While valuations continue to support a tactical overweight to emerging markets equities today, the rationale for a permanent or structural overweight is weaker

- Many of the classic arguments for a strategic overweight to emerging markets (potential for faster economic growth, underrepresentation in indices, diversification, and inefficiency of markets) lack convincing support or have diminished in importance over time.

- The most enduring case for a strategic overweight is to earn a risk premium over investments in developed markets, supported by factors including less liquid markets, weaker institutional arrangements, governance, and transparency. This is simply another way of saying emerging markets equities need a valuation discount. The risk premium available is a function of the price at which investors choose to accept emerging markets risk, not an intrinsic, permanent part of emerging markets investment.

Please see our February 2014 Commentary Emerging Markets: Navigating Through Rough Waters.

Much has been written on the tactical case for overweighting emerging markets equities today, relative to policy, which is a position we have advocated and currently continue to support, based on valuation. Our focus in this research note, however, is different; it is to re-examine the case for a structural policy overweight in emerging markets equities relative to an index such as the MSCI All Country World Index (ACWI) within a portfolio’s long equity exposure. Around a decade ago it became fashionable in the higher circles of institutional investing to argue for a 50:50 split between emerging and developed equities, which is far different from their capitalization weights. Such strategies are rare in reality, but less extreme versions of structural overweight policies have become common. This research note examines how views of emerging markets have changed over the years, explores what drove their strategic role in portfolios, and takes a critical look at what emerging markets can and cannot do for portfolios today. Along the way we deal with some myths and misconceptions as well as implementation issues, all with the aim of outlining a more robust understanding of emerging markets equities.

What Are Emerging Markets?

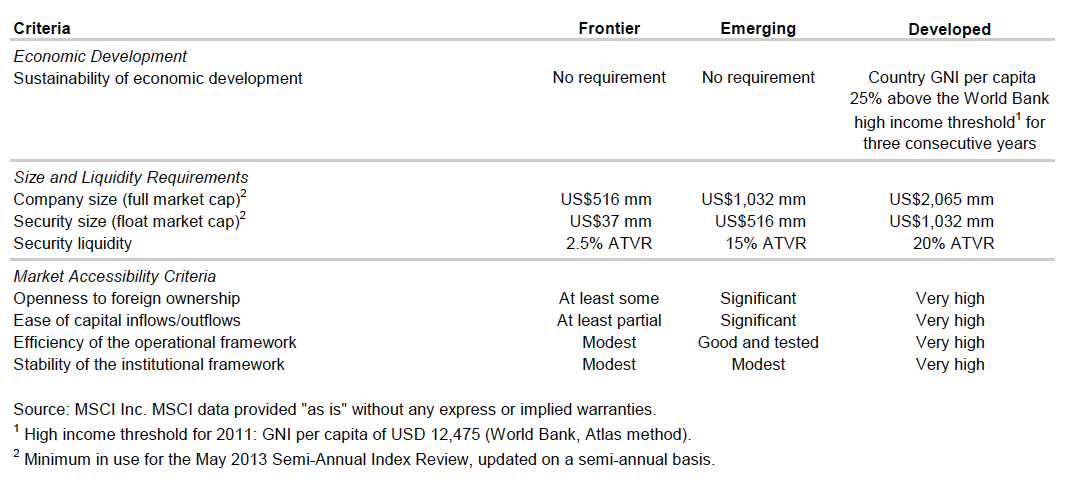

The term “emerging markets” is thought to have been coined, or at least popularized, in the 1980s by Antoine van Agtmael, a World Bank economist who went on to found the emerging equity manager EMM. In general usage the definition is both vague and somewhat shifting, conflating ideas of economic development, financial market liberalization, liquidity, and a whole host of others. Within equities, MSCI’s Emerging Markets Index is one of the most widely used benchmarks, so for investors its methodology necessarily defines emerging markets today. (As discussed later, definitions of emerging markets do change over time.) MSCI uses three criteria to decide whether to include a country in the developed, emerging, or frontier markets category:

- Sustainability of economic development

- Size and liquidity

- Access

Sustainability of economic development is proxied only by relative income levels. MSCI defines the threshold for developed country status as having a gross national income per capita 25% above the World Bank’s “high income” threshold for three consecutive years. In other words, to be an emerging market simply requires a country to be not particularly wealthy, with a reasonably sized and investable equity market, and where foreigners can allocate their funds and get their money out again. That’s what you are buying when you overweight emerging markets on an index basis and it is a thought worth retaining as we consider the case for doing so. MSCI’s methodology has no specific requirement for growth, realized or potential.

“Frontier” markets are defined using the same methodology, the cutoff from emerging markets being less onerous requirements for market infrastructure, liquidity, and access. Full details of the split are shown in the Appendix.

Why a Structural Overweight?

At the risk of stating the obvious, successful investment decisions require a very clear and specific justification for why the idea should work and what the expected outcomes are. This is important not just for the “big picture,” but also because implementation—putting the idea into practice effectively—requires a clear idea of the mechanisms involved: What inefficiency is being exploited? What is the purest way of achieving that? In the coming sections we assess a series of potential reasons for systematically favoring emerging markets stocks, derived from common reasons for investing in any class of stock:

- Faster (economic) growth

- Not properly represented in the index

- Diversification

- Inefficiency and potential for active management

- Earning a risk premium

Myth One: Investing in Growth

The notion of investing in growth remains the dominant narrative in the emerging markets story. A frequent investment committee discussion over the past 10 to 15 years has run as follows: Having just returned from visiting a particular emerging country for the first time (usually China, possibly Brazil), a committee member says, “Wow, you have no idea how dynamic this place is! There was so much going on, such entrepreneurial spirit, they work so hard, and this market is HUGE—we have to be investing there and much more than we are doing today.” Such thoughts tap powerfully into human emotion in two ways: First, they play to the enthusiasm for progress, improvement, innovation, and fresh opportunities; second, they work on back-of-the-mind fears prevalent in both the United States and Europe about imperial decline—the West has become complacent and lazy, lost its edge, etc. Seen from these perspectives, investing in emerging markets becomes an investment in the future. In other words, exactly where independent long-term investors should be leaders.

But successful investing always requires putting objectivity over emotion and so we ask: 1) Does investing in emerging markets give you growth? 2) Does economic growth matter for market returns?

Does investing in emerging markets give you growth? As noted earlier, the popular definition of emerging markets from MSCI doesn’t mention growth anywhere. Investors in the index are simply buying countries that are not rich, but are investible. Economic historians now tell us that while there seems to be an inexorable human tendency toward self-improvement, when looked at relatively speaking, rich countries tend to stay rich while poor countries stay poor.[1]See for example John Kay’s The Truth about Markets: Why Some Nations Are Rich But Most Remain Poor, Penguin Books Limited, 2004.

Wind the clock back to the 1980s, however, and investors were not talking about “emerging markets” but about Newly Industrialized Economies (NICs)—remember them?—synonymous at the time with the Asian Tigers of Hong Kong, Singapore, South Korea, and Taiwan. In 1993 the World Bank coined another term, High-Performing Asian Economies (HPAEs), including the Tigers plus Indonesia, Malaysia, and Thailand, and wrote a long report[2]The East Asian Miracle; Economic Growth Public Policy, A World Bank Policy Research Report, 1993. highlighting the common factors behind their high potential. These countries had all transitioned from agrarian to manufacturing bases by pursuing mercantilist policies: they prioritized exports over consumption, and had high savings rates they channeled into high rates of capital investment, which drove up labor productivity, value added, market share, and export revenue. This is a thumbnail sketch of what became known as the “East Asian Growth Model.” Earlier investors in what are now called emerging markets were more often than not investing in countries with a specific kind of economic model that was expected to transform their growth potential as it had done in Japan and then in the Tiger economies. The present MSCI definition of emerging markets brings in some of these countries in combination with natural resources–based economies with completely different dynamics as well as post-Soviet restructuring stories and others that fit into no particular category. In sum, there is nothing inherently “growthy” about today’s definition of emerging markets. Resource allocation, particularly capital allocation, determines whether a country follows a high-growth path and whether that growth delivers profits and earnings growth.

Does economic growth matter for market returns? A related, more powerful challenge to the growth argument is that the rate of economic growth has been irrelevant for investors when making decisions regarding market allocation. A number of academic studies have recently addressed this issue and one of the most comprehensive datasets available for doing so is that created by Elroy Dimson, Paul Marsh, and Mike Staunton (DMS) at the London Business School. They argued in their 2002 book, Triumph of the Optimists, that since 1900 a country’s relative stock market returns over the full period were inversely related to its GDP growth ranking, while in the post-war period the relationship was close to zero.

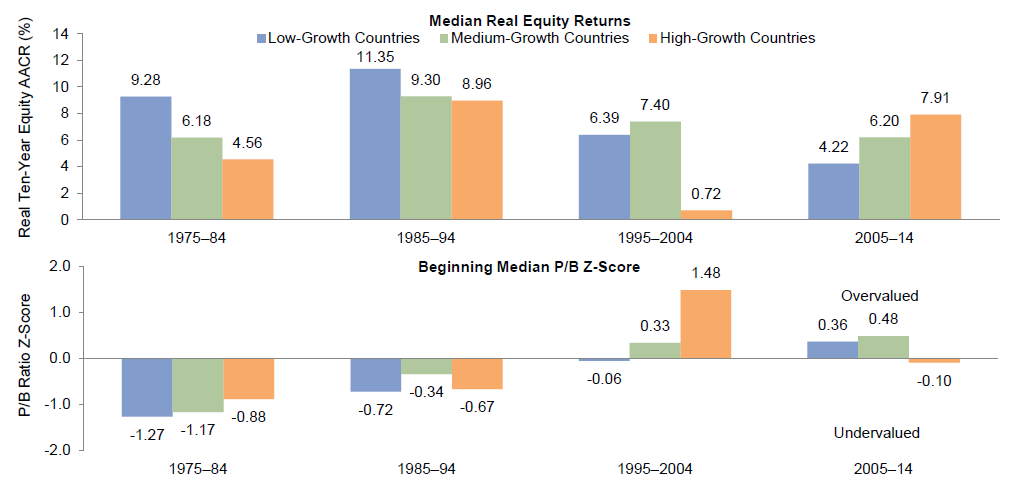

To replicate their conclusions with more familiar data, we took the MSCI indices and examined market performance grouped by high GDP growth countries and low GDP growth countries. We also controlled for valuation, which we will address later. The results are shown in Figure 1 and the conclusions match those of DMS. In three out of four decades since 1975, high GDP growth markets underperformed low-growth markets. The only period we examined when high GDP growth countries outperformed was when they started off cheaper.

Figure 1. Real Equity Market Returns and P/B Z-Scores for Low-, Medium-, and High-Growth Countries

1975–2014 • Local Currency

If this feels counterintuitive, it is worth bearing in mind the importance of capital efficiency: The ultimate driver of sustainable growth is return on equity. Say a company in a high-growth economy invests heavily; it will only generate earnings per share growth in the long run if it can invest above its cost of capital. In countries where investment is directed by the government into areas with limited productivity growth and where market signals are absent or distorted, GDP growth may result in a lot of output for a period but precious little return. State skill in allocating resources was arguably behind the success of some of the Asian Tiger countries and, by contrast, the failure of the Soviet Union. In the run-up to the previous emerging markets crisis in the late 1990s, however, emerging markets companies were typically earning lower return on equity (ROE) than those in developed countries (Figure 2), but still investing at a high rate despite the high cost of both equity and debt. High levels of low-return investment were a major contributor to that crisis—company governance and behavior seem to have improved since then, as have ROEs.

Figure 2. Return on Equity for Emerging Markets and Developed Markets

September 30, 1995 – May 31, 2014

We do not deny that a positive relationship could exist when a country accelerates past its expected GDP growth rate. In these cases, emerging markets equities may indeed benefit from the market “mispricing” anticipated economic growth, although with highly variable leads and lags. But this relationship has no bearing on the long-term strategic weighting to one set of countries over another.

Myth Two: Indices Underrepresent Emerging Economies

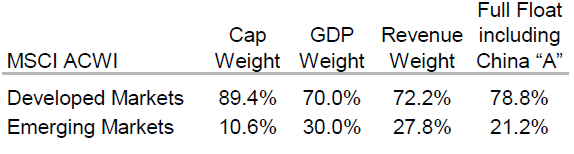

Emerging markets’ weight in the MSCI ACWI is 10% versus a contribution to global GDP of nearly one-third. This difference is behind arguments that indices “underrepresent” the economic weight of emerging markets and has often, plausibly, been advanced as a reason investors should make some adjustment to reflect this. Some active managers have criticized this idea, arguing that developed markets companies earn a significant share of their revenues and profits from emerging economies and this should be counted in exposure. This argument was anecdotal until recently, when MSCI launched a data series of geographic exposure by estimates of revenue source. Table 1 shows that viewed by revenue weight, the MSCI ACWI has emerging markets exposure very close to that implied by GDP weights. Admittedly, MSCI’s exposure data use some approximation. For companies where a geographic split of non-domestic revenues is not reported, MSCI approximates this by using—guess what—GDP weights. But we don’t have to rely on revenue exposure data only—the ACWI makes a free-float adjustment and excludes securities inaccessible to foreigners such as China “A” shares. Adding these back in, as in the last column of the table, by itself bridges around half the gap between GDP weighting and the capitalization-weighted ACWI. At the very least the underrepresentation argument is far less significant than originally thought, with the capitalization-weighted ACWI giving a reasonable approximation of the economic exposure.

Table 1. MSCI ACWI Constituent Characteristics

As of May 31, 2014

As investors digest this information, they should ask whether they are seeking exposure to emerging country economies or to emerging capital markets. The former can be achieved by investing in developed markets stocks, the latter cannot. We shall return to this point when we discuss the emerging markets “risk premium.”

Myth Three: Emerging Markets as Diversifiers

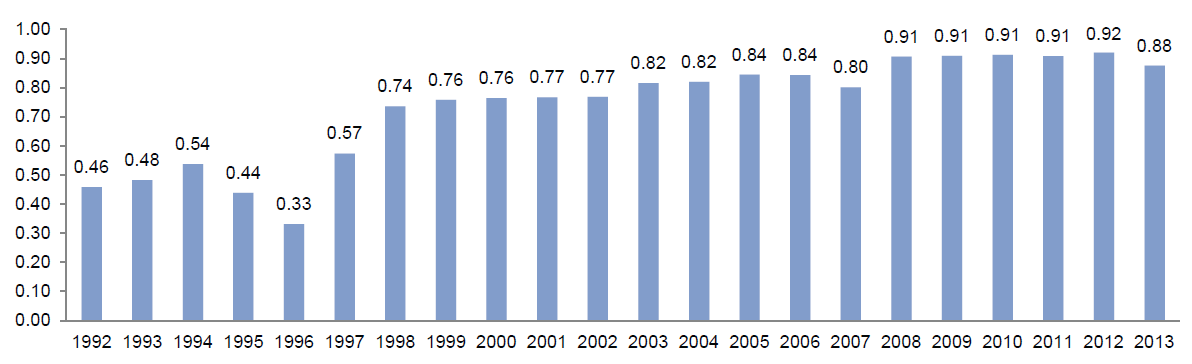

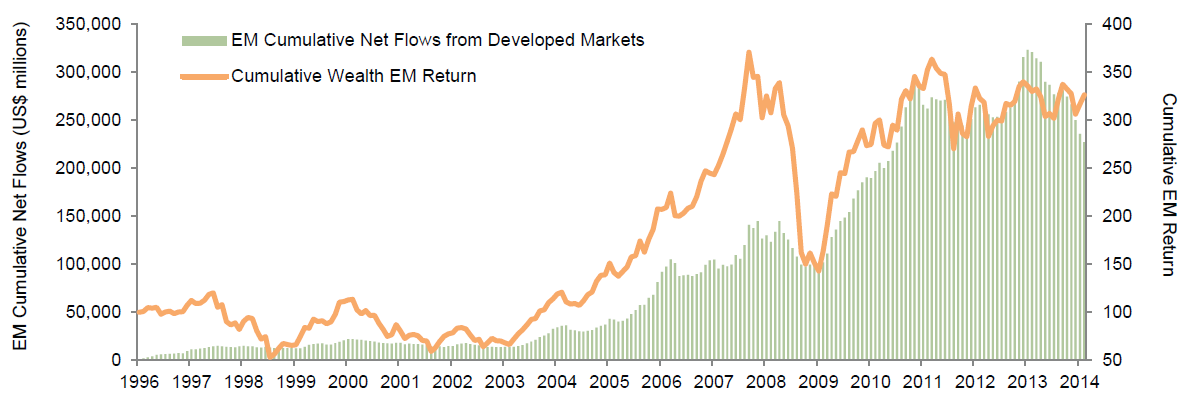

While not quite a myth, diversification from emerging markets equities is clearly not what it was. Correlations between emerging and developed markets have risen from below 0.5 in the early 1990s to more than 0.9 between 2008 and 2012 (Figure 3). The same rising trend has been seen in correlations between individual emerging markets. Of course the correlations between many assets and securities increased around the financial crisis, as is typical in volatility spikes. But there are reasons to suspect emerging markets will retain higher correlations with developed markets for a while yet: they have an increasingly common investor base. Investors and institutions from developed economies have substantially increased their exposure to emerging economies (Figure 4), making emerging capital markets increasingly geared to the swings of sentiment and risk appetite in the developed world. In his essay Skating Where the Puck Was, William Bernstein argues that true diversification is hard by definition; anything easy and liquid to implement is not diversifying because you will just be investing alongside everyone else. Emerging markets equity investing has progressively become more mainstream and low-cost exchange-traded funds have been available for emerging markets for some years now. Today, even frontier markets can be bought and sold minute-by-minute in the same way.

Figure 3. Correlations Between Emerging and Developed Markets

1992–2013

Figure 4. Emerging Markets Cumulative Net Asset Flows from Developed Markets vs Cumulative Emerging Markets Performance

February 29, 1996 – March 31, 2014

In 2013, however, nearly all (19 of 23) developed markets posted double-digit returns, and none were in the red, while in emerging markets over half had low (<5%) or negative returns. Surely that offers evidence of differential performance potential? Possibly, but DMS also present evidence that while developed markets crises are transmitted to the emerging world, the same does not happen in reverse. This makes intuitive sense given the data we have already examined on capital flows; for the time being, emerging markets remain the tail wagged by the developed capital markets dog.

Diminished diversification benefit does not, of course, mean that emerging markets should not occupy their capitalization-weighted fair share of the opportunity set, but it makes it harder to argue for a strategically larger role in the portfolio.

Myth Four: Active Management Is Easy

Even without a higher risk-adjusted return from market beta in emerging markets, an outsized allocation could be logical if one believes there will be an unusually large return to active management. We often hear market commentators declare “Emerging markets are so inefficient!” That may be so, but unfortunately it remains remarkably hard to identify active managers that can outperform meaningfully on a consistent basis.

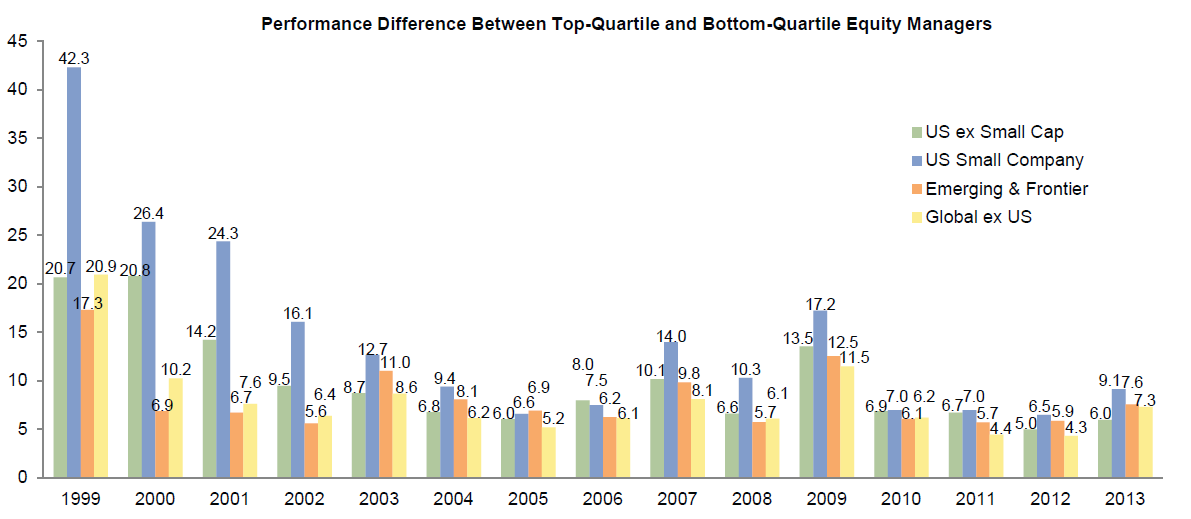

There are two ways of thinking about market efficiency and the active opportunity. Taking the first, the dispersion of outcomes between managers, high dispersion suggests a meaningful return from selecting the best managers as well as a high degree of idiosyncrasy in stock returns. Thus Treasuries exhibit very low manager dispersion, small-cap equities rather larger. Comparing manager dispersion through time in US, non-US, and emerging equities (Figure 5), it is hard to argue that emerging markets are more inefficient.

Figure 5. Manager Dispersion Comparison

1999–2013

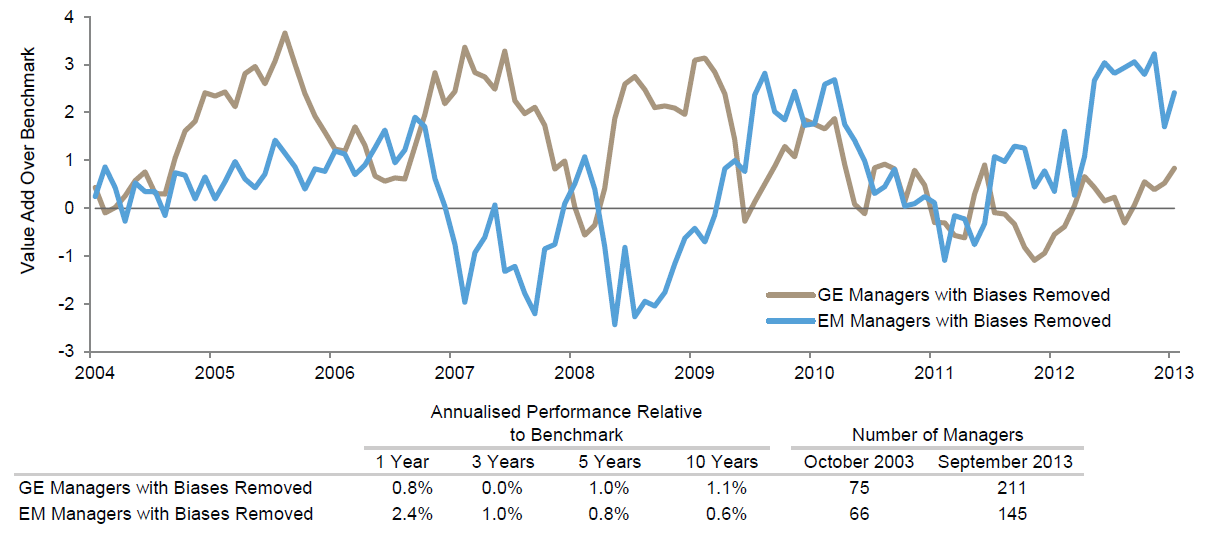

The second approach is to examine manager returns versus a benchmark. Figure 6 presents a ten-year history representing the equal-weighted average manager return[3]We use this metric rather than the median because our process for adjusting for manager bias means that the median manager would be different in each year, with some managers not present for the full … Continue reading in each year. This data set is adjusted as far as possible for back fill and survivorship bias; for example, it includes data from managers that ceased operating during the period. While the average emerging markets manager’s excess return (gross of fees) was positive, it was rather modest and over five- and ten-year periods was less than that achieved by the average manager with a broad global equity mandate.

Figure 6. Rolling 12-Month Returns of Active Managers Relative to the MSCI World and MSCI Emerging Markets Indices

October 31, 2004 – September 30, 2013

This discussion is not intended to suggest there are no compelling alpha opportunities in emerging markets. We have focused on global emerging markets mandates, which are arguably the hardest to manage and resource given the hugely disparate group of countries represented. Managers with a regional or even country focus may find it easier to build an information or analytical edge. Referring back to the discussion on investing in growth, strategies that seek out more specific market characteristics in terms of a development model or institutional/policy framework may perform better. Further, and in a different vein, the DMS research also suggests that simple value strategies work remarkably well in emerging markets. Whether one regards the value effect as inefficiency or a pure risk factor, it would still provide a tailwind with respect to the cap-weighted index. Finally, even if the diversification benefits of emerging markets have been diluted by capital flows into core or index products, particular active approaches may be able to recover some of that benefit by focusing on smaller stocks or adopting a distinctive sector focus.

Not a Myth: The Emerging Markets Risk Premium

We have now examined four of the hypothetical justifications for a strategic emerging markets overweight and found them lacking in convincing support from the data or diminished in importance over time. The final potential justification we asserted was the risk premium associated with investing in emerging as opposed to developed markets.

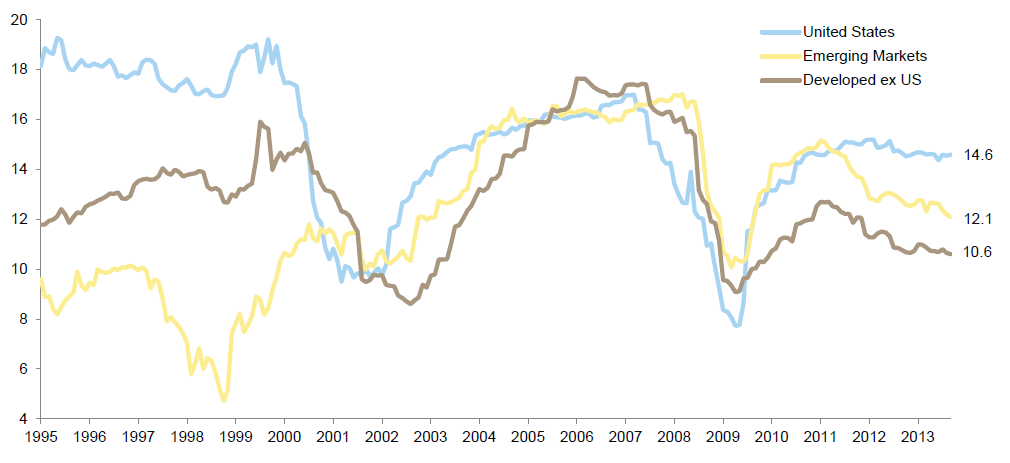

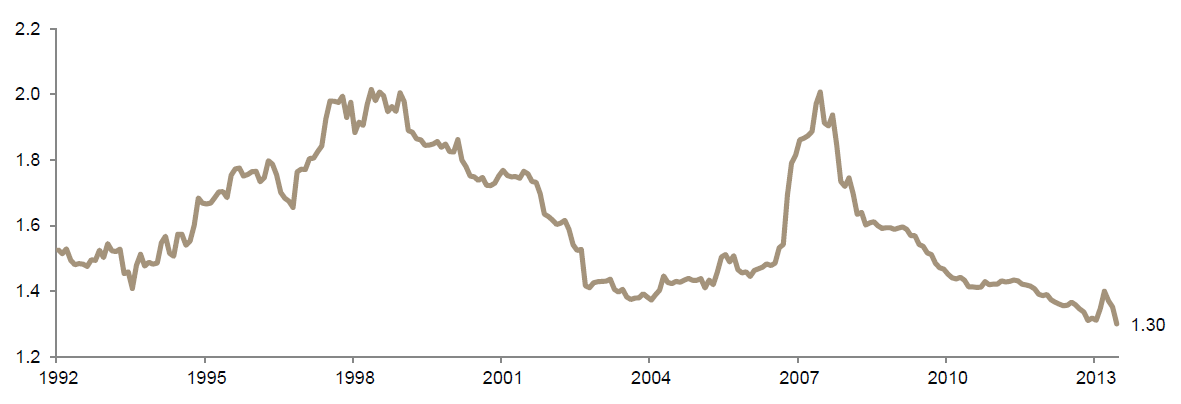

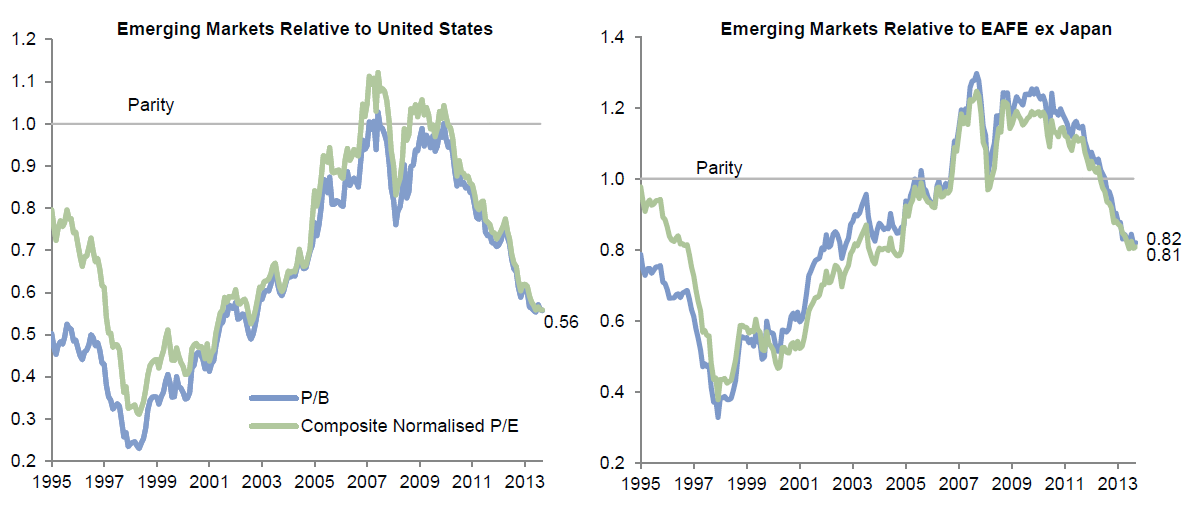

The concept of an emerging markets risk premium is rather analogous to the so-called small-cap effect and the idea is quite well supported: while relative volatility has declined, emerging markets are still more volatile than developed markets (Figure 7). Clear qualitative factors support this being the case: less liquid markets, weaker institutional arrangements, governance, and transparency to name but some. Particularly given the rise in correlation and reduced diversification benefit, investors accepting emerging markets equity risk should demand a higher return than for developed markets. And so they have done, most of the time: emerging markets have almost always traded at a meaningful discount to developed markets based on the normalized P/E ratio (Figure 8). This valuation discount should give investors a higher return over time irrespective of differential growth rates. But, remember the causality here—a positive risk premium is a function of the price at which investors choose to accept emerging markets risk, not an intrinsic quality of the market. An investor might justify an overweight to emerging markets for this reason, but make it conditional on valuation and adopt a tactical underweight if the valuation discount shrinks substantially or disappears.

Figure 7. Relative EM/DM Rolling Five-Year Volatility

December 31, 1992 – May 31, 2014

Figure 8. Emerging Markets vs Developed Markets Valuations

September 30, 1995 – May 31, 2014

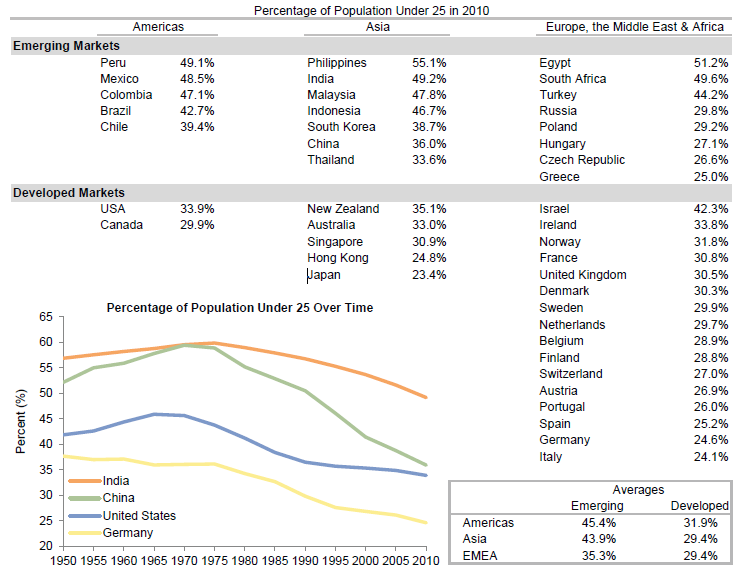

What About Demographics?

We have now considered all five of our initial “strategic” arguments for an overweight to emerging markets. Proponents of emerging markets have one final trump card to play against skeptics: demographics. Here we return to a growth-related argument and one that plays to some of the darkest financial fears of investors in Europe, Japan, and even the United States: a shrinking cohort of working people supporting an ever-larger proportion of dependents and unsustainable public finances. A country whose working-age population is stable or improving is potentially in a much better position to support investment and sustainable public finances. Demographics are a long-term factor, however. In market terms, will they make a difference on a time horizon over which investment committees and CIOs are held accountable? Even setting aside the time horizon question, the demographic situation is more complex than just young, growing populations in emerging countries versus old, shrinking populations in developed countries. Figure 9 lays out some of the data, focusing on the proportion of the population under 25. From it we draw the following messages:

- In recent years, demographics have changed for the worse across many economies, developed and emerging;

- At the high-income end of emerging markets, a number of countries are converging on figures common in developed countries; and

- Russia and the post-Soviet Eastern European “emerging” economies have some of the worst demographics in the world.

Focusing on the population under 25 is only one aspect of demographics, but it is a good proxy for the difference between young and growing populations and those where the birth rate has fallen below replacement levels. Positive demographics can provide a growing market and ease public fiscal burdens, but only if the growing potential workforce can be employed productively. This depends on developing human capital (education) and physical capital (investment) to drive productivity growth, rising incomes, and rising demand in a self-reinforcing process. If demographics were sufficient on their own, Africa would contain some of the world’s most successful economies. This brings us back to the earlier point that sustainable growth is a function of efficient resource allocation, which in turn depends on policies and institutions.

Figure 9. Emerging and Developed Markets Demographics

Conclusion

We set out to test the concept of a strategic overweight to emerging equity markets, compared with those of developed economies. We examined the major arguments in favor and found the empirical support for all but one either lacking or significantly diminished compared with the 1990s. The one point that remains robust is that emerging equity markets are riskier; they should be and generally are priced at a discount to developed markets. While this discount exists, other things being equal, investors should expect higher compound returns from emerging markets alongside higher volatility, the potential for differential future growth rates notwithstanding. For some investors, depending on their return needs and risk tolerance, this alone may be enough to justify a semi-permanent overweight, always supposing that the discount remains.

This discussion applies to global emerging markets broadly defined, in a manner similar to the MSCI index. For a portfolio that does not simply replicate the emerging markets index, this paper has revealed further questions that can only be answered by considering the nuts and bolts of implementing an emerging markets allocation:

- If public markets do not deliver the benefits of faster economic growth, can private investments?

- Can active managers increase the odds of receiving a diversification benefit?

- In portfolios with high allocations to hedge funds and private investments, where exposure to emerging markets may be limited, is a structural overweight to emerging markets equities justified to lift the portfolio’s overall exposure to emerging markets to an appropriate level?

- What drives the higher volatility of emerging markets? If this is mainly a currency effect, as some studies suggest, are there other ways of earning the risk premium?

- Will frontier markets fall victim to the same loss of diversification as they become more mainstream and capital flows increase?

In conclusion, we are skeptical of many of the reasons proposed for giving emerging markets a permanent overweight in a portfolio’s strategic asset allocation. For some investors we can see that a strategic overweight would make sense to harvest a long-term risk premium, but to be successful this strategy needs regular monitoring of valuation and a willingness to temporarily reduce in the event the risk premium on offer shrinks or disappears. In the absence of such a strategic decision, emerging markets nevertheless deserve to claim their fair share of the opportunity set: Unless an investor has decided to build in a permanent structural overweight, we propose that the neutral position for a policy allocation to emerging markets equity within broader equity (or equity-like) exposure should surely be its capitalization weight. Investors should default to benchmarking to the MSCI ACWI for the long-only equity portion of their portfolios, not the (developed-only) MSCI World Index.

As with all asset classes, investors should regularly examine the reasons for owning emerging markets equities and recognize that the single best reason is that an asset is cheaply priced. Price always trumps myths.

Appendix

Appendix. MSCI Market Classification Framework

As of June 2013

Contributors

Simon Hallett, Managing Director

Alexandra Meyer, Senior Investment Associate

Exhibit Notes

Figure 1. Real Equity Market Returns and P/B Z-Scores for Low-, Medium-, and High-Growth Countries

Sources: International Monetary Fund, MSCI Inc., and Thomson Reuters Datastream. MSCI data provided “as is” without any express or implied warranties.

Notes: For the 1975–84 and 1985–94 periods, countries in the sample include: Australia, Canada, France, Germany, Japan, Norway, Sweden, the United Kingdom, and the United States. For the 1995–2004 and 2005–14 periods, countries in the sample include those previously mentioned and the following: Brazil, Chile, China, Colombia, Malaysia, Mexico, the Philippines, South Korea, and Thailand. Equity market returns reflect total returns of MSCI country indexes in local currency adjusted for inflation. Total returns for MSCI developed markets indexes are net of dividend taxes. UK inflation data are represented by the UK RPI until 2003 and the UK CPI from 2004 to the present. Z-score represents the number of standard deviations above or below the historical average valuation. Returns data for 2014 are through April 30. 2014 GDP estimates provided by the IMF.

Figure 2. Return on Equity for Emerging Markets and Developed Markets

Sources: MSCI Inc. and Thomson Reuters Datastream. MSCI data provided “as is” without any express or implied warranties.

Note: Developed ex US represents the MSCI EAFE ex Japan Index.

Table 1. MSCI ACWI Constituent Characteristics

Source: MSCI Inc. MSCI data provided “as is” without any express or implied warranties.

Note: Revenue weights as of December 31, 2013.

Figure 3. Correlations Between Emerging and Developed Markets

Sources: MSCI Inc. and Thomson Reuters Datastream. MSCI data provided “as is” without any express or implied warranties.

Note: Correlations of returns in US$ terms over a 60-month period to end of year shown.

Figure 4. Emerging Markets Cumulative Net Asset Flows from Developed Markets vs Cumulative Emerging Markets Performance

Sources: EPFR, MSCI Inc., and Thomson Reuters Datastream. MSCI data provided “as is” without any express or implied warranties.

Notes: Data are monthly. Cumulative net flows from developed markets represents fund flows to EM funds from developed markets investors.

Figure 5. Manager Dispersion Comparison

Source: Cambridge Associates LLC.

Notes: Cambridge Associates LLC’s (CA) manager universe statistics are derived from CA’s proprietary Investment Manager Database. Performance is generally reported gross of investment management fees. Managers that do not report in US dollars, exclude cash reserves from reported total returns, and have less than $50 million in product assets (for 1998 to the present) are excluded. Returns for inactive (discontinued) managers are included if performance is available for the entire period measured. Statistics are not reported for universes with fewer than ten managers. Data pulled using a simple average.

Figure 6. Rolling 12-Month Returns of Active Managers Relative to the MSCI World and MSCI Emerging Markets Indices

Sources: Cambridge Associates LLC and MSCI Inc. MSCI data provided “as is” without any express or implied warranties.

Notes: Cambridge Associates LLC’s (CA) manager universe statistics are derived from CA’s proprietary Investment Manager Database. Performance is generally reported gross of investment management fees. Managers that do not report in US dollars, exclude cash reserves from reported total returns, and have less than $50 million in product assets (for 1998 to the present) are excluded. Returns for inactive (discontinued) managers are included if performance is available for the entire period measured. Statistics are not reported for universes with fewer than ten managers. Data pulled using a simple average. Performance of global equity managers has been measured relative to the MSCI World Index while that of EM managers has been measured relative to the MSCI Emerging Markets Index.

Figure 7. Relative EM/DM Rolling Five-Year Volatility

Sources: MSCI Inc. and Thomson Reuters Datastream. MSCI data provided “as is” without any express or implied warranties.

Notes: Data are monthly. Developed markets are represented by the MSCI World Index and emerging markets are represented by the MSCI Emerging Markets Index.

Figure 8. Emerging Markets vs Developed Markets Valuations

Sources: MSCI Inc. and Thomson Reuters Datastream. MSCI data provided “as is” without any express or implied warranties.

Notes: The composite normalised price-earnings (P/E) ratio is calculated by dividing the infl ation-adjusted index price by the simple average of three normalised earnings metrics: ten-year average real earnings (i.e., Shiller earnings), trend-line earnings, and return on equity–adjusted earnings. All data are monthly. CPI-U, CPI-G7, and emerging markets inflation data are as of April 30, 2014.

Figure 9. Emerging and Developed Markets Demographics

Sources: MSCI Inc. and the United Nations. MSCI data provided “as is” without any express or implied warranties.

Notes: Data from 2012 UN World Population Prospectus. Countries listed are included in either the MSCI World or MSCI Emerging Markets indices as of April 30, 2014.

Footnotes