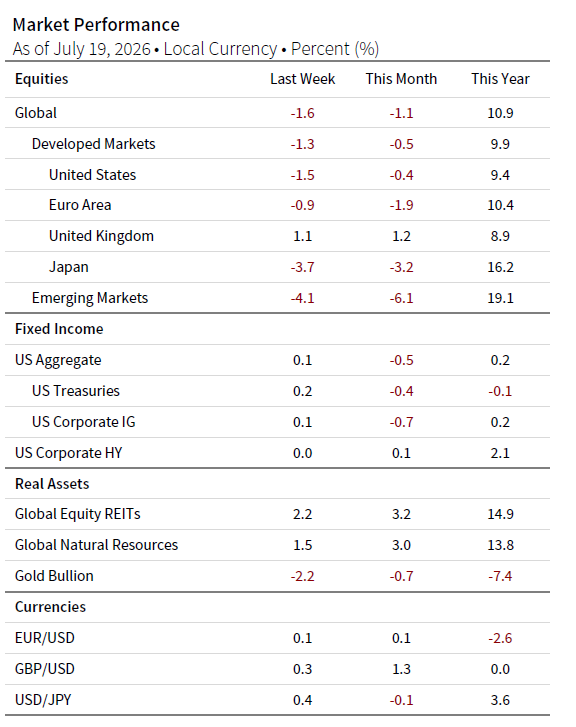

Global equities fell last week, with Korea and Taiwan leading the decline as investors backed away from crowded AI momentum trades. Oil surged roughly 12% on escalating US-Iran tensions, and while Q2 earnings opened on a solid note and US inflation surprised to the downside, neither was enough to overcome broader risk aversion.

- The market’s former leaders became its biggest drag. Semiconductor and memory shares led the decline, with the Philadelphia Semiconductor Index falling more than 20% from its June 22 peak, though still up more than 60% YTD. Samsung Electronics and SK Hynix weighed heavily on Korea, while other AI-linked hardware names also came under pressure across Asia.

- Oil’s rebound complicated the rotation under way. Higher crude prices hurt energy-importing markets and narrowed some of the support for non-US equities, even as investors continued rotating beyond the most crowded AI trades.

- Not all of the AI trade weakened at once. As hardware sold off, selective enterprise software names held up better. Cyclical and defensive sectors also outperformed. Energy stocks rose with crude, and strong investment banking and trading results helped support US financials at the start of earnings season.

- Inflation offered a measure of relief, but not enough to change the mood. June US CPI recorded its largest monthly decline in more than six years, while core inflation eased to 2.6% YOY from 2.9% in May.

Sources: Bloomberg Index Services Limited, MSCI Inc., and Thomson Reuters Datastream. MSCI data provided “as is” without any express or implied warranties.

Notes: This edition was prepared on July 19, 2026, and it reviews developments of the prior month. The equity data are total returns net of dividend taxes of MSCI indexes in local currency. Global natural resources equities are represented by the MSCI All Country World Commodity Producers Index. The fixed income data are total returns for Bloomberg indexes. Gold Bullion uses near-month gold futures contracts, as traded on the COMEX, to determine performance. Currency performance is based on Reuters data.