Executive Summary

- The Gulf region’s rapid rise in wealth over the past two decades has prompted increasing demand for Shariah-compliant offerings. While a full suite of solutions for institutional investors is still developing, the opportunity set today is sufficient to build a Shariah-compliant portfolio that offers growth, some diversification, and some protection against macroeconomic risks.

- Institutional investors look at a wide variety of asset classes when considering how to build a portfolio that meets their risk and return objectives, including equities, bonds, real assets, hedge funds, and private equity. A portfolio aligned with Shariah principles will need to make investments using specific transaction types created to facilitate Shariah-compliant investing.

- Shariah-compliant equity investing is possible today, with the creation of indices and funds that screen companies and subsidiaries for appropriateness, usually overseen by a board of Shariah scholars.

- Traditional government bonds and other forms of credit that pay interest typically are not Shariah compliant. Sukuk, which use a specific structure to comply with Shariah principles while providing a stream of income similar to a bond, are an option. The small size of the Sukuk market today makes large-scale investment challenging, but the market is changing rapidly.

- Investors should evaluate the real assets space carefully for Shariah compliance and practicality. Real estate investment opportunities exist, with closed-ended real estate transactions permissible if structured by an Islamic bank with the ability to create financing arrangements outside the typical leverage structure. Shariah-compliant REITs have begun to enter the market, but volatility in this space remains high. Commodity investments, while possible to structure according to Shariah principles, can carry high transaction costs and often involve storage of physical goods, impractical for many investors. The universe of institutional-quality Shariah-compliant funds focused on natural resources equities is very small.

- Hedge funds are generally not permissible in Shariah-compliant portfolios due to their speculative nature and use of leverage. Private equity investments, specifically leveraged buyouts, are similarly difficult to structure in accordance with Shariah principles. Growth equity and venture capital funds are more likely to be compliant, but Shariah-compliant investors will likely need separate consideration of underlying company investments.

- Given the available options, a Shariah-compliant portfolio will differ markedly from the composition of a conventional portfolio. The limitations on institutional-quality investable products create some constraints for investors, who should be prepared for returns lower than those of conventional peer portfolios. However, the opportunity set is evolving, and we continue to actively monitor the landscape.

The last two decades have seen increasing demand for Shariah-compliant asset management from institutional and private investors in the Gulf Cooperation Council (GCC) countries, partly driven by the rapid rise in the region’s wealth during the 2000s, but also by the increasing number and breadth of asset classes now available for Islamic investors. International banks—including Citigroup, Deutsche Bank, HSBC, Standard Chartered, and UBS—and other institutional asset managers have seized the opportunity to adapt their existing services to the needs of Islamic investors, and many have appointed their own boards of Shariah scholars to assure their clients that their products are indeed Shariah compliant. This has been a learning experience for the managers themselves as well as for Islamic investors, the former learning about Shariah principles, the latter about new asset management options.

In this paper we review the principles of Shariah-compliant investing and define the key financial transactions, provide a brief overview of the Islamic capital market, and discuss the opportunities for Islamic investors to build a Shariah-compliant portfolio using modified versions of more ‘traditional’ asset classes and some unique to Islamic investing. While the financial industry still has a ways to go to offer a full range of diversified products and institutional-quality managers to Islamic investors, the opportunity set today is sufficient to build viable Shariah-compliant portfolios that offer growth, diversification, and some protection against macroeconomic risks as we show in the paper’s final section.

Principles of Shariah-Compliant Investing

Islam permits investment in a wide variety of assets, as long as the source of wealth generation does not breach Islamic principles—that is, the activities are halal, or permissible, zakat (a religious tithe) is paid, and wastefulness is avoided. The basic principle underlying Islamic financial transactions is that the purpose of financing should not involve an activity prohibited by Shariah (Islamic law). In essence, the financing must not involve riba (the giving or receiving of interest) and should avoid gharar (uncertainty, risk, and speculation). Riba includes interest charged on lending money whereas gharar includes excessive uncertainty regarding essential elements of a contract, such as price in a contract of sale.

Islamic finance also promotes the sharing of risk and reward between contracting parties. The degree of risk to be shared varies by contract. An example of financing that involves a relatively high degree of risk-and-reward sharing is venture capital; by contrast, a contract that has a relatively low degree of risk-and-reward sharing is the sale of an asset on instalment credit.

Some of the most important Shariah-compliant financial transaction types include:

- Murabaha: A type of transaction where a customer requests an intermediary (e.g., a bank) to buy a product and sell it to him or her at cost plus a mark-up. The mark-up compensates the bank for transaction costs (incurred during the procurement process) as distinct from interest.

Usage: Fixed income or cash transactions.

- Mudaraba: A contract that covers the relationship between the owner and manager of assets. Under the Mudaraba model, the owner bears all losses of invested assets, with any future expected profits shared between the owner and manager at a preagreed ratio. The manager is not allowed to take any form of remuneration other than profit share, and technically has no recompense for its efforts unless the project is profitable. However, a guaranteed wage can be and often is agreed upon.

Usage: Public equity or real estate transactions.

- Musharaka: A structure for joint-venture investments, where two or more parties coinvest in a business venture. The ratio for profit sharing is predetermined and losses are shared according to each party’s equity stake. The loss-sharing feature differentiates Musharaka from Mudaraba.

Usage: Venture capital or private equity transactions.

The Islamic Capital Market

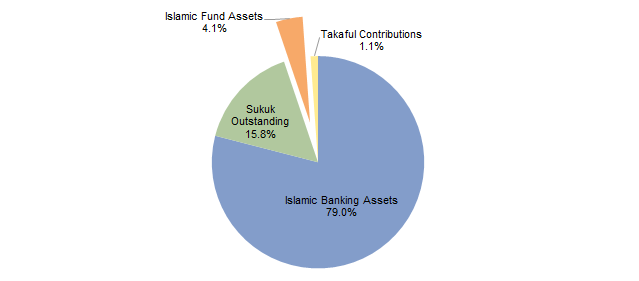

The Islamic financial services industry includes Islamic banking, that is, banking based on Shariah principles; Sukuk, a form of Islamic debt obligation similar to bonds; Takaful contributions, a cooperative system of reimbursement with some similarities to insurance; and assets in Islamic (i.e., Shariah-compliant) funds. Islamic banking has been the driving force of the global Islamic finance industry, given the growth of Islamic banks across the GCC and Southeast Asia, while the Sukuk market has also seen rapid recent growth. Islamic asset management remains a niche segment of the Islamic financial services industry despite strong recent growth. A complete picture of the market is hard to come by, but based on a review of several sources, the total number of Islamic funds has risen from 285 in 2004 to 1,161 through third quarter 2014, while assets under management were estimated to be US$75.8 billion through third quarter 2014. However, this constitutes an estimated 4% of global Islamic finance assets (Figure 1).

Figure 1. Distribution of Global Islamic Financial Assets

As at Third Quarter 2014 • Weight (%)

Sources: Bloomberg L.P., central banks, corporate communications, individual institutions, Islamic Financial Services Board, Kuwait Finance House Research, regulatory authorities, The Banker, and Zawya Thomson Reuters.

Note: Data are estimated based on a review of the sources listed.

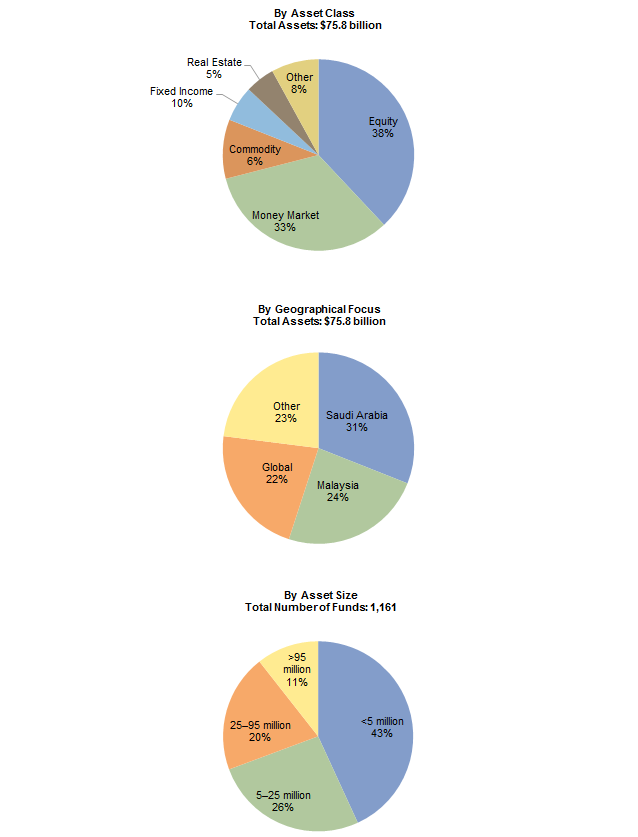

Within the Islamic funds space, equity funds constitute 38% of the overall market, the largest component (Figure 2). These are followed by money market funds (33%), commodity funds (10%), and fixed income funds (6%). By country and region, Southeast Asia is a clear investment focus, with about a quarter of fund assets invested in Malaysia (Figure 2).

Perhaps the biggest constraint in the Islamic asset management space is its current size. The largest proportion of Islamic funds remain small (less than $5 million in assets under management), which suggests limited opportunities for large, institutional-quality investors to access the market (Figure 2).

Figure 2. Global Islamic Fund Assets

As at Third Quarter 2014

Sources: Bloomberg L.P., Islamic Financial Services Board, Kuwait Finance House Research, and Zawya Thomson Reuters.

Notes: Data are approximated. By asset class ‘other’ includes alternative (1%) and mixed allocation (7%) asset classes. By geographical focus ‘other’ includes US (7%), MENA (4%), Asia Pacific (3%), GCC (2%), Kuwait (1%), Indonesia (1%), South Africa (1%), Pakistan (1%), plus additional geographical regions (2%).

Building a Portfolio Using Shariah Investment Principles

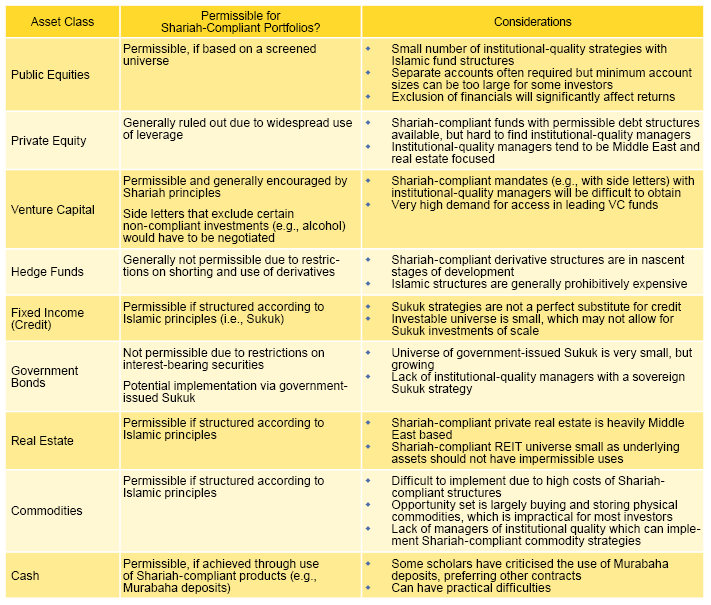

Institutional investors look at a wide variety of asset classes when considering how to build a portfolio that meets their risk and return objectives, including equities, bonds, real assets, hedge funds, and private equity. In this section we discuss each of these asset classes and the implications of Shariah compliance. Given the evolving methods for making investments based on Shariah principles, determination of a particular fund or investment’s Shariah compliance is often dependent on review by Shariah scholars (see sidebar). Some asset classes, such as hedge funds, are generally not compliant with Shariah principles and are not viable options for Shariah-compliant portfolios today. Others, such as equities, can be Shariah compliant using the specific transaction types discussed earlier and if particular types of stocks are avoided. Although the opportunity set is still growing, many of the asset classes we will discuss do have viable Shariah-compliant options.

Overview of Islamic Regulators and Scholars

The Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) and the Islamic Financial Services Board (IFSB) are the two main regulatory bodies that oversee the Islamic asset management space. Both bodies have attempted to develop global industry standards to encourage harmonization of Islamic finance practices, with the IFSB focused more on the identification, management, and disclosure of risks relevant to Islamic products and operations, while the AAOIFI focuses on best practices for reporting, as well as governance issues specific to Shariah-compliant institutions.

Despite the efforts of both of these organizations, the industry continues to suffer from a lack of standardization and is reliant on individual Islamic scholars that deem products, services, and processes as being Shariah compliant. Many Islamic fund managers therefore require their own Shariah boards to ensure their products have the required backing within the Islamic finance community.

Many boards consist of the same five or six established Shariah scholars. The cost of establishing Shariah compliance for individual securities and for investment vehicles can be very expensive. A portion of the manager’s fee is used to pay the Shariah compliance board and scholars. While the disparity is closing, the large number of Shariah boards and scholars has resulted in a range of criteria of what constitutes a Shariah-compliant product.

Public Equities

Equity investing (profit distribution through share ownership) is intrinsically well aligned with Islamic principles, provided that the business is itself halal. Industry and financial screens can help determine a permissible set of companies and investments. Such screens evaluate companies’ underlying business activities and determine whether their exposures comply with Shariah guidelines. The screen would examine the finances and revenues of a company’s subsidiaries to eliminate haram businesses (income of more than 5% from non-Shariah-compliant activities) from the universe. Examples of non-compliant businesses include conventional finance and insurance; alcohol; tobacco; pork and other non-compliant food-related businesses; gambling; entertainment services such as cinemas, music, adult entertainment; and defense and weapons firms.

Further, while companies that are Shariah compliant must derive income from halal activities, they must not fund their operations using more than what is deemed as an acceptable level of debt. The AAOIFI has established guidelines for certain financial ratios to create a universe of halal stocks:

- Conventional debt ÷ total market capitalisation < 30%

- (Cash + interest bearing deposits) ÷ total market capitalisation < 30%

- Accounts receivables ÷ total assets < 45%

- (Total interest + income from non-compliant activities) ÷ revenue < 5%

Shariah-compliant mandates can only invest in common stock–preferred stock covenants with higher-priority payments in the case of bankruptcy. Interest-like fixed dividend payments are considered non-compliant by Shariah scholars. Furthermore, cash must be placed in Shariah-compliant accounts (usually Murabaha deposits).

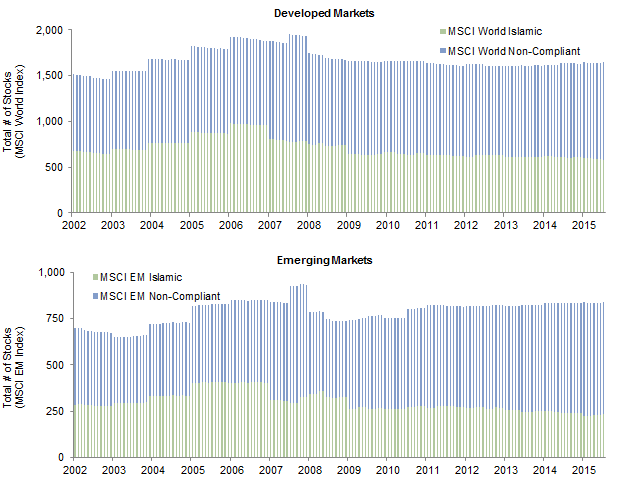

Islamic Indices. As the industry has become more sophisticated, a number of mainstream index providers have created Islamic indices based on the industry and financial ratio screens just discussed. The three most prominent are the Dow Jones Islamic Market Index™ Family, the FTSE Shariah Global Equity Index Series, and the MSCI Global Islamic Indices.

Each index provider has a Shariah board with slightly different rules for compliance. This can cause differences in the size of universe, with Islamic indices ranging from just one-third to over half the size of their respective mainstream counterparts. Figure 3 shows the ratio of Shariah-compliant to non-Shariah-compliant stocks over time for the MSCI World and MSCI Emerging Markets indices. Since inception of the MSCI Islamic indices in May 2002, the MSCI World Islamic and MSCI EM Islamic indices have had average monthly inclusion rates of 42% and 38%, respectively.[1]The MSCI World and EM Islamic indices were launched on Jul 26, 2007. Data prior to the launch date is back-tested data (i.e. calculations of how the index might have performed over that time period … Continue reading

Figure 3. Compliant versus Non-Compliant Stocks

30 June 2002 – 31 December 2015

Sources: FactSet Research Systems and MSCI Inc. MSCI data provided ‘as is’ without any express or implied warranties.

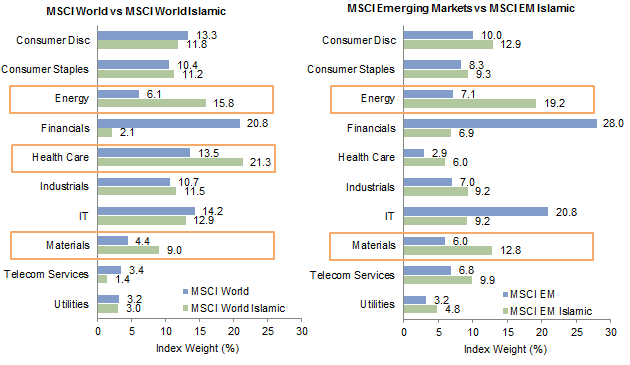

The effects of Islamic screens tend to be similar across providers. The ban on conventional banks and insurance companies almost entirely eliminates the financial sector, which means a large part of that sector’s index weight must be distributed across other sectors. In developed equities (MSCI World Islamic), the big underweight to the financial sector creates heavy overweights in energy, health care, and materials. In emerging markets, the MSCI EM Islamic Index’s financials underweight creates large overweights in energy and materials (Figure 4).

Figure 4. Sector Comparison: Standard Index versus Islamic Index

As at 31 December 2015

Sources: FactSet Research Systems and MSCI Inc. MSCI data provided ‘as is’ without any express or implied warranties.

With market movements, companies may fall into short-term non-compliance based on the financial ratios screen. Index providers (and asset managers) have varying procedures for dealing with this, based on direction from their Shariah scholars. However, most procedures for such situations involve allowing a period of time for the financial statement non-compliance to ‘correct’ itself before having to be reviewed by the Shariah board for potential removal from the index.

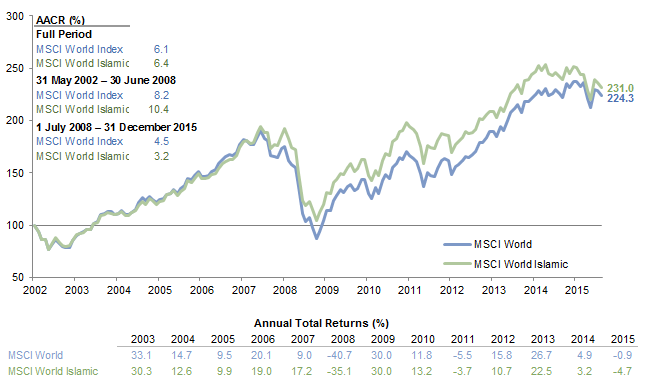

Reaching conclusions about the long-term effects of Shariah restrictions on performance is difficult, largely due to the short track record of Shariah-compliant indices. Since inception of the MSCI World Islamic Index in May 2002, Shariah-compliant equities have outperformed the wider index (6.4% vs 6.1% annualised) with slightly lower volatility (Figure 5). From inception through 30 June 2008, the MSCI World Islamic Index outperformed the mainstream index by 2.2% annualised (10.4% vs 8.2% annualised). This included a one-year outperformance of 8.2 ppts in 2007 (17.2% vs 9.0%). However, in the last 7.5 years through December 2015, Islamic index outperformance has turned to underperformance. Since July 2008, the MSCI World Islamic Index has returned 3.2% annualised compared to 4.5% for the wider index, with the Islamic index significantly lagging over the 2012–15 period.

Figure 5. Cumulative Performance of MSCI World versus MSCI World Islamic

31 May 2002 – 31 December 2015 • Rebased to 100 at 31 May 2002 • USD Terms

Sources: MSCI Inc. and Thomson Reuters Datastream. MSCI data provided ‘as is’ without any express or implied warranties.

Note: Total returns for MSCI developed markets indices are net of dividend taxes.

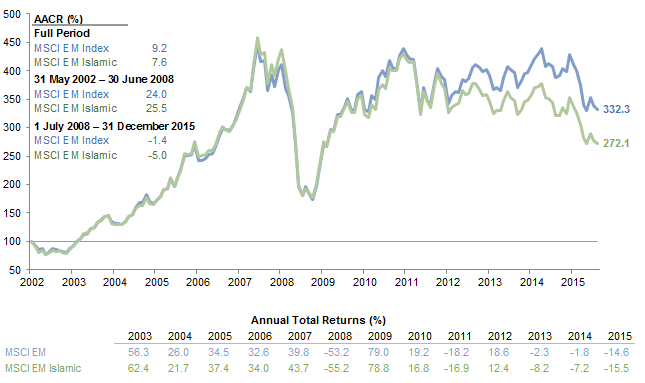

Within emerging markets equities, the MSCI EM Islamic Index has lagged the broader MSCI EM Index by -1.6% annualised (7.6% vs 9.2% annualised) since it incepted in May 2002 with slightly higher volatility (Figure 6). This has been primarily the result of underperformance in the last 7.5 years (through December 2015) where the MSCI EM Islamic Index has returned -5.0% annualised vs the wider index’s return of -1.4% annualised. Similar to developed markets, the MSCI EM Islamic Index has underperformed the broader MSCI EM Index in each of the past four years. However, from inception to June 2008, the EM Islamic Index outperformed by 0.5% annualised (25.5% vs 24.0% annualised).

Figure 6. Cumulative Performance of MSCI Emerging Markets versus MSCI Emerging Markets Islamic

31 May 2002 – 31 December 2015 • Rebased to 100 at 31 May 2002 • USD Terms

Sources: MSCI Inc. and Thomson Reuters Datastream. MSCI data provided ‘as is’ without any express or implied warranties.

Note: Total returns for MSCI emerging markets indices are gross of dividend taxes.

Implementation. In recent years, a growing number of Islamic equity funds have been launched. These funds have varied investment styles and have been created by a variety of players—established conventional investment banks and asset managers as well as local players such as Islamic banks. Further, the existence of investable indices of Shariah-compliant stocks has allowed some managers to launch products without having a Shariah board. Managers simply take the index constituents as their universe and pick from within it. This tends to work best for managers that have a quantitative investment style.

Despite the growing number of funds, the majority of the universe is funds that invest primarily in the GCC or the Asia Pacific region. Furthermore, very few are what Cambridge Associates would consider to be of institutional quality.[2]This is based on a search of Islamic equity funds on the Zawya Thomson Reuters platform.

For investors that prefer to access equities passively, strategies that track various Shariah-compliant equity indices are available. Often these are managed on a separate account basis by more well-known passive managers.

Private Equity and Venture Capital

Private equity funds, particularly venture capital funds, can be well aligned with Islamic principles, again provided that the targets for investment are halal. Target investments in this space must adhere to similar industry and financial ratio guidelines as public equity managers. These include avoiding companies in haram industries as described earlier, as well as those that use high levels of debt. Monitoring Shariah compliance is more challenging with private investments than with public equities because of the illiquid nature of the asset class and infrequency of reporting. Shariah-compliant private investment firms typically need to obtain not just quarterly financial statements from the management of their portfolio companies, but monthly earnings estimates as well. Portfolio companies that fall into non-compliance are typically given 9 to 12 months to return back to compliance; however, any income gained during this period is viewed as non-compliant and must be disposed of.

The most common contract used for private investment strategies is the Musharaka arrangement, as described earlier. Venture capital funds generally do not use debt and tend to make investments in more entrepreneurial sectors, making Shariah compliance more likely from a debt perspective. In contrast, private equity funds have traditionally used high levels of debt, particularly in the early years of investment. Leveraged buyout strategies, where a company is bought through a combination of equity and debt, are a particular challenge. To be Shariah compliant, the private equity fund would have to issue debt through an Islamic contract, such as a Murabaha facility or Sukuk financing. Furthermore, tax and legal considerations of the operating jurisdiction must be taken into account. All of these challenges can create a highly complex structure with significant cost inefficiency.

That said, the haircut one must accept when using Shariah-compliant debt has reduced significantly in recent years. In the past, a Shariah-compliant bank loan cost anywhere in the range of 80 bps to 200 bps over a conventional loan. Global banks have increased the competitive pricing of such structures, and both global and local banks have made marked improvements on their balance sheets and debt ratings, narrowing the spread on Shariah-compliant loans. Today, Shariah-compliant bank loans are not expected to be any higher than 50 bps to 100 bps over a conventional offering.

Implementation. The Islamic private equity space has grown in recent years, mainly in the growth equity portion of the asset class versus leveraged buyouts for the reasons discussed. Sectors that are a better fit for Shariah-based investing include business lines such as infrastructure and industrials, where leverage is not typically an issue.

Implementation can be directed through two main routes. The first is a conventional fund with an arrangement for the limited partner to only be invested in deals that the Shariah board determines as compliant. A typical diversified fund will only have about 10% to 15% of deals eligible for investment. The other option is to invest with Shariah-compliant private investment firms, although the universe of managers in this space tends to be more GCC and ASEAN focused, as well as of lower institutional quality. In either case, a Shariah-compliant private equity program will have to accept a concentrated and less diversified portfolio than that of a conventional program.

Sukuk

Sukuk are often referred to as the Islamic equivalent of bonds. As interest payments are forbidden under Shariah law, the issuer of the Sukuk will use a different structure (typically a rental lease or profit sharing agreement) to avoid the payment of interest while still providing a fixed income stream.

The philosophy and structure of Sukuk have been in place since the early 1990s, with the first modern Sukuk issued in Malaysia in 2001. Variations on the original Sukuk structure were pioneered by issuers from the GCC region, responding to the general need for the Islamic finance industry to raise capital on a long-term basis. Sukuk provide access to the efficiency and transparency of the capital markets while maintaining compliance with Shariah law.

Market Characteristics and Outlook. The global Sukuk market saw cumulative issuance amounts reach $700 billion in 2014 according to the International Monetary Fund. By region, Southeast Asia dominates the primary Sukuk market at 68% of total value of Sukuk issued. That said, GCC investors have traditionally avoided investment in Southeast Asian securities for a number of reasons: (1) as noted, these tend to be denominated in local currency (Malaysian ringgit) and are rated by local rather than internationally recognised agencies; (2) Middle Eastern investors display a marked preference for locally sourced deals; and (3) past issues surrounding the Southeast Asian Sukuk format and correct interpretation of Islamic law.

Based on data from the International Islamic Financial Market, Middle Eastern Sukuk constitute almost 30% of issuance volume, with Saudi Arabia and the United Arab Emirates the largest markets in the region. By issuer type, sovereign paper accounted for 48% of total value, followed by corporates (34%). The market for global hard currency Sukuk is expected to grow significantly, with increasing international interest in the region and support from the GCC, where new sovereign issues are predominantly in US dollars to which their currencies are pegged. Sovereign Sukuk have also been issued by Egypt and Turkey, with potential new supply from Tunisia and non-traditional Shariah issuers, led by the United Kingdom. As a result, the global market is becoming increasingly geographically diversified, although the GCC remains the predominant region with 55% of the market (as measured by the Dow Jones Sukuk Index).

Rating agencies are active in the global (hard currency) Sukuk market and typically get involved early in the process. The credit rating will determine the terms of the agreement that defines the structure of the Sukuk and the relationship established between the parties involved. Occasionally, hard currency issuances have been unrated, but this is a very small part of the market as issuers see the rating of the Sukuk as fundamental to the structure. The timing and cost of the process have dramatically improved over the last several years, with the ratings now typically taking seven to ten days, visibly boosting new issuance in recent years.

With these positive developments, Sukuk have performed well and yields on the market have declined both in absolute terms and compared to conventional bond markets. Despite significant growth in new issues and issuers in recent times, supply and demand remain imbalanced in favour of issuers. New issues are routinely heavily oversubscribed, making it difficult for large investors to establish mandates without having to gradually scale up their position over a period of six or more months.

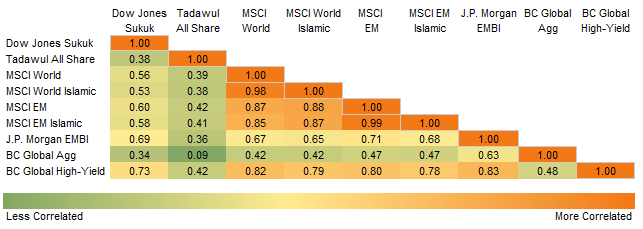

Where Do Sukuk Fit in the Portfolio? Diversified holdings of Sukuk can reduce volatility and add value to an equity-heavy, Shariah-compliant portfolio. While reducing volatility within the portfolio, Sukuk show a historically low correlation with conventional asset classes such as global equities as well as developed government bond indices, but show a higher correlation to high-yield bonds and emerging markets debt (Figure 7).

Figure 7. Correlation Between Sukuk and Conventional Asset Classes

31 October 2005 – 31 December 2015 • Based on Index Returns in USD Terms

Sources: Barclays, Dow Jones Indexes, J.P. Morgan Securities, Inc., MSCI Inc., Saudi Stock Exchange (Tadawul), and Standard & Poor’s. MSCI data provided ‘as is’ without any express or implied warranties.

Notes: Calculations are based on monthly data. Data are total returns with the exception of the Tadawul All Share Index, which are price returns. Total returns for MSCI developed markets indexes are net of dividend taxes. Total returns for MSCI emerging markets indexes are gross of dividend taxes.

Sukuk have also traditionally had a low yield, albeit comfortably higher than that offered by Murabaha contracts, which had for a long time been considered the only fixed income option for Shariah-compliant investors. As at 31 December 2015, the yield on the DJ Sukuk Index had moved up to 3.24%, the highest value in several years (it has since moved back under 3%). This was higher than for conventional government bonds (1.16% for the Citigroup World Government Bond Index), and even just above traditional investment-grade credit.[3]At the end of 2015, Dow Jones Global Sukuk Index had a 50% exposure to sovereign issues and 50% exposure to corporate Sukuk.

On balance, Sukuk’s characteristics are more similar to those of “diversifying investments” (i.e., investment-grade credit or high-yield bonds) than sovereign bonds; they can be expected to produce moderate returns but with relatively low volatility and a differentiated return profile to equities. Volatility has been reduced by lower default rates in the years since 2009, brought about through institutional investors’ increasing participation in the market, as they demand that issuers adhere to more stringent processes for structuring Sukuk and determining the Shariah compliance of coupons.

We would caution against viewing Sukuk as a deflation hedge. Conventional investors use the highest-grade sovereign bonds as a deflation hedge because these assets are expected to maintain a stable value or appreciate in deflationary conditions while providing a liquid pool from which to meet spending requirements or capital calls. Although sovereign states are among the most prominent issuers of Sukuk, these only account for around 20% of the total market at present. This figure admittedly masks that a significant portion of other issuers that are also government-related entities and/or companies active in heavily regulated industries such as utilities. However, even accounting for this, we believe the substantial corporate exposure within the broad market—and most global Sukuk fund offerings—means the asset class will not serve as a reliable hedge against deflation.

The global Sukuk market is evolving rapidly, and although finding sovereign-backed Sukuk remains a challenge today, sovereign issuance is likely to grow over time (16 governments have issued sovereign Sukuk to date and a number of developed and emerging countries have expressed an interest in following suit). As this occurs, the option of establishing sovereign-only Sukuk mandates—to serve as a deflation hedge rather than as a diversifying allocation—will become more viable.

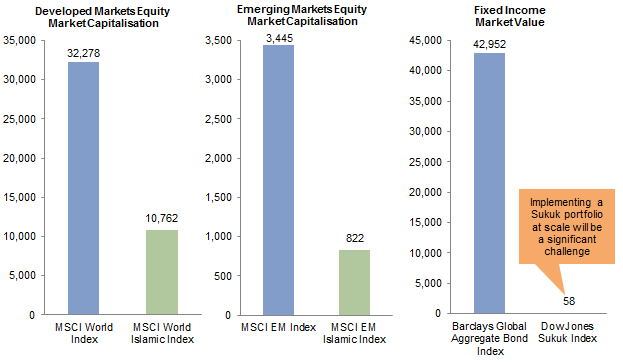

Implementation. Along with public equities, the Sukuk universe is the most developed in the Shariah-compliant space. That said, compared with conventional fixed income, the Sukuk market remains small (Figure 8), limiting its implementation scalability. At present, investors can only access the Sukuk market through active management, as the market remains small and access-constrained. Active managers can use their networks to gain access to heavily subscribed issuances and can invest off-benchmark to generate returns for their clients. Furthermore, it is not uncommon for investors to seek geographic, credit rating, and issuer-type exposures different from those of the available indices, making actively managed mandates a necessity. The Sukuk manager universe continues to grow, with more institutional-quality managers entering the market.

Figure 8. Comparison of Size of Conventional and Islamic Opportunity Sets by Asset Class

As at 31 December 2015 • US Dollar (billions)

Sources: Barclays, Dow Jones Indexes, MSCI Inc., Standard & Poor’s, and Thomson Reuters Datastream. MSCI data provided ‘as is’ without any express or implied warranties.

From the perspective of benchmarking, the Dow Jones Sukuk Index is the most widely used representation of the global (i.e., US dollar denominated) Sukuk market. The index consists of 60–70 USD-denominated, investment-grade Sukuk with a minimum of one-year maturity and $200 million issue size. At the middle of 2015, the index’s geographic exposure was 55% to the GCC countries and 25% to Asia, with the remainder made up of supranational issuers and Turkey, South Africa, and the United States. Alternatives to the DJ Sukuk Index are few, with the Thomson Reuters Global Sukuk Index perhaps the most notable.

Commodities

Commodities fall into two categories: hard commodities that are mined or extracted (metals, coal, oil, etc.) and soft commodities that are grown (corn, soya, livestock, etc.). Given the practicalities of transporting and storing commodities in any significant quantity, most investors gain exposure to commodities through products that track commodity futures indices, as futures contracts eliminate the complications of investing in physical commodities. The return comes from three sources: the change in the underlying spot price, the interest on the collateral, and the roll yield (which is related to supply and demand for the futures contracts).

Shariah-compliant commodity investing faces two separate issues: the compliance of the underlying assets, and the structure of the financial instruments used in implementing the investment. In terms of the underlying assets, certain commodities are universally accepted as haram: for example, hogs, which as at 31 December 2015 accounted for 1.8% of the Bloomberg Commodity Index and 2.2% of the S&P GSCI™. Some scholars also dispute the compliance of precious metals (specifically gold) given they can be used as currency and their value is wholly dependent on subjective assessment.[4]See, for example, Muhammad Ayub, Understanding Islamic Finance (Hoboken, NJ: John Wiley & Sons, Ltd., 2007), p. 244. In terms of structure, large Islamic banks have the resources to invest directly in commodities, without the need for derivative contracts: they can buy and sell commodities using Murabaha contracts. However, this option is not suitable for smaller asset managers.

Certain Islamic structures that are similar to forward contracts could facilitate an approximation of a conventional commodity fund. However, in practice, these structures are rarely used and prohibitively expensive. Active commodity managers that use futures contracts could, in theory, create a Shariah-compliant product very similar to their conventional offerings, but the practicalities of gaining and maintaining the approval of a Shariah board is often the primary obstacle to launching a Shariah-compliant fund. A leading commodity manager we spoke with explained that a Shariah-compliant version of its flagship commodity fund could be created with only minor adjustments to the strategy, but the costs of implementing it would have outweighed the interest they had from their clients, so they stopped pursuing it. We believe the high cost of implementation will continue to be an obstacle, unless managers see a very large uptick in demand.

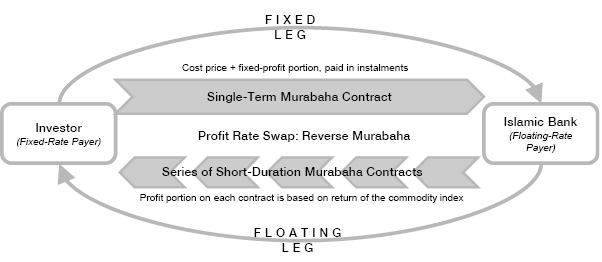

Implementation. Given that direct investments and commodity futures–like funds are not practical options today, for investors seeking exposure to commodities, the logical alternative to active commodity management is the tracking of an index through a passive fund. Indices that screen out non-Shariah compliant industries are available, such as Bloomberg Commodity Modified ex Hogs Total Return Index; however, these indices are based on conventional derivatives. To avoid these non-Islamic financial structures, some investors enter into a contract similar to a swap (conventional commodity exchange- traded funds sometimes use swaps to replicate index performance). Using Islamic principles, a contract can be structured to replicate the cash flows of a conventional swap, although based on a physical principal rather than a notional one.[5]A Wa’ad swap is the promise agreement with which returns from one long-term Murabaha contract are swapped with returns from a series of short-term Murabaha contracts, the maturity of which matches … Continue reading In exchange for paying a long-term, fixed-rate Murabaha, the investor would receive a series of reverse-Murabaha payments based on the returns of a chosen commodity index. Since this series of Murabaha have short maturities and the profit rate is based on the commodity index return at each maturity date, the cash flow is essentially based on a floating rate (Figure 9).

Figure 9. Conceptualizing a Murabaha Islamic Swap

Such an arrangement would have to be made through a major investment banking house and requires the approval of a Shariah board, each introducing its own additional costs. However, for investors that desire commodity exposure, this would be one of the most efficient methods of replicating conventional (non-Shariah) commodity performance within a Shariah portfolio.

An alternative method is to invest in funds physically backed by the commodities. A few mutual and exchange-traded commodity (ETC) funds buy the assets they are designed to track and store them with approved custodians in warehouses; commodity exposure through these products is limited to precious or industrial metals that can be stored for long periods without corruption and that are fungible. Securities in these funds are generally structured as debt securities rather than equity: upon purchase, the investor obtains an allocated physical entitlement to the underlying asset without the use of derivatives. The price of an ETC is determined by the spot price of the asset multiplied by the metal entitlement. Since the bullion is allocated it cannot be used for lending and there is no counterparty or credit risk.

Natural Resources Equities

Today, natural resources equities (investment in companies connected to commodities, e.g., oil companies) offer commodity exposure with fewer implementation headwinds than commodity futures markets. However, natural resources equities have historically been more highly correlated with broad equities than with commodity prices, since they do not require appreciation in the underlying commodity to see an upside in performance: returns are driven by the share price, meaning that market sentiment and corporate management are just as influential as commodity prices.

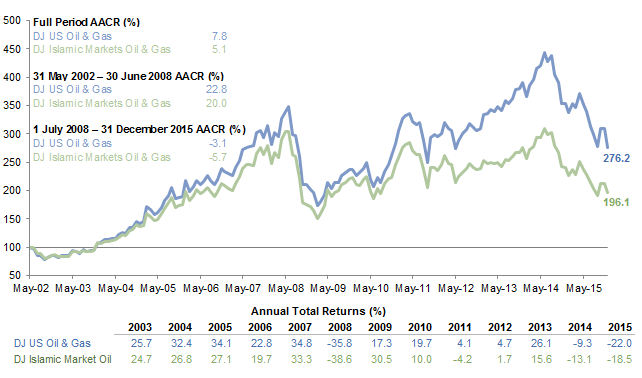

Shariah compliance for these funds can be achieved in the same way as for broad-market equity funds (described earlier). Shariah indices exist, such as the Dow Jones Islamic Market Oil & Gas Index, which screens companies based on similar characteristics as those previously described for equity funds.[6]According to S&P Dow Jones Indices LLC: Companies must meet Shariah requirements for acceptable products, business activities, debt levels, and interest income and expenses. The screening … Continue reading Figure 10 compares the returns of the Dow Jones Oil & Gas Index against its Shariah-compliant counterpart.

Figure 10. Cumulative Performance of DJ US Oil & Gas versus DJ Islamic Market Oil & Gas

31 May 2002 – 31 December 2015 • Rebased to 100 at 31 May 2002 • USD Terms

Sources: Dow Jones Indexes, Standard & Poor’s, and Thomson Reuters Datastream.

Note: Total returns are shown gross of dividend taxes.

Shariah-screening results in a universe of compliant stocks from which investment managers can build portfolios. The screening process can alter the composition of the index; for example, a Shariah-compliant broad natural resources index would likely have a much smaller allocation to gold mining companies, as these typically rely on levels of debt that exceed the screen’s threshold for financial viability. In recent years this has been beneficial to Shariah-compliant investors, as gold mining stocks have been through a three-year period of significant underperformance. While the compliance of livestock assets is a consideration for commodity-futures indices, in listed equity indices, the agriculture sector is dominated by fertilizer and seed companies.

Implementation. Actively managed natural resources equity strategies use fundamental research to pick stocks from the Shariah-compliant universe in which to invest; they may also have the option to invest in off-benchmark positions subject to approval by a Shariah board. Both actively managed and passive funds are few and far between in this space, particularly managers of institutional quality.

Private Real Estate (Closed Ended)

Real estate investment managers typically employ leverage when making their investments, which is of course banned under Islamic law. Consequently, any leverage used within a Shariah-compliant fund must be structured by an Islamic investment bank. The Mudaraba structure is the most common amongst Shariah real estate funds: this is similar to a limited partnership in that the investor (rab al-maal) gives money to the manager (mudarib) which manages the capital based on its expertise, with the investor having no involvement with the management of assets. However, certain standard fund provisions must still be adapted to ensure compliance; for example, investors cannot be charged interest for late payment of commitments.[7]See Nabarro LLP, ‘Shariah Compliant Real Estate Funds: An Introduction,’ London, June 2011.

The manager also has to take into account the Islamic credentials of its tenants. Office and industrial real estate are favoured by Shariah property managers over hotels and retail assets that may be exposed to haram products (e.g., alcohol). A small exposure (typically <10%) to haram assets can sometimes be tolerated, with the provision that any income generated from haram products be ‘purified’ (most often donated to charity).

Implementation. A small universe of Shariah real estate funds is available to institutional investors, primarily offered by asset managers based in the GCC or Singapore, where local demand is highest. The funds tend to have a regional focus, with Asia and the Middle East being the most common followed by the United Kingdom. The nature of the fund-raising process means that, at any given time, there is limited choice, limiting diversification potential.

Another option popular with smaller investors is syndication, whereby a group of investors pools their resources to invest in a single real estate project. The syndication is usually arranged by an Islamic bank that acts as the mudarib. This differs from a pooled fund in two key ways. First, investment in a pooled fund is ‘passive’ in that the investor does not identify the assets, and the decision to invest is driven by an assessment of the portfolio managers’ skill, whereas in a syndicated transaction the decision to invest is more often based on the choice of asset. Second, a syndicated transaction is project based, where all investment risk is concentrated in one asset; in a pooled vehicle the risk is diversified as the manager will spread the capital over several transactions.

Listed Real Estate

For investors with too little capital to build a diversified private real estate programme, real estate securities can be an imperfect alternative. Real estate investment trusts (REITs) are publicly traded securities of companies whose underlying assets are real property or whose operations are closely tied to the real estate industry. As these are equities, they are far more liquid than private real estate, but subsequently they may be vulnerable to non–real estate influences: for example, interest rate increases due to inherent leverage and low tolerance by investors for situations where yields fall below fixed income yields. This makes REITs highly volatile.

Implementation. A handful of Shariah-compliant REITs are available; the first Islamic REIT was listed in Malaysia in 2006 and four Shariah REITs are currently listed on the Malaysian stock exchange. At the end of 2014, Singapore boasted one of the largest listed Islamic REITs in the world—Sabana REIT at $680 million market capitalisation. The first Emirates REIT was launched in 2010 but only publicly listed in April 2014. Shariah REITs tend to focus investment on industrial, office, or health care assets, as these sectors are the least likely to derive revenue from haram sources. These sectors have historically been seen as ‘safe havens’ as they provide sustainable yield; so while they have enjoyed strong performance in recent years, future performance may suffer from current high valuations.

Sovereign Bonds and Cash

Within the context of conventional investment portfolios, investors hold sovereign bonds for a variety of reasons, including as a liquidity reserve, ase of steady income, to reduce the volatility of their equity portfolios, or to offer some diversification away from equity risk. Sovereign bonds also serve a ‘deflation hedging’ role as they offer the best protection against economic and equity price deflation. To serve as a reliable deflation hedge, these bonds must have very low credit risk (sovereign, not corporate issuance), be non-callable long-term bonds, and be owned in an amount sufficient to limit declines in capital values of the total portfolio. A decline in interest rates during such a period should produce sizeable capital gains in the bond portfolio, offsetting falling asset values elsewhere.

Shariah-compliant investors cannot build traditional deflation hedging allocations in their portfolios because of the prohibition of riba, and because a large proportion of Sukuk—which in some senses can be described as a Shariah-compliant form of bond—are issued by non-sovereign entities, which introduces excessive credit risk as already discussed.[8]As a result of the current makeup of the market, most global Sukuk funds invest in both sovereign and corporate issues at present, making them inappropriate for a deflating-hedging allocation. If the … Continue reading As a result, high-quality Shariah-compliant cash and money market strategies are the most viable, though imperfect, means of building a deflation-hedging allocation.

Most cash securities are structured as Murabaha contracts. Under this type of contract, a lender provides the commodity (in this case the commodity is cash), which it owns, and sells this to the client on credit. When agreeing on the terms of the contract, the lender takes into account the length of time over which the price is to be paid by the client and increases the mark-up component of the price accordingly; the longer the maturity of the Murabaha payment, the higher the mark-up charged. To avoid riba and ensure Shariah compliance, in Murabaha involving cash—rather than an economically useful commodity with an intrinsic value—the only basis for claiming an excess on the par value of underlying cash transaction is time. The exact timing and value of repayment must be explicitly agreed upon at the outset of the arrangement.

Although Murabaha deposits are the pre-eminent form of cash security, their use as a mode of financing has faced criticism from some Islamic scholars. The structure is technically a type of sale rather than a mode of financing, which has been used as a device to avoid riba in instances where alternative contract types are impractical. Mudaraba (profit sharing arrangements) and Musharaka (joint ventures) contracts are preferred where practical difficulties do not preclude their use. Wakala, a structure that has similarities to Mudaraba—but with both risk and profits shared by both parties in the arrangement—has seen increasing popularity with industry purists in the last few years.

Implementation. Several institutional funds are available within the cash and money markets space, but the vast majority of Shariah-compliant investors access these securities via accounts with GCC banks. The benefit of the latter is that these accounts can be customised to the investor’s needs, meaning that specific contract types, issuers, and maturity profiles can be emphasised. However, GCC banks often have retail-oriented customer bases, which may mean that their platforms are sub-optimal for larger institutional investors.

Hedge Funds

The term ‘hedge fund’ refers to a broad range of strategies that tend to use some degree of shorting/hedging and may use leverage and derivatives. The vast majority of derivatives such as futures, forwards, swaps, convertibles, etc. are deemed non–Shariah compliant as they involve an unacceptable level of gharar (speculation). This eliminates the viability of many traditional hedge fund strategies—including event arbitrage, merger arbitrage, and credit distressed securities—for Islamic investors.

Conventional short selling is also currently prohibited as (1) the vehicles borrow securities to undertake short selling (under Shariah, one cannot sell what one does not own) and (2) interest is paid in the borrowing of the security. Some scholars have begun to accept in principle the idea of short selling as a form of acceptably managing risk, as long as there is assurance that the asset will be delivered, eliminating gharar. However, we have not seen compelling, institutional-quality, Shariah-compliant hedge funds emerge, though we continue to monitor activity in this space.

Putting It All Together: Building the Portfolio

Our review of the options for Islamic investors shows that a Shariah-compliant portfolio can be constructed, although practical limitations must be acknowledged. To build a viable policy asset allocation for a large institutional Islamic investor ($500 million or more), we have considered the information presented in this report and the actual opportunities available to investors, as summarised in Figure 11.

Figure 11. Shariah Compliance and Its Effect on Portfolio Diversification

As we have discussed, while almost every asset class can, in theory, become Shariah compliant, in practice a Shariah-compliant policy portfolio today cannot include them all. In private equity, for example, few top-quality global managers are willing to use Shariah-compliant debt financing to fund their investment activities. Similarly, in Sukuk, the limited available market of hard currency Sukuk makes it very challenging for a large investor to gain sufficient scale in the asset class.

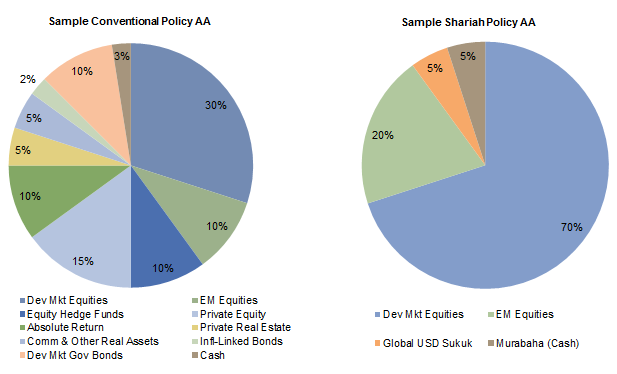

With these considerations in mind, a policy allocation for an Islamic investor might be as follows:

- Developed markets equity: 70%

- Emerging markets equity: 20%

- Global Sukuk: 5%

- Murabaha/cash: 5%

Using the available representative indices for each category, we show the risk/return profile of a portfolio with this allocation from July 2007 to September 2015 (Figure 12) as well as that of a conventional portfolio based on the mean asset allocation of institutional clients with assets over $1 billion in the Cambridge Associates database (Figure 13). This is a limited time period due to the short history of the available indices. As shown in Figure 12, the sample conventional portfolio outperformed the sample Shariah-compliant portfolio by 1.5 ppts annualised (3.1% versus 1.6% average annual compound return) over this period with almost one-third less volatility (standard deviation of 12.6% versus 17.9%). This resulted in a higher Sharpe ratio of 0.26 for the sample conventional portfolio compared to the sample Shariah-compliant portfolio (0.14). As expected, the sample Shariah-compliant portfolio had a much higher beta to global equities (0.88) when compared to its sample conventional counterpart (0.62).

Figure 12. Risk/Return Analysis for Sample Conventional and Shariah-Compliant Portfolios

1 July 2007 – 30 September 2015 • USD Terms

Sources: Barclays, Bloomberg L.P., Cambridge Associates LLC, Citigroup Global Markets, Credit Suisse, Federal Reserve, MSCI Inc., and Thomson Reuters Datastream. MSCI data provided ‘as is’ without any express or implied warranties.

Notes: The Conventional Policy is based on the average asset allocation as at 30 September 2015 of 84 institutions with assets greater than $1 billion in the Cambridge Associates peer database. Relevant benchmarks were used to proxy returns over time for this asset allocation. The Sample Shariah Policy uses relevant benchmarks to proxy a return for an asset allocation of 70% developed markets equities, 20% emerging markets equities, 5% global Sukuk, and 5% Murabaha (cash). All data are quarterly and based on total returns. Total returns for MSCI developed markets indices are net of dividend taxes. Total returns for MSCI all country and emerging markets indices are gross of dividend taxes.

* The Sharpe Ratio represents the excess return generated for each unit of risk. To calculate this number, subtract the average T-Bill return (risk-free return) from the average return, then divide by the standard deviation.

Figure 13. Composition of Sample Conventional and Shariah-Compliant Portfolios

Note: The Conventional Policy is based on the average asset allocation as at 30 September 2015 of 84 institutions with assets greater than $1 billion in the Cambridge Associates peer database. In Figures 12 and 14, the benchmarks used to proxy returns fo reach asset class in this sample allocation are as follows: MSCI World Index (Dev Mkt Equities), MSCI Emerging Markets Index (EM Equities), Credit Suisse Long/Short Equity Index (Equity Hedge Funds), Cambridge Assocaites Private Equity Index(Private Equity), Credit Suisse Multi-Strategy Index (Absolute Return), Cambridge Associates Private Real Estate Index (Private Real Estate), Bloomberg Commodity Index (Comm & Other Real Assets), Barclays Global Inflation-Linked Index (Infl-Linked Bonds), Citigroup World Government Bond Index (Dev Mkt Gov Bonds), and Cash (Cash).

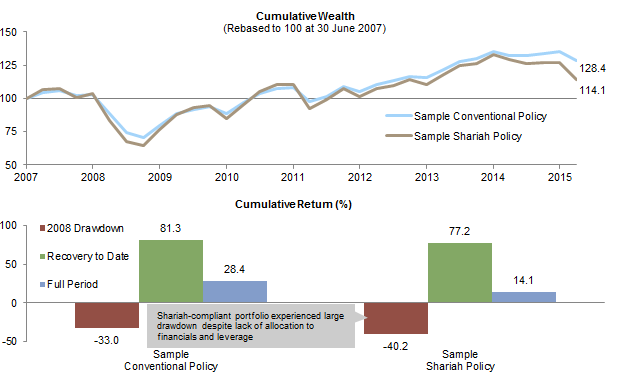

We also conducted a stress test of this sample Shariah-compliant portfolio to measure the effectiveness of the portfolio in providing downside protection in a drawdown event like 2008. Despite the lack of allocation to financials, as well as no use of leverage in the portfolio, the sample Shariah-compliant portfolio still underperforms its sample conventional counterpart in a stress scenario (Figure 14), owing to the overall lack of diversification in the portfolio, and in particular, the lack of true diversifiers in a Shariah-compliant portfolio.

Figure 14. Historical Performance Analysis of Sample Conventional and Shariah-Compliant Portfolios

Second Quarter 2007 – Third Quarter 2015 • USD Terms

Sources: Barclays, Bloomberg L.P., Cambridge Associates LLC, Citigroup Global Markets, Credit Suisse, Federal Reserve, MSCI Inc., Standard & Poor’s, and Thomson Reuters Datastream. MSCI data provided ‘as is’ without any express or implied warranties.

Notes: The Conventional Policy is based on the average asset allocation as at 30 September 2015 of 84 institutions with assets greater than $1 billion in the Cambridge Associates peer database. Relevant benchmarks were used to proxy returns over time for this asset allocation. The Sample Shariah Policy uses relevant benchmarks to proxy a return for an asset allocation of 70% developed markets equities, 20% emerging markets equities, 5% global Sukuk, and 5% Murabaha (cash). All data are quarterly and based on total returns. Total returns for MSCI developed markets indices are net of dividend taxes. Total returns for MSCI all country and emerging markets indices are gross of dividend taxes. Periods are represented by the following: ‘2008 Drawdown’, third quarter 2008 through third quarter 2009; ‘Recovery to Date’, second quarter 2009 through third quarter 2015; and ‘Full Period’, second quarter 2007 through third quarter 2015.

This analysis gives investors seeking to build a Shariah-compliant portfolio a sense of how they could structure a long-term investment portfolio and the implied returns and volatility they might expect to encounter relative to conventional investors.

Conclusion

As we have discussed, the options for Islamic investors are evolving and the landscape will continue to change in the years ahead. More institutional-quality, actively managed funds are becoming available, which could materially change the experience of Shariah-compliant portfolios relative to the index-based sample portfolio we have shown. Islamic investors seeking to build a Shariah-compliant portfolio have more opportunities than ever before, and we will be closely watching this landscape as it evolves.

Cambridge Associates does not provide stock selection recommendations, and any reference to specific companies is not to be interpreted as a

recommendation of that company as an investment option.

Index Disclosures

Broad-based securities indices are unmanaged and are not subject to fees and expenses typically associated with managed accounts or investment funds. Investments cannot be made directly in an index. Past performance is no guarantee of future results.

Barclays Global Aggregate Index

The Barclays Global Aggregate is an index consisting of over 5,000 government, corporate, asset-backed, and mortgage-backed securities.

Barclays Global High Yield Index

The Barclays Global High Yield Index represents the US High Yield Index, Pan-European High Yield Index, High Yield CMBS Index, and non-investment grade portion of the Barclays Global Emerging Markets Index.

Barclays Global Inflation-Linked Index

The Barclays Global Inflation-Linked Index represents bonds with cash flows linked to an inflation index. Countries covered include the United States, United Kingdom, Canada, Sweden, Italy, Germany, Greece, France, and Japan. All bonds must be sovereign issues, have greater than one year-to-maturity, and be denominated in the relevant native currency.

Bloomberg Commodity Index

The Bloomberg Commodity Index is made up of 22 exchange-traded futures on physical commodities. The index currently represents 20 commodities, which are weighted to account for economic significance and market liquidity. Weighting restrictions on individual commodities and commodity groups promote diversification.

Cambridge Associates Private Equity Index

The Cambridge Associates Private Equity Index is based on data compiled from 1,647 private equity funds including fully liquidated partnerships, formed between 1986 and 2015.

Cambridge Associates Private Real Estate Index

The Cambridge Associates Private Real Estate Index is based on data compiled from 847 real estate funds, (including opportunistic and value-added real estate funds) including fully liquidated partnerships, formed between 1986 and 2015.

Citigroup World Government Bond Index

The Citigroup World Government Bond Index is composed of issues of the government markets of the United States, Japan, Germany, France, the United Kingdom, Canada, Italy, Australia, Belgium, Denmark, the Netherlands, Spain, Sweden, and Austria, and measures total return performance for government bond markets with a remaining maturity of at least one year.

Credit Suisse Long/Short Equity Index

The Credit Suisse Long/Short Equity Hedge Fund Index measures the aggregate performance of dedicated short bias funds. Long/short equity funds typically invest in both long and short sides of equity markets, generally focusing on diversifying or hedging across particular sectors, regions,or market capitalisations. It is a subset of the Credit Suisse Hedge Fund Index.

Credit Suisse Multi-Strategy Index

The Credit Suisse Multi-Strategy Hedge Fund Index measures the aggregate performance of dedicated short bias funds. Strategies adopted in a multi-strategy fund may include, but are not limited to, convertible bond arbitrage, equity long/short, statistical arbitrage and merger arbitrage. It is a subset of the Credit Suisse Hedge Fund Index.

Dow Jones Islamic Market Oil & Gas Index

The Dow Jones Islamic Market Oil & Gas Index is a sector index within the Dow Jones Islamic Market family. To be included in the Islamic Market family, stocks are screened to ensure compliance with Shariah requirements, including a review of business activities, debt levels, and interest income and expenses.

Dow Jones Sukuk Index

The Dow Jones Sukuk Index is designed to measure the performance of global Sukuk (Islamic fixed income securities). To be included in the index, a bond must pass screens for Shariah compliance and meeting the standards issued by the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI), have a minimum maturity of one year, a minimum size outstanding of USD 200 million, and an explicit or implicit rating of at least BBB-/Baa3 by leading ratings agencies. The index is US dollar denominated.

FTSE Shariah Global Equity Index Series

The FTSE Shariah Global Equity Index Series is designed to measure performance of large- and mid-cap stocks included in the FTSE Global Equity Index Series universe, screened for Shariah compliance. The initial screen reviews business activities, and remaining companies are subject to a screen for financial ratios.

J.P. Morgan EMBI Global Index

The J.P. Morgan EMBI Global Index is an unmanaged index that tracks total returns for dollar-denominated Brady bonds, Eurobonds, traded loans, and local market debt-instrument issues by sovereign and quasi-sovereign entities of emerging markets countries.

MSCI Emerging Markets Index

The MSCI Emerging Markets Index represents a free float–adjusted market capitalisation index that is designed to measure equity market performance of emerging markets. As at February 2013, the MSCI Emerging Markets Index includes 23 emerging markets country indexes: Argentina, Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, India, Indonesia, Israel, Korea, Malaysia, Mexico, Morocco, Peru, Philippines, Poland, Russia, South Africa, Taiwan, Thailand, and Turkey.

MSCI Emerging Markets Islamic Index

The MSCI Emerging Markets Index reflects Shariah investment principles by applying stringent screens to exclude securities based on business activities and financial ratios. The index is designed to measure the performance of large- and mid-cap segments in the 23 emerging markets countries that are relevant to Islamic investors and has 230 constituents.

MSCI World Index

The MSCI World Index represents a free float–adjusted, market capitalisation–weighted index that is designed to measure the equity market performance of developed markets. As at February 2013, it includes 24 developed market country indices: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Greece, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the United Kingdom, and the United States.

MSCI World Islamic Index

The MSCI World Islamic Index reflects Shariah investment principles by applying stringent screens to exclude securities based on business activities and financial ratios. The index is designed to measure the performance of large- and mid-cap segments in the 21 developed markets countries that are relevant to Islamic investors and has 573 constituents.

Tadawul All Share Index

The Tadawul All Share Index represents a free-float adjusted index designed to measure the market performance of the 169 publicly traded companies on Saudi Arabia’s Tadawul stock exchange.

Shahnawaz Nawabi, Investment Director

Joseph Goddard, Associate Investment Director

Riazul Raquib, Associate Investment Director

Footnotes