Executive Summary

- Manager selection is critical when investing in hedge funds. Every analysis of a potential hedge fund allocation boils down to a granular assessment of a fund’s value proposition as reflected in its investment philosophy, terms, and business operations. Equally important is the need to identify the specific role each fund serves as part of an overall portfolio.

- Successful hedge funds exhibit three basic characteristics: consistent alpha-generative security selection, portfolio management expertise, and business proficiency. Exceptional managers blend proprietary research with portfolio construction in a way that allows them to leverage their best ideas while maintaining sound risk management. Position sizing, entry and exit timing, strategy rotation, and internal prioritization of investment ideas all contribute to performance. Net returns matter most, but the path taken to achieve those returns is important, too. Good hedge fund managers are good business partners, and tend to have long-term relationships with their investors. Investors should look to allocate capital to managers they believe will treat all investors equally and honorably both in good times and through any rough patches.

- Each hedge fund represents a unique line item in a diversified portfolio and should serve a specific role (e.g., growth engine or diversifier). As part of the due diligence process, limited partners (LPs) should understand the attributes each fund offers and consider how much they are willing to pay for those attributes. To achieve the investment goals of individual long-term investment pools, LPs must exercise discipline and be willing to redeem from managers if the value proposition offered is no longer attractive or if a more compelling value proposition exists elsewhere.

- Hedge fund investments carry several basic costs, among them, advisory fees (including management and performance fees), fund expenses, and indirect costs; an effective evaluation looks at the full carrying costs of the investment. Management fees are intended to allow the manager to run the business and should not be a primary source of profit. Today, the trend is clear—fees are under pressure and will continue to be so. Although the base compensation structure of management and incentive fees is likely to remain, the industry continues to evolve. Management fees that scale down as assets grow or over time to reward investor loyalty are likely to become more common.

- Regulatory uncertainty remains the biggest wildcard for hedge fund managers. Additional regulatory requirements have added to the cost of running any hedge fund and for newer firms with smaller asset bases, these increased costs will be even more meaningful. What today is deemed as legal, in-depth research may be viewed in a different light in the future.

Hedge funds add value to diversified portfolios, but not all hedge funds do so; not even close. Of the 9,000 or so entities self-titled as hedge funds, only a small percentage (think low single digits) offer compelling value propositions for institutional investors. Given these odds, manager selection is critical when investing in hedge funds (Figure One). Equally important is the need to identify the specific role each fund serves as part of an overall portfolio; no one likes to experience buyer’s remorse.

The last few years have led to increased scrutiny of hedge fund returns, and now more than ever managers must be able to show how their funds contribute to broader portfolios and explain why specific fee and liquidity structures exist. Our clients have had exposure to hedge funds for close to four decades and have benefited from the differentiated return streams, capital protection and reduced volatility offered through these partnerships. We continue to believe hedge funds serve a vital role as part of strategic asset allocations. The industry has evolved over time, but much has remained constant in the way we identify and select managers. Every analysis boils down to a granular assessment of each hedge fund’s value proposition as reflected in its investment philosophy, terms and business operations.

As investors have revisited their hedge fund allocations over the last year or so, some common themes have emerged in discussions with investors and managers. This paper seeks to address several of those themes. In particular, this paper will consider: (1) the characteristics of successful hedge fund partnership; (2) the importance of understanding the expected role each fund serves; (3) fees and terms as part of the hedge fund value proposition; and (4) the future landscape for hedge funds.

Figure 1. Manager Return Dispersion

As of December 31, 2012 • Based on Ten-Year Average Annual Compound Returns

Source: Cambridge Associates LLC Investment Manager Database.

Notes: Percentile rankings are based on a scale of 0–100, where 0 represents the highest value and 100 the lowest. Data are based on managers with a minimum of $50 million in assets. Absolute return includes multi-strategy, event-driven, general arbitrage, and credit opportunities. For absolute return and hedge funds, returns are reported net of fees. For other strategies, we have subtracted a fee proxy from returns reported gross of fees as follows: U.S. core/core plus bonds, 33 basis points (bps); emerging markets equity, 98 bps; U.S. large cap, 69 bps; U.S. small cap, 93 bps; and global ex U.S. equity, 80 bps. Managers for which product asset data were unavailable were excluded. All of the manager universes have survivorship bias, so while the distribution may include better performance, the comparison across strategies is valid.

Foundations for Success

When it comes to manager selection, successful hedge funds exhibit three basic characteristics: consistent alpha-generative security selection, portfolio management expertise, and business proficiency. Regardless of the timing of fund due diligence—twenty years ago, present day or a decade in the future—the presence of each one of these attributes increases the likelihood of realizing consistently attractive risk-adjusted returns.

No matter the strategy, investors expect hedge fund managers to identify compelling investment ideas for their portfolios. From a security selection perspective, however, consistency is the key. One sizable win from a correct market call or one-time market event (e.g., subprime trade) may generate a spectacular windfall and public acclaim but it does not on its own make a compelling case for long-term investment. The repeatability of a manager’s idea sourcing process is critical. For evergreen funds, this process must apply for one or multiple strategies and be driven by a specific research skill, investment philosophy or other competitive idea sourcing edge.

Exceptional managers blend their proprietary research with portfolio construction in a way that allows them to leverage their best ideas while maintaining sound risk management. Blowups may generate headlines, yet for every hedge fund implosion caused by poor judgment there are dozens of other managers that, while never putting their limited partners’ investment lives at risk, fail to do more than generate an uninspiring return. Position sizing, entry and exit point timing, strategy rotation and internal prioritization of investment ideas all contribute to performance—skill in these aspects of portfolio management often separates true moneymakers from merely good storytellers. From a manager evaluation perspective, portfolio construction talent is often the most challenging attribute to identify.

Hedge funds operate in a hyper-competitive environment and by nature are fragile businesses. Even with the institutional changes experienced in the industry during the last decade, it is still surprising to find the high number of managers who fail to step back and apply the same analytical lens they use for prospective investment opportunities to their own businesses. An inability to motivate employees, retain key personnel, share wealth, reinvest in the business, be entrepreneurial and provide sound customer service (including transparency beyond rote reporting of numbers) is often what dooms managers who otherwise have the pedigree for investment success. In the long/short equity space, hedge fund managers generally look for long positions in companies with management teams that seek to maximize shareholder value; limited partners should have the same expectations of the managers themselves.

Ultimately, net returns are what matter, but the path taken to achieve those returns is important, too. The absolute number of top funds may be small as a percentage of the overall universe, but institutional limited partners still have many investable options: an investor should never force an allocation if there is any question regarding the manager’s integrity (regardless of a firm’s performance track record). Good hedge fund managers are good business partners, and tend to have long-term relationships with their investors. Offering documents are important in framing the relationship between the general partner and limited partners, but in most cases the terms are quite permissive, giving a lot of discretion to the investment manager. Investors should look to allocate capital to managers they believe will treat all investors equally and honorably in both good times and through any rough patches.

Role in the Portfolio

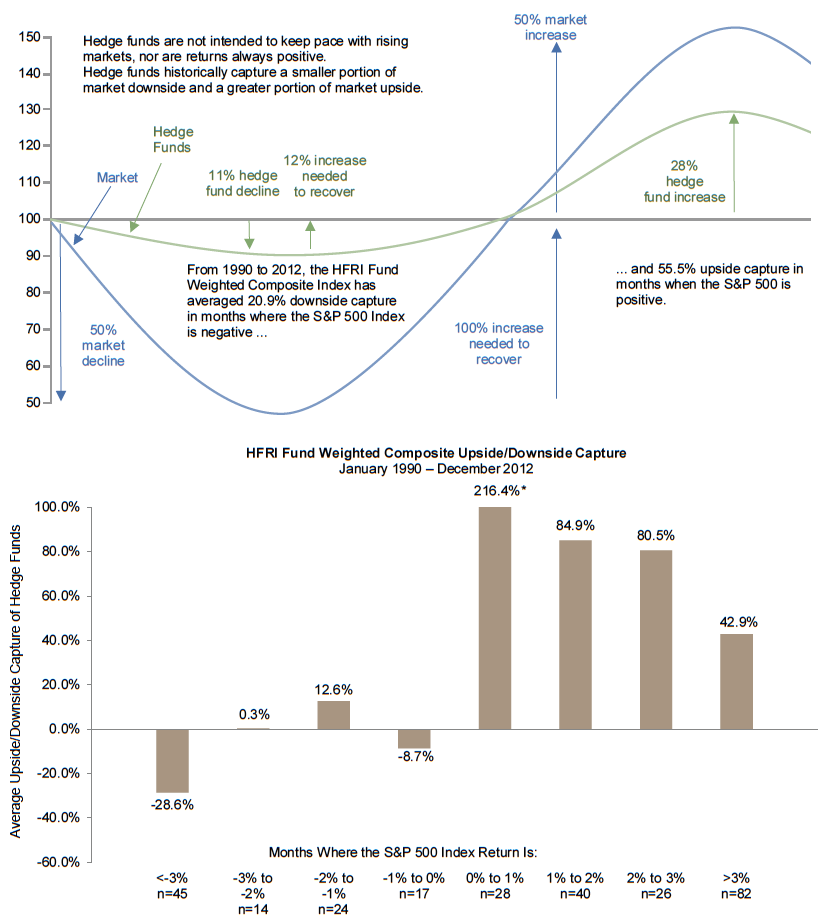

LPs pay higher fees and forgo liquidity to invest in hedge funds. In return, investors expect something special not offered through other investment vehicles. Investors should require more from their hedge fund managers than a mirrored equity market return that could be implemented easily and cheaply through index funds and exchange-traded funds (Figures 2 and 3) . During a bull market investors may naturally yearn for less-hedged exposure, but capital allocators should not underestimate the positive and long-term impact on portfolios from the smoothing effect of differentiated return streams, capital protection, and reduced volatility (factors that have lost their immediacy as 2008 fades from shorter-term performance reviews).

Figure 2. The Positive Impact of Return Smoothing on Compound Returns

Notes: For the ten-year period ended December 31, 2012, the volatility of the HFRI Fund Weighted Composite Index was 6.5, versus14.8 for the S&P 500 Index. Returns in this example are fictitious. Hypothetical performance results have many inherent limitations, some of which are described below. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. In fact, there are frequently sharp differences between hypothetical performance results and the actual results subsequently achieved by any particular investment program. One of the limitations of hypothetical performance results is that they are generally prepared with the benefit of hindsight. In addition, hypothetical trading does not involve financial risk, and no hypothetical trading record can completely account for the impact of financial risk in actual trading. For example, the ability to withstand losses or to adhere to a particular trading program in spite of trading losses are material points that can also adversely affect actual trading results. There are numerous other factors related to the markets in general or to the implementation of any specific trading program that cannot be fully accounted for in the preparation of hypothetical performance results and all of which can adversely affect actual trading results.

Figure 3. Misperceptions About Hedge Fund Behavior: Asymmetric Upside and Downside Capture

Sources: Cambridge Associates LLC Investment Manager Database, Hedge Fund Research, Inc., and Standard & Poor’s

* Graph is capped for scale purposes.

Each hedge fund represents a unique line item in a diversified portfolio and should serve a specific role (e.g., growth engine or diversifier). As part of the due diligence process, limited partners should understand the attributes each fund offers and consider how much they are willing to pay for those attributes. Fund characteristics to consider include: strategy exposure, expected volatility, equity or credit beta, upside/downside capture rate, correlation to markets and other managers. How a particular manager may perform in a specific market environment is also an important consideration. An effective manager evaluation considers potential near-term returns, performance in times of stress, and longer-term opportunities all while keeping in mind the carrying costs for maintaining the investment.

The post-Great Recession investment period has been marked by high correlations across asset classes, pockets of elevated volatility, and an extended low interest rate environment, all of which have affected the opportunity set for hedge funds and for active management in general. Certainly there has been no shortage of lackluster returns during the last few years, and periods of lower returns naturally trigger questions about the sustainability of specific strategies or of the industry at large (i.e., is there any role for hedge funds in a portfolio?) (Figure 4) . That macro conditions can impact investment opportunities over discrete time periods is not new, and investors should be careful not to extrapolate short-term performance into industry demise. A Fortune magazine story titled “Hard Times Come to Hedge Funds” outlined how managers got “clobbered” on their shorts, “murdered” on their longs and had concern as the “SEC is moving in ….” That particular article was published not last year but in 1970. An investor who was convinced forty-plus years ago that all hedge funds were doomed would have missed considerable portfolio benefits over the ensuing decades.

Figure 4. Comparison of Hedge Fund Returns to Equities

December 31, 1994 – June 30, 2013

Sources: BofA Merrill Lynch, Federal Reserve, Hedge Fund Research, Inc., MSCI Inc., and Thomson Reuters Datastream. MSCI data provided “as is” without any express or implied warranties. Notes: Graphs compare rolling five-year hedge fund index performance to the beta-adjusted MSCI World Index return. Beta measures th sensitivity of the portfolio’s rate of return to changes in the market’s rate of return, and therefore measures the amount of risk in the portfolio that cannot be removed through diversification. A beta in between zero and one means that the asset’s returns are similar in direction to the benchmark’s but the magnitude of moves are lower (less volatile). Historically, hedge fund returns have been significantly less volatile than the benchmark MSCI World Index. Beta to the benchmark for the period is 0.37 for the HFRI Fund Weighted Composite Index, 0.46 for the HFRI Equity Hedge (Total) Index, and 0.38 for the HFRI Event-Driven (Total) Index. To better measure the value added provided by hedge funds, we beta adjust the benchmark index returns to reflect the lower volatility of the HFRI indices. The beta-adjusted equity returns are calculated as excess return of the MSCI World Index (Index return minus the 91-day T-bill return) multiplied by the respective HFRI Index beta, plus the 91-day T-bill return.

No textbook or model can provide the exact number of hedge funds or commensurate strategy exposure to maintain in a portfolio. To achieve the investment goals of individual long-term investment pools, limited partners must exercise discipline and be willing to redeem from managers if the value proposition offered is no longer attractive or if a more compelling value proposition exists elsewhere (either through another hedge fund or in an entirely different asset class). Reasons for manager turnover include: organizational changes, shifts in assets under management (increase or decrease), style drift, or prolonged underperformance. Industry-wide asset flows into or out of a strategy may also impact the risk profile for a particular fund and its return prospects. Prudent turnover across a hedge fund roster is necessary and healthy. It is rare (if it has ever been the case) for an investor to comment on how manager proliferation has added value to a portfolio.

Fee Components

Terms and fees vary across hedge funds. In evaluating any active manager, one question stands out: “Am I getting what I’m paying for?” Given their more flexible, less liquid investment structure and higher fees, this question is especially important for hedge funds, and is one that does not disappear after a manager funding. Limited partners should regularly evaluate each hedge fund in their portfolio regardless of any lock-up. A derivative aspect to this question is the issue of who should pay for what and in what amount as it relates to the investment process. Hedge fund investments carry several basic costs: advisory fees (including management and performance fees), fund expenses, and indirect costs. Limited partners may wish to consider each component in isolation, but an effective evaluation looks at the full carrying costs of the investment. A hedge fund that offers a low management fee but then passes through a high percentage of fund expenses may represent no better value proposition than a manager with a higher fixed management fee but much lower discretionary expenses. Managers should be able to explain why they have a certain fee structure in place and how the fees fit within the operations of the business. Be wary of any manager who says he has set his fees at a certain level because that is what the capital introduction team told him he could get or because that is what everyone else does.

Management fees are usually net-asset based fees charged on a quarterly basis. These fees are intended to allow the manager to run the business and should not be a primary source of profit. Incentive fees generally are charged annually and are meant to compensate a manager for generating positive investment results. The structure is intended to create alignment of interest between the general partner and the limited partners. Often the performance fee will be subject to a high-water mark. i.e., if the fund has lost money for a given period, the manager forgoes an incentive fee until the breakeven point is reached again

Some funds implement a modified high-water mark wherein limited partners pay a reduced carry (typically half of the normal incentive fee) until the fund recoups an amount in excess of the drawdown (often 150% to 200% of the drawdown). This structure is intended to provide a manager with organizational stability after a down period.

In addition to the management fee, there are usually other costs and fees borne directly by the fund, however, fund pass-through expense policies differ from firm to firm. Annual audit and tax costs, third-party administration costs, fund-related legal fees (set-up and offering), investment research and offshore fund director fees are examples of typical fund expenses. Other expenses may include investment-related legal costs, research travel, technology costs, marketing costs and employee compensation. Indirect costs include trading commissions and prime brokerage-related costs.

Carrying costs (fees and fund expenses) should be straightforward and structured in a way that treats all limited partners in an equitable manner. Investors should know which costs they absorb, whether there are any fee caps and what total costs represent as a percentage of their investment. Given the potential open-ended nature of some of these charges, it is critical for an investor to believe that the manager is a good business partner. Certain investors may have different terms based on their individual characteristics (e.g., an investor that allocates a large amount of capital to a manager may receive a fee reduction).

Managers should be willing to disclose these differences and again be able to articulate the underlying business reason why such a difference exists. While some term variations are reasonable, limited partners should carefully consider investing in a fund where certain investors have materially better liquidity rights or other benefits.

Friction Points

Fees and liquidity are the two aspects of hedge fund investing that trigger the most unease for investors. The traditional hedge fund compensation model is skewed in favor of the general partner as there is no upside cap on fees, and at least theoretically a hedge fund manager can generate a limitless return as a percentage of each investor’s initial contribution (i.e., the percent incentive fee charged remains constant but the dollar value of the actual carry earned increases as a percentage of the initial investment).

Investors have downside protection through the high-water mark structure, which serves to make the fee distribution more symmetrical by reducing or eliminating certain fees following periods of negative returns, but the structure is still asymmetric since fees are never negative. And in a worst-case scenario, a manager can lose most (or all) of his limited partners’ capital, close the fund down and then reinvent himself elsewhere (an unfortunate outcome that has occurred in the industry).

When managers generate exceptional returns, the hedge fund compensation structure receives less scrutiny. Even though the percentage gap between the gross and net return increases as returns increase, limited partners are (rightfully) pleased when they receive outsized returns. For periods when returns are lower on an absolute basis, fixed fees take up a much greater percentage of overall returns. A limited partner invested in a fund with a typical fee structure may see fees erode close to fifty percent of the return if the fund compounds at a mid-single digits rate. Under these circumstances, it is natural for investors to reexamine the question: “Am I getting what I’m paying for?”, and to do so with a heightened urgency.

Figure 5. Impact of Fees on Hedge Fund Returns: Sample Analysis

Today the trend is clear: fees are under pressure and likely will continue to be so. Anyone who has invested capital over an extended period of time has experienced stretches of underperformance. However, participants in the hedge fund industry recognize that performance expectations are always high. No doubt certain short-term factors have impacted return opportunities. For example, in periods with higher interest rates, the return earned on cash reinvested from short sales (referred to as the “short rebate) often offset the fixed costs a limited partner incurred for holding the investment. In some instances, the cost for executing short trades has increased. But managers do not receive a free pass; if the value proposition of a manager is so thin it is skewed due to the lack of a short rebate, the value proposition may not be that compelling anyway.

The second sensitivity point for limited partners is liquidity. The most typical tradeoff for funds with multiple share classes is a reduced incentive fee (and, at times, management fee) for capital that is locked up for an extended period. As the hedge fund industry has evolved, views and treatment of liquidity have changed. The trend from the 1990s through the financial crisis had been toward offering less liquidity to limited partners. Often managers that expanded their mandates from single to multiple strategies, and thereby took strategy rotation responsibilities away from limited partners, extended fund lockup terms. As hedge funds shifted toward private investments in the mid-2000s, liquidity profiles became even less attractive with more funds pursuing private deals often set aside in illiquid side pockets.

The first attempt to mandate hedge fund registration in 2004 had a likely unintended impact on hedge fund liquidity structures. In seeking to exclude private equity and venture capital funds from the registration process, the SEC defined “private funds” in part as vehicles that permitted investors to redeem within two years of entry. That registration attempt ultimately was deemed unlawful in 2006.[1]Goldstein v. Securities and Exchange Commission, No. 04-1434, 2006 [D.C. Cir. June 23, 2006] Nonetheless, following the SEC release, many hedge funds, particularly new launches, moved to a two-year lock-up as a way to bypass the then-pending registration.

For investors, the most important consideration about liquidity is whether the fund structure and investment approach create an asset/liability mismatch. Certain strategies rely on investment theses that take longer to play out; a limited partner will not profit if the fund’s structure allows ill-conceived liquidity. No one wants their investment results held hostage by others who might create organizational or portfolio instability by losing patience and redeeming at an inopportune time. At the opposite end of the spectrum, investors should be skeptical of managers with portfolios that offer infrequent liquidity when the underlying holdings are liquid.

Liquidity has value and limited partners should be skeptical of managers that artificially claim the need for a long-term lock for more liquid strategies and portfolios without any equitable trade-off on the incentive fee. From an organizational stability perspective, length of lock is no more important than how staggered exit points are across the limited partner capital base. Having a more balanced capital base with varied exit points across the partnership was one of the most positive organizational changes to come from the liquidity issues experienced in 2008, as managers recognized the importance of avoiding a self-imposed run-on-the-bank. In addition, fund terms incorporating mandatory side pocket exposure have largely disappeared. Instead, most hedge funds that still invest in private deals allow limited partners the ability to opt out, a significantly better structure than in times past. If a hedge fund spends considerable investment time pursuing and executing illiquid investments, limited partners need to account for this exposure and activity when assessing the risk profile of the fund.

A More Perfect Union

Perfection is an impossibility in the investment world, as no fund will ever offer the exact combination of investment strategy and terms sought by each limited partner. Investing is a personal process and in assessing each organization’s value proposition, limited partners must prioritize what is most important to them. For some, the length of lock may be prohibitive, for others the composition of the investor base may be unacceptable. Just because a manager sets his management or incentive fee at a certain level does not mean the value proposition is unattractive. In conducting each manager review, investors must balance the philosophical underpinnings of the terms with the operations of the organization and, of course, the expected net return.

In term and fee negotiations with managers, it is clear an anchoring effect exists within the industry. In general, managers perceive change in a negative light; even firms with strong risk-adjusted track records, loyal capital bases and stable organizations have proceeded cautiously when considering term changes. No one wants to give off any scent of weakness and most managers have been quite comfortable with the legacy hedge fund structure.

Although the base compensation structure of management and incentive fees is likely to remain, the industry continues to evolve as investors seek and realize term and fee modifications. In some cases, managers have lowered their base fees; two and twenty is no longer an accepted industry norm. Other adjustments include management fees that scale down as assets grow or scale down over time to reward investor loyalty; these features likely will become more common. A more creative approach may see managers implementing a hard dollar cap on management fees and thus rebating any excess fees at year end. Current best practice calls for managers to calculate the incentive fee net of all other expenses. Managers may go a step further and calculate incentive compensation off a base that represents a return net of two or three times all expenses. Not yet in use in the industry, this structure would provide an ongoing hurdle not market-related and also maintain alignment of interest by serving as an incentive to keep costs low. The periods over which firms crystalize the incentive fee may also lengthen (i.e., from an annual calculation to over a two- or three-year period to match lockups), although such a structure may have a derivative impact on organizational stability and trigger potential tax-related complications.

Business owners must leverage their resources, including revenue streams, to maintain their value proposition or strengthen it. Effective reinvestment in the business is important; examples include firms that have enhanced their investment teams to take advantage of market opportunities such as the recent hiring of individuals with structured product expertise or built out their own custom technology and tools to improve the research process. What does not constitute effective reinvestment is seeing insider capital grow as a larger percentage of the asset base as excess management fees paid to the general partner are recycled into the fund, particularly after periods of lower returns. In addition, it is fair for limited partners to question whether firms that generate significant revenue from the management fee also need a modified high-water mark structure to maintain organizational stability.

Future Landscape

The barriers to entry for the hedge fund industry have increased during a time when traditional funding sources have become less available. Breakeven points vary from organization to organization, but what is clear is that additional regulatory requirements have added to the cost of running any hedge fund. While limited partners will continue to seek more efficiency from funds, managers will be experiencing higher operating costs and looking for ways to offset those expenses.

For newer firms with smaller asset bases, these increased costs will be even more meaningful, adding to already existing pressure for new entrants to perform well upon launch; any cushion managers previously had to weather rough early patches no longer exists. The danger is that new participants will be so disadvantaged relative to larger, more-established industry peers that the landscape will become bar-belled with a few large legacy firms and a larger number of satellite firms never able to grow to an optimal size. Over the long term, it is important for limited partners to see compelling new market participants, as competition is healthy and hedge funds have lifecycles. While the industry is seeing more successful generational transfers as it matures, there will still be many cases when a portfolio manager’s retirement represents the end of a firm.

Seeding relationships for new launches will continue to increase. These structures can impact value propositions so limited partners will need to take into account the ownership structure of each fund. To the degree possible, given the confidential nature of many transactions, investors should have a clear understanding of both current and long-term ownership arrangements. As hedge funds mature, the industry will also see more deals involving owners seeking to monetize the general partnership. Whether a firm executes a passive transaction, public offering or other deal type, each manager will provide a reason why the transaction is beneficial to limited partners (some with more spin than others). In assessing these transactions, limited partners should keep in mind that hedge fund managers act in a manner consistent with their personal best interests (if they acted otherwise you would question their business acumen). It is a red flag when the purchasing entity in a transaction looks for significant asset growth, has influence over the firm’s direction or shifts the investment team’s focus away from returns and more toward annuity management (i.e., the most important aspect of the organization becomes steady income from the management fee).

Lifecycle changes at funds and within the industry can lead to changes in investment approach. For example, as different investor types including pensions and sovereign wealth funds have embraced alternatives, the composition of the hedge fund investor base has shifted. Investors able to allocate large blocks of capital may impact not only fees but also portfolio construction. Limited partners should be alert to the possibility that when a manager accepts a large capital allocation from one entity he or she may change the investment approach of the organization to be a better fit for that particular sizable investor. A shift in mandate can also occur absent a change in investor composition. For example, the risk appetite of a manager who has a majority of his wealth invested in his fund may evolve as that individual matures. As more managers run funds for longer periods, industry participants may question the traditional notion that alignment of interest must call for a manager to have most of his liquid net worth invested in his fund.

Investors pay hedge fund fees to access investment strategies not available elsewhere. If investors are able to identify alternative investment options that offer the same attributes as traditional hedge funds but with lower costs and more liquidity, the industry’s supply/demand dynamics will change. There are now many more ways for limited partners to gain short exposure than what existed a decade or two ago, but most of these products encompass a high degree of market timing and have little alpha from other sources. Due diligence on these alternative investments requires the same value proposition analysis as for traditional hedge fund investments; lower fees and greater liquidity do not automatically equate to a better long-term investment option.

The biggest wildcard for managers remains one that has existed for a number of years: regulatory uncertainty. The greatest risk to the hedge fund structure is a scenario in which certain strategies become too expensive to execute or in which legislation renders the business model unsustainable. Courts may view what is today deemed as legal, in-depth research in a different light in the future. Government enthusiasm for short bans and similar initiatives has waned in the quarters and years since the financial crisis but sentiment can change quickly depending on the current market environment or political shifts. Today, such outcomes may look like extreme tail-risk events, but as the last decade has demonstrated, anything is possible.

Conclusion

As with all industries, the landscape for hedge fund managers continues to change. Asset flows into and out of strategies and individual managers fluctuate as risk/reward propositions change, and limited partners will continue to task managers with being entrepreneurial and opportunistic while not straying from the processes and approaches that have made them successful.

Manager selection remains critical. Our longest-standing and best hedge fund relationships are with managers that care not only about their risk-adjusted track records but also about their reputations. These managers couple a desire to be right with a willingness to learn and acknowledge mistakes, and have a natural and insatiable curiosity for finding and profiting from inefficiencies. That’s just how they see the world: “What is misvalued or mispriced and how can I make money from that observation?”. We believe that managers with these characteristics are capable of generating consistent returns while also serving as good business partners.

With any security purchase investors should know how much they are paying (both in fees and illiquidity), and have an expected sense of the risk profile of the investment. In general, hedge funds have three return components: the strength of a manager’s investment ideas (alpha), the effect of market moves on a return (beta), and any borrowed capital required to generate or enhance returns (leverage). The risk-free rate also can impact returns to varying degrees depending on the market environment and strategy exposure. Although there is no magic formula to represent the perfect balance among these return drivers, investors should look for more impact from alpha generation than from beta or leverage to justify the relative illiquidity, increased monitoring requirements and higher fees of hedge funds.

From a value proposition perspective, balance between the general partner and limited partners matters. In general, it is reasonable for services that benefit the fund, such as audit, tax, legal, insurance, investment research and administration expenses to be picked up by limited partners, but other expenses (seen as business overhead costs) including research travel, investment-related legal, technology, marketing and base compensation should be covered by the general partner. Annual all-in carrying costs (exclusive of incentive fees) greater than 160 to 180 bps may be worthwhile in some circumstances but limited partners should be careful not to lose too much margin of safety (and also give up too much upside) when investing with a manager. Just because a manager generates strong returns does not mean limited partners must pay excessive fees and forgo an extra 25 or 50 bps annually.

To a certain degree, the concept of alpha has been lost in a recent market environment comprised of higher correlations across assets and narrower return dispersion across managers. Over the long term, investors who believe in active management understand that partnering with talented investment professionals adds value to diversified portfolios. The challenge remains constant: identifying the right partners and paying the right price for that alpha.

Footnotes