We are on record advising clients to underweight US equities, as they are overvalued both in absolute terms and particularly relative to non-US markets. That said, we believe strongly in the value of constantly looking for where we could be wrong; thus, we have lately been exploring analyses that make the case for a bullish stance on US markets. What must one believe to be bullish? In our opinion these beliefs range from the plausible (if unlikely) to the downright untenable. Of course, timing, as they say, is everything. At current prices equities are likely to post disappointing returns over the longer term; such considerations tend to be far less important over shorter time frames.

A “New Era”?

Perhaps the strongest bullish case for US equities is, somewhat paradoxically, not really a bullish case at all, but rather an argument that current pricing reflects a long-term shift to lower returns on capital thanks to its easy availability coupled with technological prowess. As long-time pension advisor Keith Ambachtsheer described it in a recent missive: “Pricing [of the S&P 500] is consistent with a lower return-on-capital, lower growth, lower long-term interest rate environment.”[1]Keith Ambachtsheer, “Rethinking Investment Beliefs for the 21st Century,” The Ambachtsheer Letter, March 2015.

Ambachtsheer draws heavily on William Bernstein’s 2013 paper, “The Paradox of Wealth,” which argues that returns on capital necessarily drop as capital becomes more plentiful and economic growth provides more comfortable living standards. In essence, the argument is that worries about current valuations miss the point; rather than representing speculative activity and setting us up for another crash, pricing is instead reflecting the new era of (in Ambachtsheer’s words) “mature capitalism.”

This is at the very least a provocative thesis. However, it is unlikely to mollify investors that want (or in many cases need) higher returns. Ambachtsheer attempts to boost the bullish potential of the argument by saying returns could be better than expected if companies can grow earnings and interest rates stay low, but as we will discuss, the former is in doubt … and we are skeptical the latter will be much help.

About Those Valuations

Most bullish arguments do not say equities are cheap, but rather make the case that current valuations, while high relative to history, are nonetheless justifiable. And there are plausible scenarios under which equities could, in fact, post decent returns from this starting point.

For example, one of our models is for a “boom” scenario under which we assume real earnings growth of 4% and a price-earnings (P/E) ratio at the end of ten years of 21.7 (1 standard deviation above the long-term mean), which gets US equities to an annualized nominal return of 9.3%, and a more than respectable 5.1% real, assuming 4% inflation over the period.

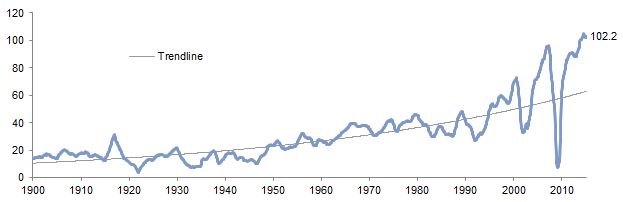

How likely is this? We cover the drivers of corporate profit margins in the next section, but looked at from a top-down perspective, profits are already well above their long-term trend line; it would be unprecedented for growth to continue in such a strong fashion for this length of time. Indeed, given the stresses already apparent—e.g., the gap between CEO and worker pay, as well as worries over debt-funded corporate share buybacks—it beggars belief that corporate profits could post a decade of such torrid growth absent some extraordinary change that also allowed for a sharp rise in wages.

Real Earnings

January 31, 1900 – April 30, 2015

Sources: Global Financial Data, Inc., Standard & Poor’s, and US Department of Labor – Bureau of Labor Statistics.

Notes: Real earnings are shown in logarithmic scale. Real price levels are calculated based on March 31, 2015, dollars. Graph is based on monthly data; monthly earnings are interpolated from quarterly data. Prior to 1968, earnings are reported quarterly by Global Financial Data, Inc. Since January 31, 1968, data are reported by Standard & Poor’s.

Further, it is worth appreciating just how extreme valuations currently are. While an increasing number of observers seek to justify them by pointing out they remain below 1999–2000 peaks, this seems an awfully high bar. We also question the embedded assumption of Ambachtsheer and Bernstein that investors are implicitly “accepting” such returns. The history of valuation extremes is that they always bring out sophisticated-sounding “new era” pronouncements on why this time is different.[2]The most famous example is perhaps Irving Fisher’s 1929 statement that stocks had reached a “permanently high plateau” less than two weeks before the “Black Tuesday” crash. And of course equities can take a variety of different paths on their way to low long-term returns.

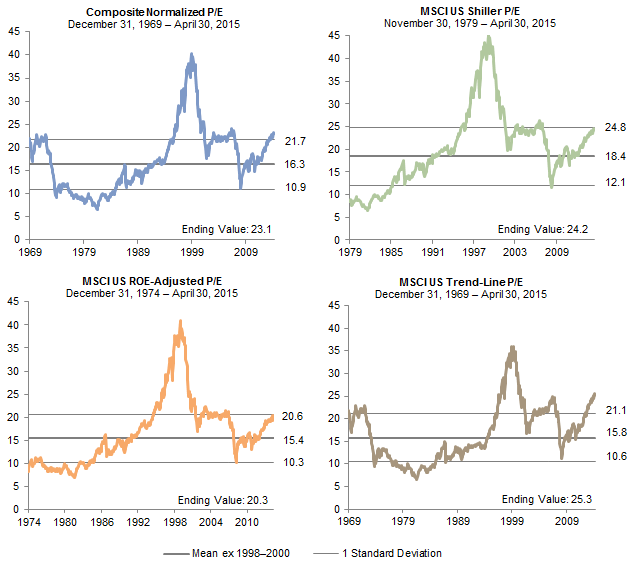

So how high are valuations? Our composite metric for the MSCI US, at 1.3 standard deviations or 41% overvalued, is at levels similar to its 2007– 08 peak and approaching its highest level ever outside the late 1990s tech bubble. This is consistent with other similarly constructed metrics; basically, everything that takes a long-term normalized view of earnings is showing a similar trend.

US Price-Earnings Valuations

Sources: MSCI Inc. and Thomson Reuters Datastream. MSCI data provided “as is” without any express or implied warranties.

Notes: The composite normalized price-earnings (P/E) is calculated by dividing the inflation-adjusted index price by the simple average of three normalized earnings metrics: ten-year average real earnings (i.e., Shiller earnings), trend-line earnings, and return on equity (ROE)–adjusted earnings. To minimize the impact of bubble periods on valuations, we have excluded the years 1998–2000 from our historical average and standard deviation calculations. Graphs based on monthly data. CPI data are as of March 31, 2015.

Even shorter-term metrics such as the trailing 12-month and forward earnings[3]Forward earnings P/E ratios are based on analyst estimates for corporate earnings over the next year. It is worth noting than at least one investment bank has been circulating a chart showing that … Continue reading P/E ratios have risen of late, with the former topping 20 (against a long-term mean of about 16) and the latter above 17, its highest since 2004. With over 70% of companies reporting and using estimated earnings for the remainder, first quarter 2015 earnings are negative on a year-over-year basis. If this holds, it will be the first such decline since third quarter 2012, according to FactSet.

As a result, long-term projections based on reversion to the mean, such as our “return to normal” (RTN) assumptions that reflect our base case, show a low or even negative expected return for US equities over the next decade or so. Our model shows a 0.5% annualized real return for the next decade, while asset manager GMO projects -2.0% for large caps and -3.2% for small caps (over seven years), and Research Affiliates expects 0.7% for large caps and -0.2% for small caps (over ten years).

Valuation-Based Scenario Return Assumptions for US Equities

As of April 30, 2015

Source: Cambridge Associates LLC.

Of course, this assumes valuations return to normal from today’s starting point over the next ten years, but as noted earlier, high valuations are not particularly useful as a timing tool. For context, consider that US equities spent 71 months above 1 standard deviation from 1996 to 2002, and over 40 months from 2003 to 2007 hovering right around that level. Today, equity valuations have been above 1 standard deviation for just 12 months, although as discussed in the next section, valuations would be significantly higher were it not for abnormally high corporate profit margins.

What About Corporate Profit Margins?

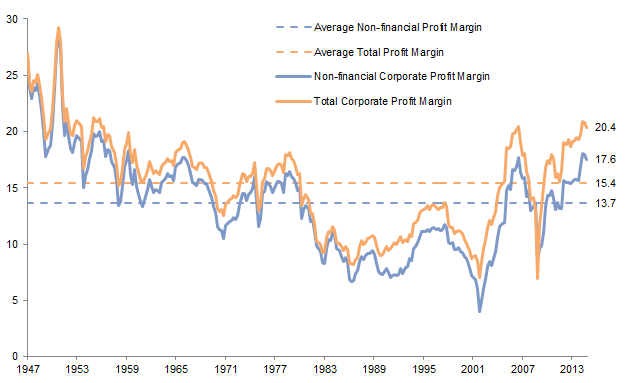

Another bullish argument is that the soaring margins that have enabled booming profits over the last few years are here to stay, and thus worries that they will at some point revert to their long-term mean—crimping profit growth absent a huge increase in sales—are off the mark.

Corporate Profit Margins

First Quarter 1947 – Fourth Quarter 2014 • Percent (%)

Source: Bureau of Economic Analysis.

Notes: Corporate profit margins are calculated by dividing corporate profits before tax by the gross value added of corporate business. All data are seasonally adjusted at annual rates.

To assess the prospects for this, consider what has boosted margins in recent years:

- Easy money. The Federal Reserve’s zero interest rate policy (ZIRP) has allowed virtually any company to borrow money at low rates, thus driving down interest costs and also boosting upside returns through added leverage.

- Lower tax rates.

- A falling share of revenue going to labor versus corporate profits.

- An increase in the weighting of finance and technology firms in the S&P 500, as well as a sharp rise in these sectors’ margins.

Let’s take them one at a time. Easy money certainly seems likely to persist for the foreseeable future, particularly when considering the Sturm und Drang that has accompanied the possibility the Fed might raise rates by an entire 25 basis points later this year.

So long as the money is not repatriated. For more details please see Alex Jones, “The Cash Is Not What it Seems,” Cambridge Associates US Market Commentary, February 2013, and Alex Jones, “Combing Through the Cash Pile,” Cambridge Associates Research Brief, July 24, 2014.

Lower tax rates are a more complicated issue. Much of this is attributable to an increase in overseas sales, which are taxed more lightly than domestic revenues. However, foreign revenues have not only been hurt by the recent rise of the US dollar, but also can result in money being “stuck” overseas lest it be subjected to US taxes. Sustainability seems questionable.

While much ink has been spilled on #3—largely lamenting the declining power of labor—reported numbers may be misleading, in part because of #2. When US corporations boost overseas sales, the profits are included in US GNP … but the labor (assuming it occurs outside the United States) is not. In other words, at least part of the reason this ratio looks as bad as it does is because it counts overseas profits but not overseas workers. As to whether this driver can persist, we are skeptical given both the strength of the US dollar and increased pressure on US corporations to boost wages.

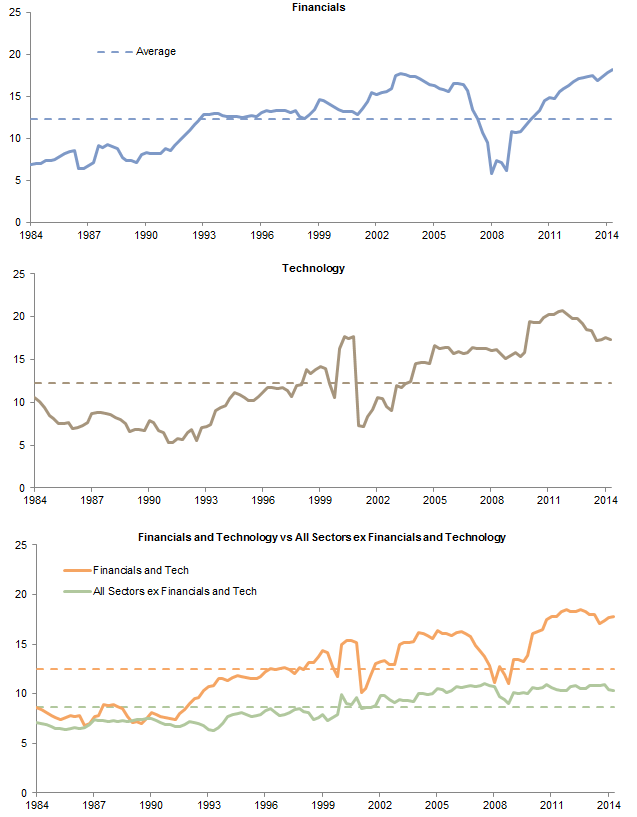

The last driver may be the most important. The margins of finance and tech firms, which currently account for slightly less than one-fifth of US corporate revenues, have soared in recent years; as a result, these two sectors account for just less than 40% of current US corporate profits. Unfortunately, while we can make some informed guesses as to what is going on here—financial firms, for example, have benefited from ZIRP, while the low fixed costs of tech coupled with a “winner take all” model have engendered huge margins at firms such as Apple, Facebook, and Google—it is a fool’s errand to predict the staying power of such trends.

Those making a more bullish argument would rejoin that financial firms are likely to continue benefiting from the easy money environment for some time, and that the economics of the tech industry have gone through a structural change that will enable “winners” to charge premium fees due to network effects (e.g., advertisers feel they must be on Google because of their dominance of search, while Apple users are willing to pay up for the convenience of having everything centralized in the Apple “network”).

It is certainly plausible that US corporate profit margins can remain high; the best hope for this seems to be persistence in the easy money environment, and perhaps a reversal in US$ strength. And while current margins are well above their long-term mean, their history shows a number of long trends above and below the mean; thus, it is hardly inconceivable that high margins will persist longer than we expect. But similar to the “boom” scenario, this is not our base expectation.

Profit Margin of Russell 3000® Index Sectors

Fourth Quarter 1984 – First Quarter 2015 • Percent (%)

Sources: FactSet Research Systems and Frank Russell Company.

Beyond Fundamentals

Finally, we can’t have a discussion about bullish arguments without mentioning the elephant in the room—the continued, and increasing, intervention of central banks in asset markets. Setting aside issues about the ultimate effects (not to mention ethics) of policies such as ZIRP and direct asset buying, there is little question investor faith in the “Yellen put”[4]Formerly known as the Bernanke put, and which of course originated in the late 1990s as the Greenspan put. has underpinned US equities in recent years—and even less doubt direct measures such as those undertaken by the Bank of Japan (among others) to buy index exchange-traded funds, particularly on days the market is down,[5]As detailed by Takashi Nakamichi and Tatsuo Ito, “BOJ Helps Tokyo Stocks to Soar,” The Wall Street Journal, March 11, 2015. have boosted equity prices. Thus, one can make a plausible case that no matter what happens with fundamentals, central banks, which no longer view equity prices as a reflection of underlying economic reality, but rather a tool to help shape it,[6]As spelled out in then–Fed Chairman Ben Bernanke’s November 4, 2010, Washington Post op-ed: “What the Fed Did and Why: Supporting the Recovery and Sustaining Price Stability.” will continue doing “whatever it takes” to keep equity prices levitated.

What About Structure?

Equity prices are high relative to earnings, which are themselves elevated thanks to historically high profit margins. Yet one can construct a bullish case for US equities. The question is, to what degree are the assumptions baked into such a view plausible … or even possible? Our view is that the beliefs needed to assume a strong return for US equities over the next decade or so are unlikely to come to pass, but certainly not impossible. That said, given the dearth of attractive alternatives and the challenges of generating a return that will cover spending needs in the current environment, investors should maintain some of their allocation to US equities, which is why we have advised only small underweights to this asset class in favor of overweights to Europe, Japan, and emerging markets, particularly in Asia.

Within US equities, investors should take a close look at how their exposures are structured. While active management (particularly of the value bent) and hedge funds have taken a beating of late, both in terms of returns and public perception, this is to be expected in the late stages of a bull run such as we have seen over the past several years. We remember hearing similar death knells for such managers in 1999 and 2007, right before many of them more than earned their keep.

Jon Hansen et al., “Hedge Funds: Value Proposition, Fees, and Future,” Cambridge Associates Research Report, August 2013.

As we said a couple of years ago: “To a certain degree, the concept of alpha has been lost in a recent market environment composed of higher correlations across assets and narrower return dispersion across managers.” When this environment ends, investors will almost certainly benefit from active managers and hedge funds with the courage to take non-consensus positions.

See our recent publication, Eric Winig et al., “Time to Batten Down the Hatches?,” Cambridge Associates Research Brief, March 16, 2015.

In short, while we still don’t know whether it is time to batten down the hatches, investors would be well served to make sure their US equity structure is consistent with their risk tolerance.

The Bottom Line

To believe long-term returns on US equities from this starting point will approach historical averages, one must essentially believe most, if not all, of the following:

- US corporations—particularly tech and finance firms—will continue to earn profits at historically extreme rates for the foreseeable future.

- Interest rates will stay at historically low levels.

- Credit markets will remain extraordinarily accommodative.

- Real economic growth will surprise to the upside.

- Valuations will rise to even higher levels thanks to central bank support.

Of all these we find the last the most compelling … and the most concerning. In our view, investors today are not willingly accepting a period of lower returns on capital, but rather buying equities because they are being forced out the risk curve by central banks intent on keeping risk asset prices levitated. In this challenging environment, investors would do well to take a close look at their US equity structure to ensure it is compatible with their risk tolerance.

Footnotes