolios.

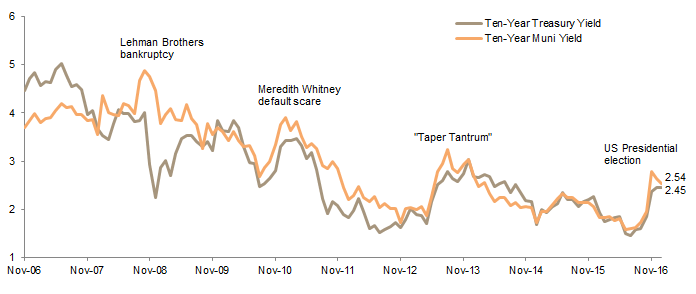

Municipal bonds had a best-of-times/worst-of-times year in 2016, with the Bloomberg Barclays 1-10 Year Index returning about 2.7% during the first half of the year, and the mirror image of that (about -2.7%) during the second half. The full year return was -0.1%. Muni yields roughly tracked the path of Treasury yields during 2016. Ten-year Treasury yields meandered down to just 1.37% in July, before inflation concerns, together with predictions of higher growth and looser fiscal policy, nudged them above 2.5%. The yield of the 1-10 year muni index increased from 1.56% at the end of 2015 to 2.11% at year end. For many municipal indexes, November’s dismal total returns were the worst monthly return in recent decades. The blowout in yields over the past few months was similar in scale to that experienced at the start of the 2008–09 global financial crisis, during the default scare induced in December 2010 by analyst Meredith Whitney, and over the 2013 “Taper Tantrum” (unlike the muni crash surrounding the Lehman Brothers bankruptcy, the latter three instances saw munis suffer along with Treasuries) (Figure 1).

Figure 1. Yields for Ten-Year Municipal Bonds and Treasuries

November 30, 2006 – January 31, 2017 • Percent (%)

Sources: Barclays, Bloomberg L.P., and Thomson Reuters Datastream.

Note: All data are monthly.

Against this backdrop and as 2017 opens, muni investors have voiced a number of worries, including the prospect of tax changes that could make municipal bonds less appealing, the impact of underfunded municipal pensions, and the potential for elevated issuance related to the new administration’s infrastructure priorities. In this note, we share our views on each of these concerns, review muni valuations, and discuss the prospects for future muni returns if the falling rate environment of the past 35 years has indeed come to an end. In short, while investors have some legitimate worries, those in high tax brackets would struggle to come up with a compelling alternative to municipal bonds, which we still see as having a role as ballast in portfolios.

Tax Reform: Only a Modest Concern

Tax reform is a key risk, given that the party controlling the House, Senate, and Presidency plans to cut taxes. Muni bonds are beneficiaries of the tax code, and either sharply lowering tax rates or introducing some taxation of municipal income would limit the relative appeal of municipal bonds. Take, for example, two hypothetical AA-rated bonds that mature in ten years: the municipal bond yields 2.3% and the corporate bond yields 2.8%. With income tax rates above 30%, as they are today, the corporate bond’s after-tax yield (2.0%) is below that of the muni bond. It would take a dramatic cut in the top income tax rate to 18% from nearly 40% today to make the after-tax yields of the two bonds identical.[1]We use corporate bonds in this example because yields of corporate bonds are generally higher than munis today given similar maturities. However, we believe that for most taxable investors, municipal … Continue reading Given that various plans floated in recent months proposed top individual tax brackets between 25% and 33%, we believe that the impact of individual income tax rate cuts (if they occur) will be moderate rather than catastrophic.

Similarly, a lower rate for corporate income taxes, which currently top out at 35%, could crimp insurers’ demand for munis (for the past three decades, insurance companies have held a low-teens percentage of the muni market, and they can serve as important opportunistic buyers during periods of mutual fund outflows).

Some tax reform appears to be priced in. In late November, Morgan Stanley calculated that across the ratings and maturity spectra, muni bonds were trading at an implied tax rate of 22%, from the 40% range earlier last year.[2]Please see Michael Zezas, Mark Schmidt, and Spencer Chang, “Follow the Fiscal Road,” Morgan Stanley Global Insight, November 27, 2016. While anything could happen, a cut in the top individual rate to this level seems unlikely given the proposals already put forward.

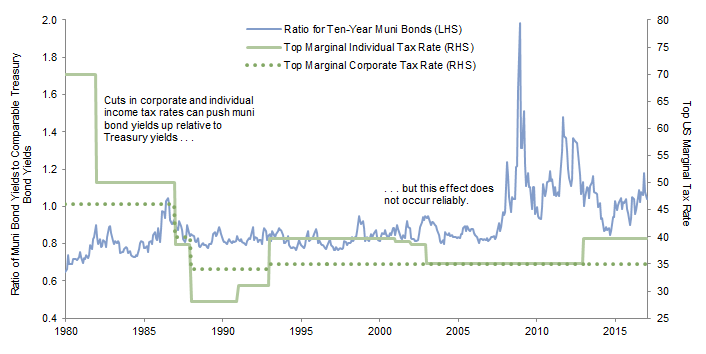

Further, the linkages between tax rates and relative muni yields are not always consistent. In Figure 2, we compare muni/Treasury yield ratios to the prevailing top corporate and individual income tax rates. Munis appear to have suffered (relative to Treasuries) from the Reagan tax cuts in the 1980s. And the rise in the top individual brackets under Bill Clinton made municipal bonds more appealing, helping to suppress yields relative to Treasuries.[3]The level of rates for middle-income households is not a meaningful driver for municipal bonds, which are overwhelmingly owned by high-income taxpayers: two-thirds of the tax-exempt municipal … Continue reading But it is clear from the chart that tax rates are only one of many factors driving relative yields.

Figure 2. Ten-Year Yield Ratios for Municipal Bonds in Various Income Tax Regimes

January 31, 1980 – January 31, 2017 • Percent (%)

Sources: Barclays, Bloomberg L.P., Tax Foundation and Tax Policy Center.

A cut in tax rates is not the only type of tax reform that could negatively impact muni bonds. Other possibilities? The tax benefits of munis could be phased out or capped; for example, legislation could mandate that only the first $1,000 of municipal income is tax-free. And it is even possible that the tax exemption for muni bonds could be scrapped, although while the potential pain of municipal bond holders would elicit little public sympathy, bond issuers facing materially higher funding costs would lean heavily on legislators.

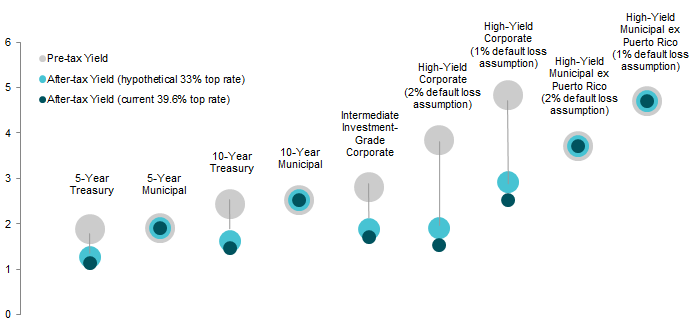

Are there tax reforms on the table that will make muni bonds at least somewhat less valuable? Yes. But some (or even all) of the damage to bond prices is already baked in, and tax cuts sufficient to wipe out the advantage are unlikely. In Figure 3, we compare the yields of muni bonds, corporate bonds, and Treasury bonds on a pre-tax basis, after the nearly 40% tax faced by today’s high income investors, and after a 33% top tax rate, which represents the current proposal from President Trump and the level proposed in 2016 by House Republicans. As shown, municipal bonds have a considerable after-tax return advantage today, and a drop in the top individual tax rate to 33%, while lessening that advantage, does not remove it.

Figure 3. Estimated Pre-Tax and After-Tax Yield of Selected US Bond Investments

As of January 31, 2017 • Percent (%)

Sources: Barclays, Bloomberg L.P., Federal Reserve, and Thomson Reuters Datastream.

Note: Yields on high yield-bonds are reduced to reflect various default-loss provisions.

Pension Underfunding: Pay Attention

For more discussion of these issues see Sean McLaughlin et al., “Eyes Wide Open for Municipal Bondholders as Pension Deficits Widen,” Cambridge Associates Research Brief, December 5, 2016.

Investors are starting to focus on the serious problem of pension underfunding. Moody’s has estimated that unfunded municipal pension liabilities will reach $1.75 trillion this year, even outstripping the total par value of outstanding municipal bonds.[4]This estimate uses long-term corporate bond yields as the discount rate, rather than (overly rosy) assumed returns of 7.5% or more that are commonly used by municipal issuers. The problem is not universal; the majority of pensions are at reasonably healthy levels. But some states and cities are woefully underfunded. Figure 4 shows the percentage of tax revenues required to cover unfunded pension and health care liabilities together with bond interest. Under current assumptions (green bars), the burden is manageable for the vast majority of states. But if the return and amortization assumptions are made more realistic, the burden becomes much less bearable for some states, including Illinois and New Jersey. If states were to discount liabilities at just 5%, with only 20 years of amortization to get back above water, seven states would need to devote an unsustainable 25% of revenues or more to this effort, and these states collectively represent a quarter of the municipal bond market.

Figure 4. Percent of State Revenues Required to Cover Both Bond Interest and Unfunded Liabilities

Fiscal Year 2015 • Percent (%)

Source: J.P. Morgan Asset Management.

Note: Graph also includes revenues required to cover defined contribution plan payments.

Investors are rightly concerned that impossible-to-fulfill pension commitments could impact the credit ratings of general obligation bonds, and they are beginning to discriminate between states with healthy pensions and those like Illinois that have troubling gaps. Investors should employ active managers that can steer away from uncompensated pension risks, and should diversify across states, even though doing so may forgo a slight amount of after-tax yield for investors in high-tax jurisdictions.

Other credit concerns today are even less widespread than pension underfunding, but skilled managers continue to watch them. Some cities, including Hartford, Dallas, and of course Chicago, have varied but difficult financial problems. Additionally, hospitals, which make up about 8.5% of the Barclays Municipal Bond Index, may face revenue shortfalls depending on what happens to the Affordable Care Act.

Elevated Issuance: Not in the Cards

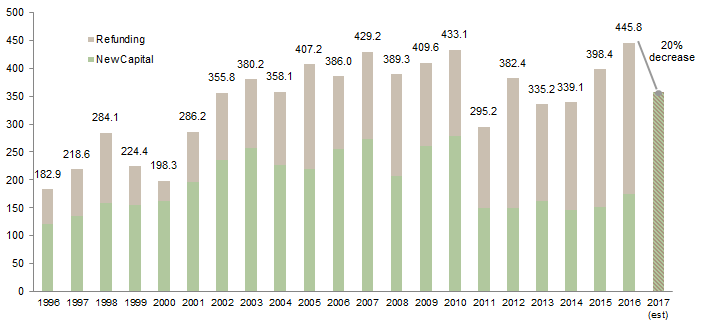

President Donald Trump has pledged to improve US infrastructure. Some investors worry that states and counties, in funding part of the buildout, would issue large amounts of municipal bonds, overwhelming investor demand and pushing up yields. While major infrastructure legislation has yet to be introduced, investors should bear in mind that the recent increase in yields will limit refinancing activity, likely pushing total issuance down, rather than up. Last year, refunding issuance accounted for the majority of new bond issues. While maturing debt will in many cases be replaced, refinancing activity is likely to be materially lower. Based on the total 2017 issuance forecasts from a variety of sell-side firms, issuance will decline an average 20% this year (Figure 5). We do not believe that a surge in issuance this year is at all likely.

Figure 5. Municipal Bond New Capital and Refunding Issuance

1996–2017 • US Dollar (billions)

Source: Securities Industry and Financial Markets Association.

Notes: All issuance data are based on deals with maturity of 13 months or greater. Issuance estimate for 2017 represents the average of issuance forecasts from Barclays, Morgan Stanley, PNC, and RBC (forecasts ranged from $333 billion to $370 billion).

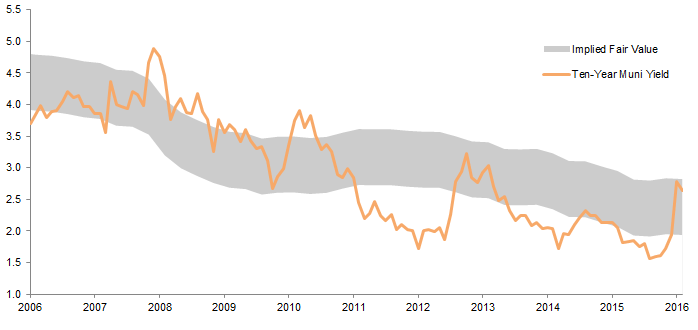

Beyond Appealing Relative Value, Absolute Valuation Is Reasonable

As already discussed, munis are attractive on a relative basis to Treasuries and corporate bonds given their tax advantages. Absolute valuations are also within reason. In our valuation of Treasury bonds, we look at the trailing ten-year average of nominal GDP growth to develop our fair value range. (In high growth environments, bond yields tend to drift upward to compete with investments that will do well in those high growth economies.) For muni bonds, we discount the Treasury fair value by 20% to account for muni bonds’ tax advantages (historically, the ratio of muni bonds to Treasury bonds has varied, but has averaged in the 80% range). By this metric, munis are solidly in fair value (Figure 6), with the current yield of 2.5% for the ten-year muni bond within the 1.9% to 2.8% fair value range. In recent years, municipal yields have traded at a higher average ratio to Treasuries than they did in prior decades, so if this change represents a structural shift, then the range of fair values could be modestly higher. For example, if we assume no yield discount to Treasuries is appropriate, then fair value yields would instead be found between 2.3% and 3.6%. In that scenario, at current yields, munis would still be considered fairly valued.

Figure 6. Municipal Bond Valuations

November 30, 2006 – January 31, 2017 • Percent (%)

Sources: Barclays, Bloomberg L.P., and Thomson Reuters Datastream.

Note: Implied fair value is based on Bloomberg Barclays Municipal Bond Index yield history relative to the tax-adjusted rolling ten-year average US GDP growth.

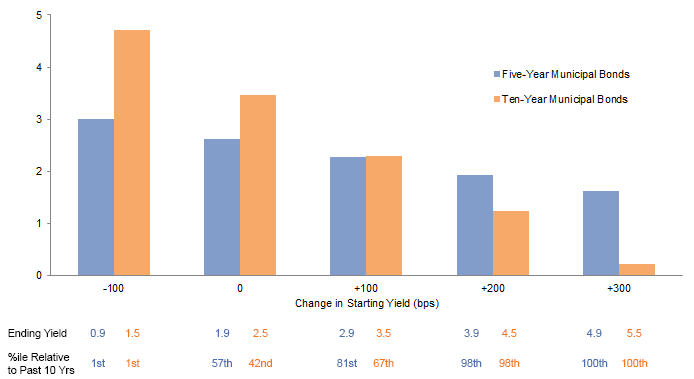

The Future of Returns

When evaluating high-quality bonds (for which there is typically not a material impact from default losses), the starting yield is a solid estimate of subsequent long-term returns. In a falling-rate environment, like we have had for the past 35 years, muni returns have modestly outrun their starting yields in most periods. In a bond bear market, the reverse would generally be true. But the return differences stemming from the level of ending yields are not as large as many investors might believe. Figure 7 illustrates our total return estimates for ten-year municipal bonds over the next five years under five varied ending-yield assumptions that range from 1.5% (the lowest yield on record) to 5.5% (the highest yield over the past ten years). If yields are unchanged and end at 2.5%, annualized total returns would likely come in around 3.5%. Even if yields rise 200 basis points to 4.5% (higher than they were during 98% of days over the past ten years), annualized total returns would still be positive at 1.2%. And for many muni investors, ten years represents the longest maturity in their portfolios, rather than the average maturity. The five-year return estimates for five-year muni bonds would be much closer to their starting yields, as shown in Figure 7, and five-year muni bonds today yield 1.9%.

Figure 7. Five-Year Annualized Nominal Return Estimate for Municipal Bonds at Various Ending Yields

As of January 31, 2017 • Percent (%)

Sources: Barclays, Bloomberg L.P., and Cambridge Associates, LLC.

Notes: Estimates for 5-year municipal bond are based on starting yield of 1.91% and an annual roll yield assumption of 70 basis points. Estimates for 10-year municipal bond are based on starting yield of 2.54% and an annual roll yield assumption of 90 bps. Shifts in yield are based on a starting yield that subsequently approaches terminal yield on a linear basis over a period of five years. Estimated total returns in the stable-yield scenario exceed the starting yield because of the roll-down effect: when the yield curve is positively sloped, yields decrease and prices increase as a bond’s maturity nears, and this boosts returns even when the portfolio is managed to a constant maturity. The scenarios do not include an allowance for default losses; since the 1930s, well-diversified portfolios of high quality municipal bonds have rarely experienced material default losses.

Conclusion

Taxable investors tend to gravitate toward municipal bonds for the ballast in their portfolios. Muni bonds generally exhibit low volatility, and after-tax returns are often unexciting but higher than those on offer from Treasury or investment-grade corporate bonds.

Of the two key concerns we discussed (tax reforms and pensions), pension deficits may prove to be more meaningful than tax reforms over the next five years and are perhaps less priced in. However, we do not believe the eventual pension crunch makes municipal bonds uninvestable today. Investors should be prepared for pension-related volatility, should diversify across states and issuers, and should ensure that their managers are actively managing the portfolio to limit uncompensated exposure to municipalities that have sustainably high unfunded pension liabilities.

Valuations today are reasonable in absolute terms, and particularly in relation to Treasury bonds. Only a few asset classes equal municipal bonds in terms of stability, and for high-bracket investors, these asset classes generally cannot compete with the after-tax expected returns of muni bonds.

Sean McLaughlin, Managing Director

Brandon Smith, Investment Associate

Footnotes