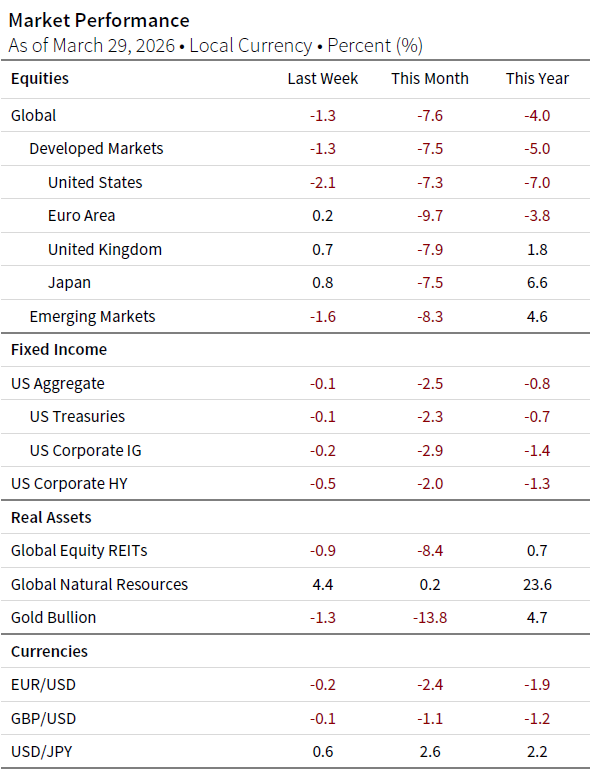

Global equities fell for a fourth consecutive week amid rising expectations for a more extended Iran War, higher commodity prices, and renewed near-term inflation concerns. Performance dispersion across equity markets was significant, with more defensive and commodity-sensitive segments outperforming growth-oriented areas.

- Markets were volatile as investors weighed the risk of further escalation in the Middle East against periodic signs of diplomatic restraint. The result was a market increasingly focused on the likelihood that the conflict could prove more prolonged and economically disruptive than previously assumed.

- Within equities, the US market, which had been outperforming since the start of the Iran War, lagged last week as mega-cap tech and other growth stocks underperformed. Utilities, energy, and materials led at the sector level, reflecting a combination of defensive positioning and renewed inflation concern.

- Investor concerns broadened beyond energy into secondary channels, most notably agriculture, and logistics. This raised fears of a wider input-cost shock that could create more significant and persistent inflation pressure. WTI ended the week near $100 a barrel and Brent rose above $110.

- Developed markets composite PMIs for March pointed to slowing, but still expanding, economic activity. Manufacturing generally surpassed consensus expectations, while services disappointed.

Sources: Bloomberg Index Services Limited, MSCI Inc., and Thomson Reuters Datastream. MSCI data provided “as is” without any express or implied warranties.

Notes: This edition was prepared on March 29, 2026, and it reviews developments of the prior month. The equity data are total returns net of dividend taxes of MSCI indexes in local currency. Global natural resources equities are represented by the MSCI All Country World Commodity Producers Index. The fixed income data are total returns for Bloomberg indexes. Gold Bullion uses near-month gold futures contracts, as traded on the COMEX, to determine performance. Currency performance is based on Reuters data.