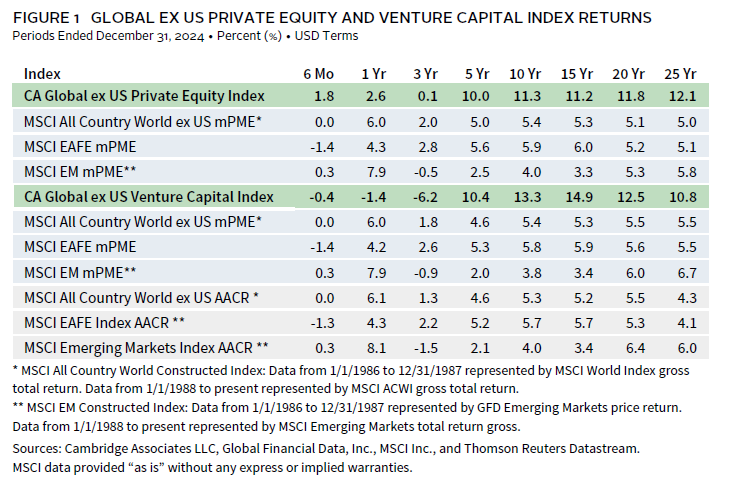

Like in the United States, private equity (PE) outperformed venture capital (VC) in ex US markets in 2024, with the Cambridge Associates LLC Global ex US Private Equity Index returning 1.8% and the Cambridge Associates Global ex US Venture Capital Index losing -0.4%, both in USD terms. With a strong US dollar, returns were much better when measured in euros; the PE index earned 9.4% and VC gained 5.2%. The ex US PE and VC indexes have now largely underperformed their public market counterparts (based on modified public market equivalent [mPME] returns) in the most recent three years (Figure 1). Still, both private asset classes retain their value proposition over the longer term.

Calendar Year 2024 Highlights

- The ex US PE index earned better returns than its VC counterpart, but private asset classes were bested by public markets. In general, less mature vintage years outperformed older ones, while sector and country-specific returns varied.

- Historically, the VC index has had a larger exposure to public companies, a trend that held in 2024. Based on market values as of December 31, 2024, public companies accounted about 10% of the ex US VC index and about 8% the ex US PE index.

Global ex US Private Equity Performance Insights

For the ex US PE index, 2024 was marked by many of the same trends from the prior two years. While the ex US PE index bested its VC counterpart, it fell short of public markets and US PE returns. Returns varied by vintage year, with the youngest vintages (2022–23) delivering the strongest calendar year returns and generally outperforming older funds. Distributions rose in 2024 and outpaced contributions, though distribution yields remained historically low. Investments in information technology (IT), financials, industrials, and healthcare all performed well, with the latter two sectors taking in the most capital during the year. Country-level returns were mixed: the United States (the largest country in the index) earned the highest return, China posted the lowest, and European countries ranged from negative to positive results. Japan, despite its small index weight, received a disproportionate share of capital, while China saw reduced inflows, highlighting shifting regional investment preferences amid ongoing economic and regulatory divergence.

According to Pitchbook, in 2024, 17 ex US PE-backed companies went public with a pre-value median of just more than $2 billion. This is a notable increase from 2023 in both count and value; there were 11 initial public offering (IPO) exits with a pre-value median of $117 million. The number of ex US PE-backed merger & acquisition (M&A) transactions fell to 2,009 in 2024, down from 2,166 in the previous year.

Vintage Years

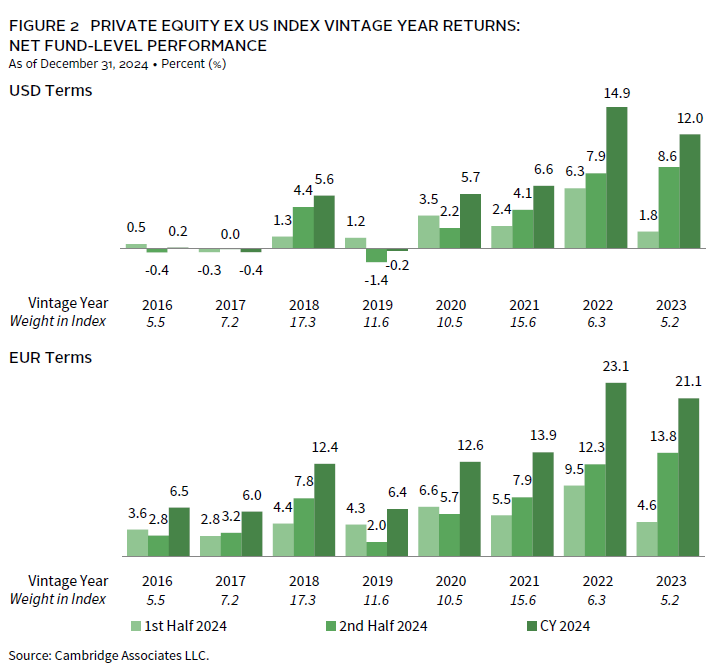

Returns for key vintage years (those that represented at least 5% of the index’s value) in the ex US PE index varied meaningfully based on fund age. The two youngest vintages (2022–23) posted the best calendar year returns, and younger funds mostly outperformed their older counterparts (Figure 2). The US dollar strengthened in 2024, particularly in the fourth quarter, which meant that returns were far better when measured in EUR terms. As a percentage of net asset value (NAV), funds from 2018 remained the largest at more than 18% of the index, but the massive 2021 vintage already accounted for more than 15%, a figure that has continued to increase as more capital has been deployed. Combined, the key vintages (2016–23) represented almost 80% of the index’s value and returned about 5% in USD terms and 12% in EUR terms.

While a variety of sectors influenced vintage year returns during the year, IT, healthcare, and industrials generally had the largest impacts. IT companies earned positive returns in all key vintages except for the worst-performing (2016). The best-returning vintage (2022) benefited from positive performance in all sectors except industrials. Healthcare companies were positive contributors in all but two vintages.

LP Cash Flows

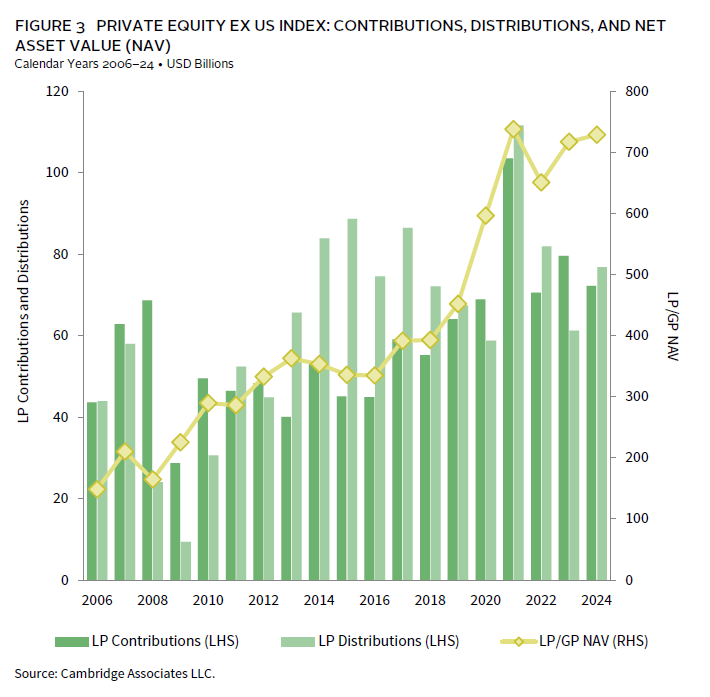

Distributions increased to $77 billion in 2024 and outpaced contributions, which decreased to $72 billion from the prior year. Since 2013, general partners (GPs) have returned more capital to limited partners (LPs) than they called in all but two years (Figure 3). While this is a healthy cash flow trend, the ex US PE index has now experienced three consecutive years of historically low distribution yields (annual distributions/beginning NAV). After an active fundraising, investment, and exit environment in 2021, growth rates have come down considerably and macro headwinds have created liquidity challenges.

During 2024, funds from vintages 2021–24 called more than $10 billion each. The 2024 vintage alone accounted for greater than $20 billion or 28% of all contributions. Funds from 2018—which represented the largest vintage in the index—returned close to $18 billion to LPs in 2024, or about 23% of all distributions. Vintages 2016–17 and 2019 also made up a meaningful share of distributions.

Sectors

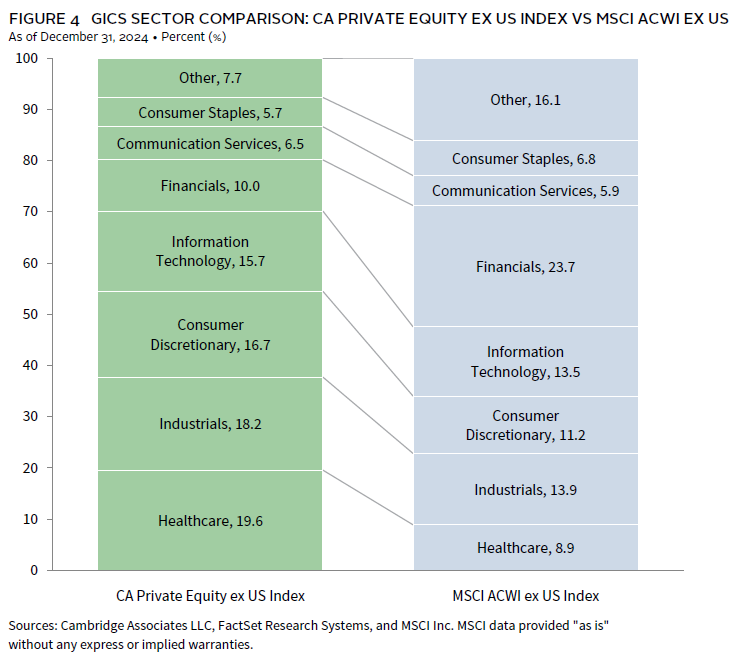

Figure 4 shows the Global Industry Classification Standard (GICS®) sector breakdown of the ex US PE index and a public market counterpart, the MSCI ACWI ex US Index. The chart illustrates differences in sector exposures, which help explain relative performance. The PE index has considerably less exposure to financials and more to healthcare, industrials, and consumer discretionary, while the public index has a slight underweight to IT. The ex US PE benchmark also has a significantly smaller share of capital allocated to IT relative to the US PE index, which could explain performance differences between the regions.

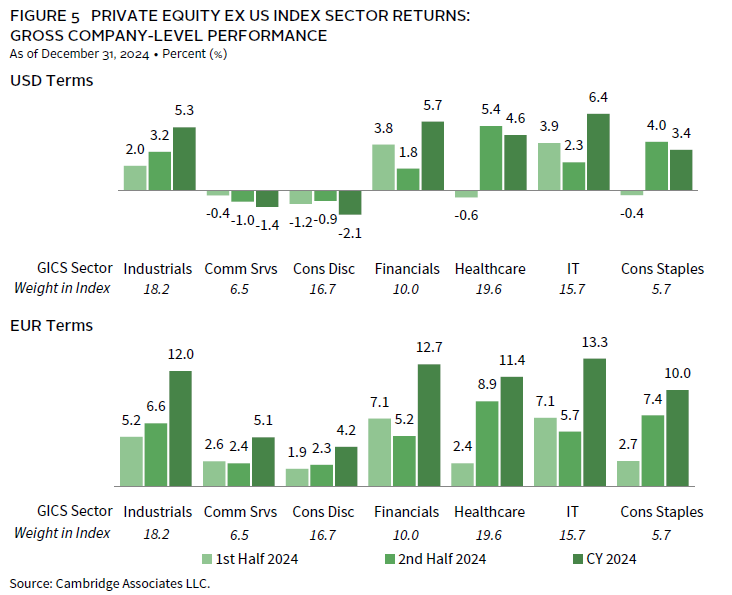

Five of the seven meaningfully sized sectors earned positive returns during 2024 and performance throughout the year varied (Figure 5). IT, financials, and industrials were the strongest sectors (in rank order), gaining more than 5% each. Healthcare—the largest sector by weight—also did well after earning more than 5% in the second half of the year. Collectively, the key sectors posted a pooled gross return of 3% in USD terms and 10% in EUR terms.

The two largest sectors by weight, healthcare and industrials, garnered the most capital during the year. Both took in a larger share of inflows relative to their size in the index; healthcare received 25% compared to its 20% weight and industrials received 22% compared to its 18% weight. Consumer discretionary, however, only received 13% of the capital despite being the third largest sector (almost 17% weight). Healthcare and industrials are often more resilient during market downturns, while money moves away from growth-oriented sectors like consumer discretionary.

Countries

Like vintage years and sectors, returns across countries ranged considerably. The largest country in the index (the United States) earned the highest return, while the second largest country (China) earned the lowest. The smaller European countries also had mixed performance, ranging from -2.9% for France to 7.0% for Germany-based companies (Figure 6). While Italy was a meaningfully weighted country after the first half of the year, it no longer met the 5% threshold by the end of 2024. China’s economy has underperformed broadly in the last few years, while the United States and Europe experienced a stronger recovery from the COVID-19 pandemic. Combined, the pooled gross return for all five countries was 3% (USD) and 9% (EUR).

Japan, despite representing less than 3% of the index, received 13% of the invested capital during the year. China, however, received just 6%, falling short of its long-term norm of 9%. Since 2022, less capital has flowed into China, while more money has flowed into Japan and South Korea. Although the ex US PE benchmark excludes US-based funds, more than 10% of capital invested by managers went into US-based companies in 2024. Businesses in the United Kingdom—which historically have received 16% of capital on average annually—garnered just 12% during the year.

Global ex US Venture Capital Performance Insights

For the ex US VC index, calendar year 2024 was marked by performance that, while only modestly negative, continued a now three-year trend of negative returns. Private markets meaningfully underperformed their public counterparts, and while the dollar value of distributions increased from the prior year, the index’s distribution yields for the past three years were the lowest on record. Annual performance in USD terms was flat to negative for most of the meaningfully sized vintage years, though currency effects led to much stronger returns when measured in euros. As is common in VC, sector overweights in IT and healthcare were significant, though returns for all meaningfully sized sectors were muted or negative. China—the largest country in the index by capital weight—experienced the worst performance of all meaningfully sized countries, while the United Kingdom (the third largest) returned nearly 40% in USD terms. The MSCI ACWI ex US Index earned 6.1% for the year, a meaningful outperformance over the private index. However, the ex US VC index still outpaced its public counterparts over the long term (Figure 1).

According to Pitchbook, 33 ex US VC-backed companies went public in 2024, with a pre-value median of just greater than $82 million. For comparison, in 2023, there were many fewer IPOs (14) with a pre-value median of about $68 million. With 2,232 deals, the number of ex US VC-backed M&A transactions rose a bit in 2024 from 2023, when there were 2,214.

Vintage Years

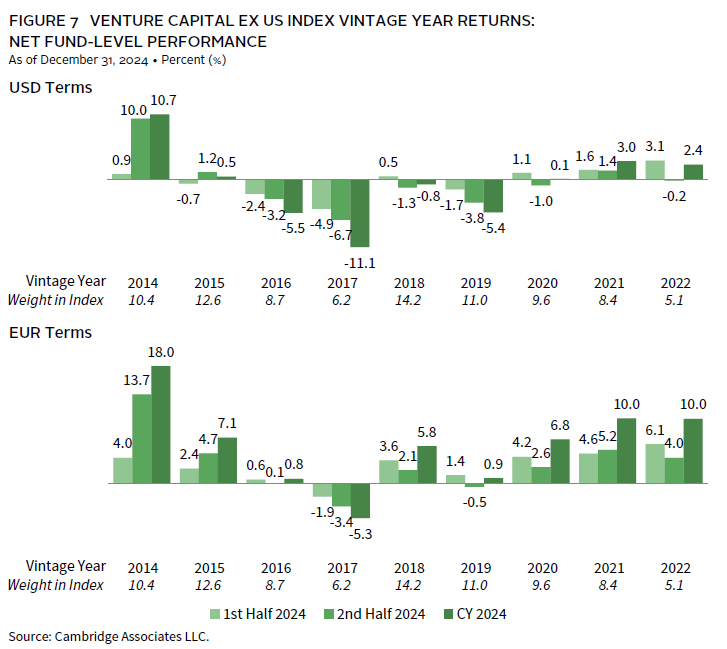

As of December 31, 2024, there were nine meaningfully sized vintages (those that represented at least 5% by capital weight) in the ex US VC index and together they accounted for 86% of the index’s NAV (Figure 7). Returns ranged from -11.1% for 2017 vintage funds to 10.7% for 2014 funds; performance was meaningfully better when measured in EUR terms, with 2017 and 2014 funds returning -5.3% and 18.0%, respectively.

For funds formed in 2014, the best-performing vintage year, performance was primarily driven by write-ups in its largest sector, IT, which were partially offset by modest write-downs in communication services and consumer discretionary. Performance for funds formed in 2017, the worst-performing vintage, was hampered by write-downs in consumer staples and healthcare. Mixed performance in its two largest sectors, healthcare and IT, drove performance for the largest vintage year, 2018, which represented nearly 15% of the index and posted a return of -0.8% for the year.

LP Cash Flows

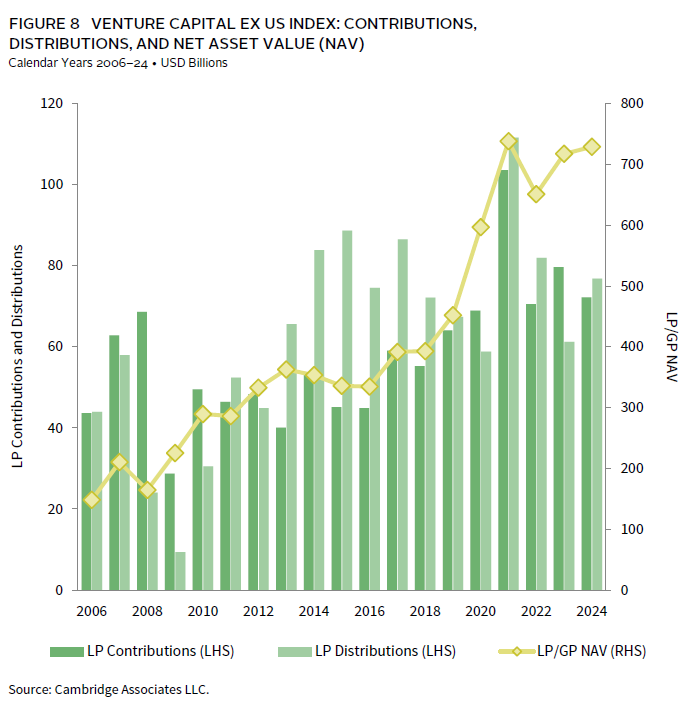

VC funds outside the United States called $7.7 billion and distributed $7.5 billion over the course of the year, which were 13% and 5% increases, respectively, from the prior year (Figure 8). Despite the increases, annual totals for both contributions and distributions were the second lowest since 2017, as a challenging macro environment continued to weigh on activity.

Almost 90% of the capital called during the year was from funds formed in 2020–24. Roughly 65% came from funds formed in 2021–22 alone, with those vintages calling $2.0 billion and $2.9 billion, respectively. Distributions were more widespread, with nine vintages accounting for 85% of total capital returned to LPs; each distributed at least $350 million during the year. Four vintages (2012, 2014–15, 2018) accounted for more than 50% of total distributions, with each returning more than $800 million.

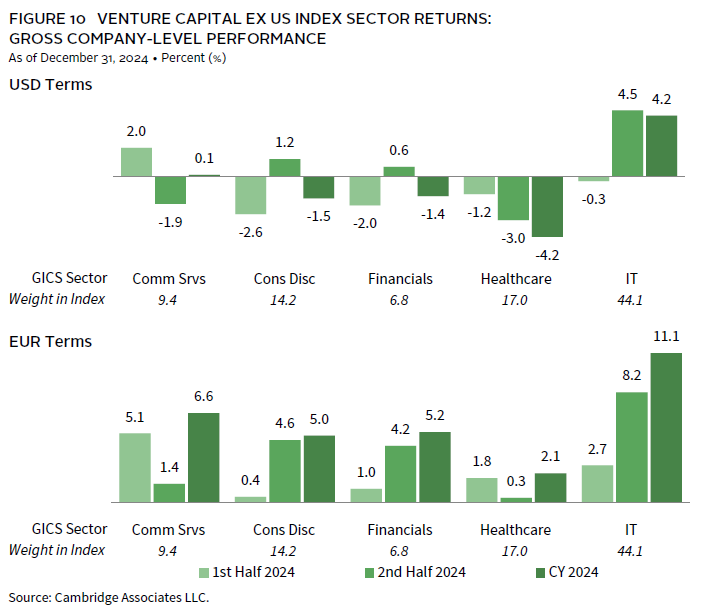

Sectors

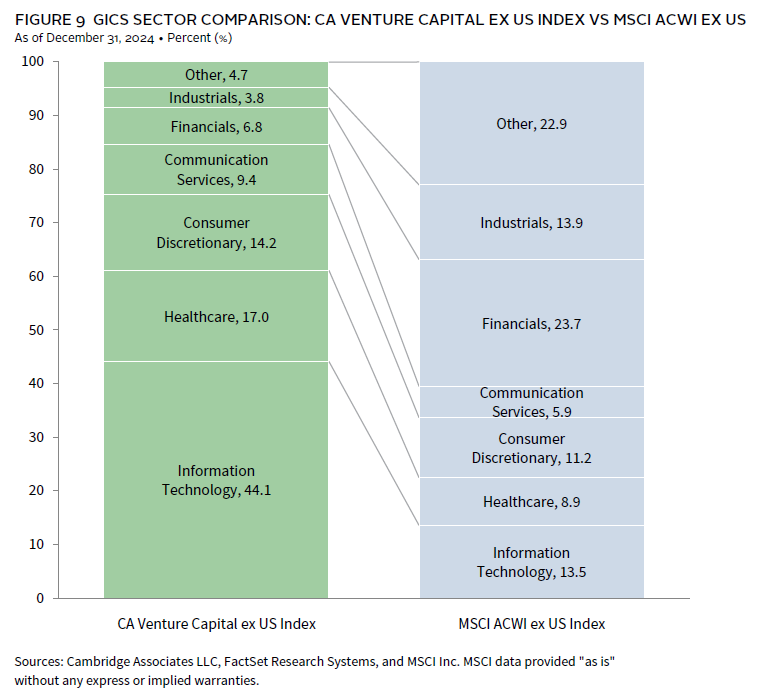

Figure 9 shows the GICS® sector breakdown of the ex US VC index and a public market counterpart, the MSCI ACWI ex US Index. The chart highlights some significant overweights in the ex US VC index, including in the IT, healthcare, consumer discretionary, and communication services sectors. The private market underweights are most significant in financials and industrials, respectively, as well as in consumer staples and materials (which are included in the “other” category).

Only two of the five meaningfully weighted sectors posted positive returns in USD terms during the year (Figure 10). IT (4.2%) was the best-performing sector, followed by communication services (0.1%). The two worst-performing sectors, healthcare and consumer discretionary, returned -4.2% and -1.5%, respectively. IT’s positive return was primarily driven by funds in the 2014 vintage. Healthcare performance was generally mixed across vintages but was negatively impacted by write-downs across several vintages (2011, 2015–17, 2019), while performance for the financials sector was pulled down by funds formed in 2013, 2017, and 2021. Performance for all key sectors was meaningfully better when measured in EUR terms. On a gross, dollar-weighted basis, the three largest sectors by market value—IT, healthcare, and consumer discretionary—accounted for 75% of the index and, together, returned 1.0% on a pooled basis, slightly above that of the other two meaningfully weighted sectors (-0.5%).

Companies in IT, healthcare, and consumer discretionary garnered 76% of the capital invested during 2024, just above the long-term norm of 73% for the three sectors. While the overall discrepancy between 2024 and the long-term norm was small, it was due to a significant increase in capital allocated to healthcare companies (36% compared to 26% long term), offset somewhat by a decreased allocation to consumer discretionary (6% compared to 11% long term).

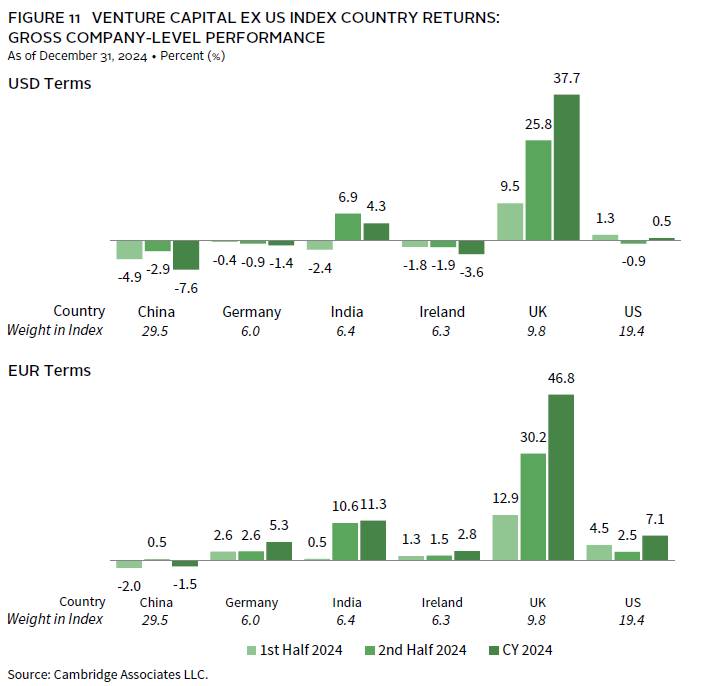

Countries

China was by far the largest country in the ex US VC index at the end of 2024 (Figure 11). Weights for the six meaningfully weighted countries ranged from Ireland’s 6% to China’s 30%. The United Kingdom (10%) and the United States (19%) were included, as were Germany and India, at 6% each. The United Kingdom posted the best annual return of the six; at 37.7% on a gross USD basis, it far outstripped the return for the next best-performing country, India, at 4.3%. The United States (0.5%) was the only other meaningfully sized country to eke out a positive return during the period, while China (-7.6%) was the worst performer of the group, just as it was in the first half of 2024.

Companies in Germany and India each garnered about 9% of the capital invested during year, slightly less than double the 5% of capital that each attracted over the long term. In contrast, China received substantially less capital than what it has over that long term, at 18% for the year, compared to 28% over the long term. The other four meaningfully weighted countries saw investment roughly in line with their long-term averages, with investments in the United States receiving the most (23%).

When combined, companies based in China, Germany, India, Ireland, the United Kingdom, and the United States returned 1.3% on a gross dollar-weighted basis during the year, outperforming the full index by 145 basis points.

Caryn Slotsky, Managing Director

Drew Carneal, Associate Investment Director

Wyatt Yasinski, Associate Investment Director

Figure Notes

Private equity includes only buyout and growth equity funds.

Global ex US Private Equity and Venture Capital Index Returns

The PE/VC indexes are pooled horizon internal rates of return and are based on limited partners’ fund-level performance; the returns are net of fees, expenses, and carried interest. Because the indexes are capitalization weighted, performance is mainly driven by the largest vintage years.

Public index returns are shown as both time-weighted returns (average annual compound returns) and dollar-weighted returns (modified public market equivalent). Returns are annualized, with the exception of returns less than one year, which are cumulative. The CA mPME replicates private investment performance under public market conditions. The public index’s shares are purchased and sold according to the private fund cash flow schedule, with distributions calculated in the same proportion as the private fund, and mPME net asset value is a function of mPME cash flows and public index returns.

Vintage Year Returns

Vintage year fund-level returns are net of fees, expenses, and carried interest.

Sector Returns

Industry-specific gross company-level returns are before fees, expenses, and carried interest.

Country Returns

Industry-specific gross company-level returns are before fees, expenses, and carried interest.

GICS Sector Comparisons

The Global Industry Classification Standard (GICS®) was developed by and is the exclusive property and a service mark of MSCI Inc. and S&P Global Market Intelligence LLC and is licensed for use by Cambridge Associates. Other includes sectors that make up less than 3% of the CA benchmark.

About the Cambridge Associates LLC Indexes

Cambridge Associates derives its ex US Private Equity and Venture Capital indexes from the financial information contained in its proprietary database of funds based outside the US. Those funds can still invest inside the US which explains the US exposure within both indexes. As of December 31, 2024, the database comprised 702 VC funds formed from 1986 to 2024 with a value of about $154 billion. Ten years ago, as of December 31, 2014, the index included 355 VC funds with a value of about $44 billion. As of December 31, 2024, the database comprised 1,249 PE funds formed from 1987 to 2024 with a value of about $729 billion. Ten years ago, as of December 31, 2014, the index included 860 PE funds with a value of about $353 billion.

The pooled returns represent the net periodic rates of return calculated on the aggregate of all cash flows and market values as reported to Cambridge Associates by the funds’ general partners in their quarterly and annual audited financial reports. These returns are net of management fees, expenses, and performance fees that take the form of carried interest.

About the Public Indexes

The MSCI ACWI ex US captures large- and mid-cap representation across 22 of 23 developed markets (DM) and 24 emerging markets (EM) countries. With 1,981 constituents, the index covers approximately 85% of the global equity opportunity set outside the United States. DM countries include Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, and the United Kingdom. EM countries include Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Kuwait, Malaysia, Mexico, Peru, the Philippines, Poland, Qatar, Saudi Arabia, South Africa, Taiwan, Thailand, Turkey, and the United Arab Emirates.