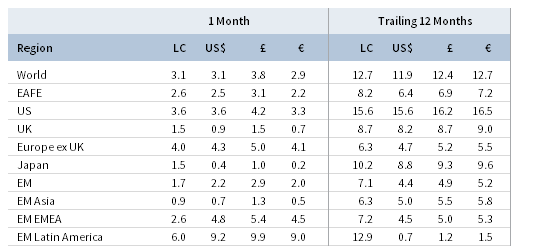

Equities led the resurgence in risk assets last month, as US/EU trade tensions abated for now and robust global corporate results continued to reflect healthy underlying fundamentals. Global equities gained across the board, led by Europe ex UK and the United States as developed markets outperformed emerging markets, which bounced back from a weak second quarter. Value stocks outperformed growth counterparts, highlighted by strong performance from the financials and industrials sectors, and large caps outgained small caps—both counter to recent trends. Global government bonds were generally weaker in July as global yields rose and curves flattened, but corporate bonds gained as credit spreads tightened. Natural resources equities advanced despite weak underlying commodity prices, and developed REITs continued to rebound from losses earlier in the year. Among currencies, the US dollar and UK sterling generally weakened, while euro performance was mixed.

Global economic growth indicators continued to moderate in July amid signs that ongoing trade tensions may be starting to dampen business sentiment, particularly outside the United States, though growth remains above trend and the economic outlook is still healthy. Economic frictions between the United States and Europe eased (for now) following a face-to-face meeting between European Commission President Jean-Claude Juncker and US President Donald Trump, after which they announced intentions for the two economic powerhouses to work together to promote freer and fairer trade practices worldwide. On the other hand, the ongoing trade dispute between the United States and China continued to deteriorate. Meanwhile, the last few trading days of July witnessed sharp declines in some popular internet stocks (e.g., Facebook and Netflix, part of the so-called “FAANG” group of dominant US-listed technology companies)—whose secular growth stories may have been increasingly used by investors as shelter from the gathering trade storms—following the release of disappointing earnings results and forward guidance. Facebook’s Chinese equivalent, Tencent, the largest stock in the MSCI Emerging Markets Index, similarly struggled in July and, like Facebook, is currently trading more than 20% below its peak market value. Yet, despite more negative than positive headlines, global risk assets generally marched higher last month as second quarter continued the run of strong corporate results observed over the past two years.

TOTAL RETURN FOR MSCI INDEXES (%)

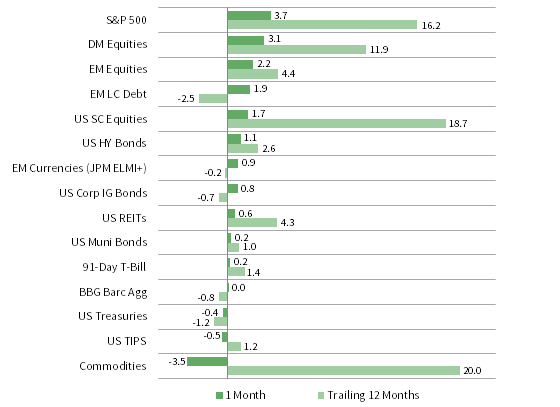

US equities (3.7% for the S&P 500 Index) advanced and outperformed developed counterparts as economic and corporate results continued to outshine those of the other major regions, and trade tensions with Europe appeared to subside for now. Small caps, perceived to be more insulated from a trade war scenario, underperformed large caps following four consecutive months of outperformance. All 11 S&P 500 sectors were in the black for the month, led by industrials, health care, and financials, while real estate, energy, and consumer discretionary delivered the lowest returns. Second quarter earnings results were robust, with quarterly year-over-year earnings growth running at nearly 24% based on about three-quarters of companies having reported. Highlighting underlying economic strength, revenues are expected to grow about 10%. The initial GDP estimate showed the US economy expanding at a 4.1% annualized rate in second quarter, which marks the highest growth since third quarter 2014. Consumer spending, net trade, and business investment were the primary drivers of the strong GDP print; surging exports contributed just over 1 percentage point, likely the result of businesses attempting to get ahead of tariff implementation. Residential fixed investment and inventories were a drag on growth, the former pointing to a slowdown in the US housing market. Consumer and industrial inflation ticked up in June, and the labor market continued to show job and wage gains, including a higher labor force participation rate, all leading the US Federal Reserve to reaffirm its gradual pace of rate hikes and to emphasize a monetary policy shifting away from post-crisis accommodation.

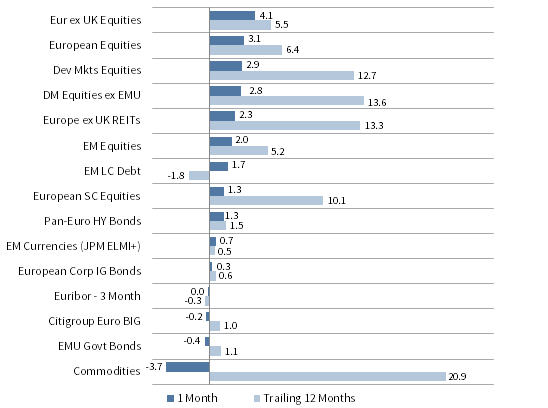

European equities (3.3% in USD, 3.1% in EUR, and 3.9% in GBP) outperformed developed markets peers as trade tensions with the United States appeared to abate for now. Europe ex UK and EMU stocks outgained UK counterparts, which became mired again in Brexit uncertainty. Although still early in the season, second quarter earnings from European corporates are growing in the low double digits, aided by diminishing currency headwinds. However, the economic backdrop appears less rosy, as second quarter GDP in the Eurozone disappointed, indicating the region grew at the slowest rate in two years. Additionally, the European Commission downgraded euro area growth expectations for 2018 from 2.3% to 2.1%, citing trade tensions and higher energy prices. The Eurozone’s composite purchasing manager index (PMI) came down slightly in July but remains squarely in growth territory; however, PMI data out of Germany improved. Markets rallied following Jean-Claude Juncker’s meeting with the Trump administration, following which the EU and United States announced tentative plans to improve trade relations by moving toward zero tariffs or trade barriers on non-auto industrial goods and by working together to reform the WTO. The European Central Bank (ECB) left rates unchanged and reaffirmed its Asset Purchase Program wind-down by year end, also signaling it will not raise rates until at least summer 2019. In the United Kingdom, Brexit secretary David Davis and foreign secretary Boris Johnson resigned from Prime Minister Theresa May’s cabinet (after its annual Chequers retreat) in formal protest of the planned publication of the government’s “Brexit White Paper,” which, in the former Brexit leaders’ view, makes too many concessions to the EU.

Japanese equity gains (0.4% in USD, 0.2% in EUR, and 1.0% in GBP) were relatively muted and underperformed developed markets peers as the yen broadly depreciated. Calendar second quarter earnings are up 10% year-over-year, the slowest rate since third quarter 2016 (though the reporting season remains in its early stages). In a counter to the recent rise in global trade protectionism, Japan struck a free trade deal with the EU in an agreement that covers nearly a third of the global economy. The pact cuts duties on products and gradually reduces auto tariffs, while also bringing Japan into compliance with the EU’s new data laws. The pact did not help business sentiment, which fell in July due to trade tensions with the United States. In fact, Japanese exports to the United States fell in June for the first time in 17 months, mostly due to lower exports of cars and semiconductor equipment. The Bank of Japan kept its monetary stimulus package largely unchanged at its July meeting, despite market speculation that the central bank would follow the Fed and ECB in dialing back accommodative policy. Inflation remains weak, and signs point to a continued growth moderation after a strong run over the prior two years.

Emerging markets equities (2.2% in USD, 2.0% in EUR, and 2.9% in GBP) bounced back last month but underperformed developed markets counterparts as 2018’s US dollar rally paused. Among emerging regions, Latin America and emerging Europe, the Middle East & Africa outperformed, while emerging Asia lagged the broader index. Index heavyweight China was the notable detractor and declined about two percent or more in major currency terms. Trade tensions mounted as the United States formally implemented tariffs on $34 billion worth of Chinese goods, to which China retaliated in kind; the Trump administration then signaled that tariffs on the entire roughly $500 billion of Chinese imports were on the table. Calendar second quarter GDP pointed to a moderate slowdown in the Chinese economy, and later data indicated a slowing of business activities and household consumption. In response to trade and economic worries and counter to the recent deleveraging initiative, Chinese authorities cut the reserve requirement ratio for domestic banks and introduced a fiscal stimulus package, allowing the renminbi to weaken in response. Declines by some of the once high-flying Chinese technology stocks also weighed on emerging markets equities amid signs of slowing growth. As an example, internet giant Tencent has lost nearly $150 billion in market valuation since peaking in January. Among the other large emerging markets, Brazil and India rallied, with local indexes in the latter setting multiple new highs during the month. Turkish stocks fell sharply in major currency terms as the central bank surprised the market by leaving rates unchanged despite spiking inflation, which caused the lira to plummet. Frontier markets stocks (3.7% in USD, 3.4% in EUR, and 4.3% in GBP) rebounded but remain down year-to-date.

Real assets performance was mixed in July. Commodity futures (-2.1% for the Bloomberg Commodity TR Index and -3.5% for the energy-heavy S&P GSCI™ Index) retreated despite a pause in the US dollar rally, led lower by industrial metals and energy. Crude oil prices ($74.25 for Brent and $68.76 for WTI) sank over six percent as Libya regained control over export terminals. Markets also seemed to react to the potential for US emergency stockpiles to be released (to counter any move by Iran to disrupt crude shipments through the Strait of Hormuz in response to renewed US sanctions). Energy MLPs (6.6%) and natural resource equities (1.0% for the MSCI World Natural Resources Index in USD terms) advanced on strong earnings results despite underlying commodity weakness. Developed markets REITs (0.9% in USD terms) continued to rally in the face of higher bond yields; Europe ex UK REITs (2.3%) outperformed both US REITs (0.6%) and UK REITs (-0.6%). Gold prices (-2.3%) fell in USD terms to $1,222.01 as some trade tensions eased and data confirmed there are several pockets of economic strength around the globe.

Global fixed income returns were also mixed last month; developed markets government bonds declined, while corporate bonds and emerging markets debt advanced. US Treasuries (-0.4%) declined as yields were mostly range-bound but rose late in the month on stronger economic growth and an increase in Treasury issuance. The benchmark ten-year versus two-year yield spread fell to 29 basis points (bps) by month end as Federal Reserve minutes and Chair Powell’s congressional testimony affirmed the steady upward path for rates. Notably, the three-month Treasury bill yield rose above 2% last month for the first time since 2008 and now exceeds the S&P 500 dividend yield, the first such occurrence since 2007. Five- and ten-year Treasury yields climbed 12 bps and 11 bps to end at 2.85% and 2.96%, respectively. Likewise, UK gilts (-0.4%) saw five- and ten-year yields back up 6 bps and 5 bps to end at 1.02% and 1.44%, respectively. EMU government bonds (-0.4%) delivered similar results. US credit spreads tightened last month as US high-yield bonds (1.1%) and US corporate investment-grade bonds (0.8%) outperformed Treasuries. US tax-exempt bonds (0.2%) also outgained taxable equivalents, while US TIPS (-0.5%) were the worst-performing US fixed income category. UK linkers (0.5%) outperformed nominal gilts (-0.4%), in contrast to the United States.

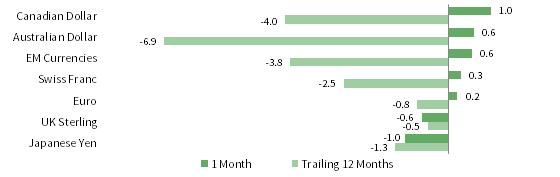

The US dollar and the UK sterling were generally weaker in July, while euro performance was mixed. July also marked a notable turnaround in the Canadian and Australian dollars and the Swiss franc, which all gained relative to the three major currencies we track, as did an equal-weighted basket of EM currencies. The US dollar depreciated against the Canadian and Australian dollars, EM currencies, the Swiss franc, and the euro, but gained relative to the UK sterling and the Japanese yen. The greenback is now broadly positive over the trailing 12 months. The euro fell against the Canadian and Australian dollars, the EM currency basket, and the Swiss franc, but gained against the Japanese yen, UK sterling, and US dollar. The UK sterling weakened against all but the Japanese yen, depreciating the most against the Australian and Canadian dollars and EM currencies, as UK inflation and retail sales came in lower than expected. Still, the Bank of England raised rates shortly after month end, as expected.

Currency Performance as of July 31, 2018

The US dollar mostly weakened in July, depreciating against the Canadian and Australian dollars, an equal-weighted EM currency basket, the Swiss franc, and the euro, but gaining relative to the UK sterling and Japanese yen. The US dollar broadly gained for the trailing 12 months, particularly against commodity-exposed and EM currencies.

VERSUS THE US DOLLAR

Total Return (%)

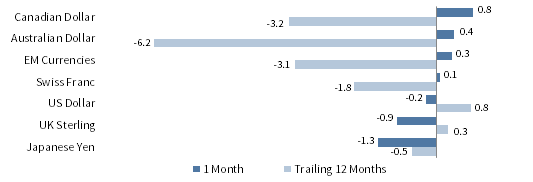

Euro performance was mixed last month. The common currency gained against the Japanese yen, UK sterling, and US dollar, but fell relative to the Canadian and Australian dollars, EM currencies, and Swiss franc. The euro was mostly stronger over the trailing 12 months, except against the US dollar and the UK sterling.

VERSUS THE EURO

Total Return (%)

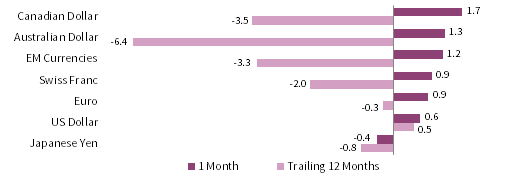

Amid heightened Brexit uncertainty, as well as lower-than-expected inflation and retail sailes, the UK sterling depreciated against all but the Japanese yen in July; the Bank of England still raised rates shortly after month end, as expected. Over the trailing 12 months, in contrast, the UK sterling strengthened against all but the US dollar.

VERSUS THE POUND STERLING

Total Return (%)

Note: EM currencies is an equal-weighted basket of 20 currencies.

USD Market Performance as of July 31, 2018

Equities advanced amid strong corporate and economic results, particularly in the United States, as US equities outperformed DM peers. EM assets rebounded on a reprieve from USD strength. Corporate credit spreads tightened as HY bonds outgained IG equivalents, and US Treasuries fell. Commodities saw the greatest decline.

INDEX PERFORMANCE (US$)

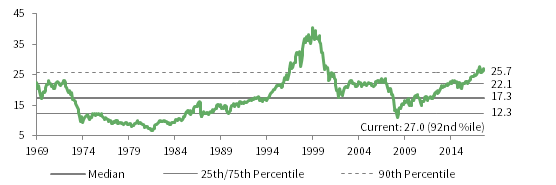

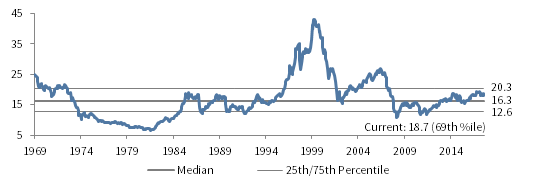

COMPOSITE NORMALIZED P/E: MSCI US

December 31, 1969 – July 31, 2018

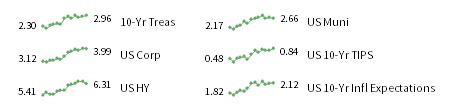

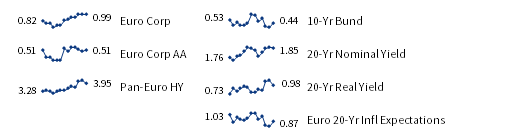

FIXED INCOME YIELDS

July 2017 – July 2018

Sources: Barclays, Bloomberg L.P., BofA Merill Lynch, FTSE International Limited, Frank Russell Company, J.P. Morgan Securities, Inc., MSCI Inc., National Association of Real Estate Investment Trusts, Standard & Poor’s, and Thomson Reuters Datastream. MSCI data provided “as is” without any express or implied warranties.

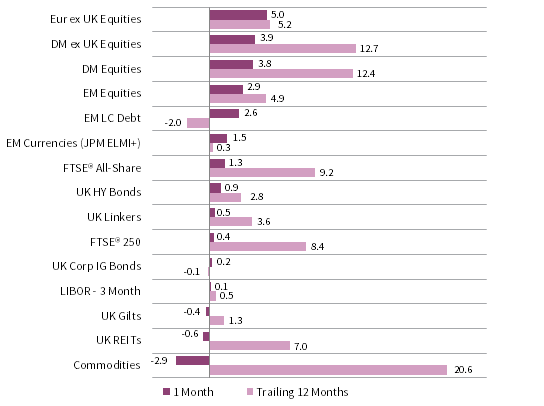

Euro Market Performance as of July 31, 2018

Equities gained across the board; Europe ex UK outperformed broader European and DM stocks, which outgained EM counterparts, while European small caps lagged. EM debt led fixed income returns, followed by Pan-Euro HY bonds, while Eurozone IG fixed income slightly declined. Commodities posted a sharp loss.

INDEX PERFORMANCE (€)

COMPOSITE NORMALIZED P/E: MSCI EUROPE EX UK

December 31, 1969 – July 31, 2018

FIXED INCOME YIELDS

July 2017 – July 2018

Sources: Barclays, Bloomberg L.P., Citigroup Global Markets, EPRA, FTSE International Limited, J.P. Morgan Securities, Inc., MSCI Inc., National Association of Real Estate Investment Trusts, Standard & Poor’s, and Thomson Reuters Datastream. MSCI data provided “as is” without any express or implied warranties.

GBP Market Performance as of July 31, 2018

Equities led performance in July, paced by Europe ex UK stocks, while UK equivalents lagged. EM equities and bonds bounced back and UK HY bonds outgained corporate IG counterparts. UK gilts and UK REITs slightly retreated, and commodities fell following a strong run in first half 2018.

INDEX PERFORMANCE (₤)

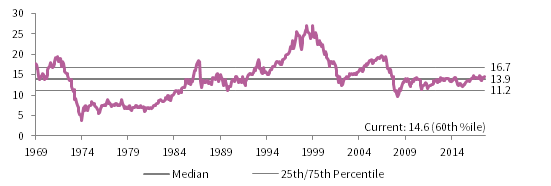

COMPOSITE NORMALIZED P/E: MSCI UK

December 31, 1969 – July 31, 2018

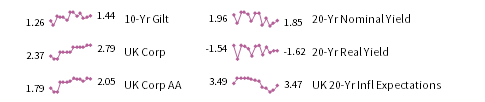

FIXED INCOME YIELDS

July 2017 – July 2018

Sources: Barclays, Bloomberg L.P., BofA Merill Lynch, EPRA, FTSE International Limited, J.P. Morgan Securities, Inc., MSCI Inc., National Association of Real Estate Investment Trusts, Standard & Poor’s, and Thomson Reuters Datastream. MSCI data provided “as is” without any express or implied warranties.

Exhibit Notes

Performance Exhibits

Total return data for all MSCI indexes are net of dividend taxes.

US dollar index performance chart includes performance for the Bloomberg Barclays Aggregate Bond, Bloomberg Barclays Corporate Investment Grade, Bloomberg Barclays High-Yield Bond, Bloomberg Barclays Municipal Bond, Bloomberg Barclays US TIPS, Bloomberg Barclays US Treasuries, BofA Merrill Lynch 91-Day Treasury Bills, FTSE® NAREIT All Equity REITs, J.P. Morgan ELMI+, J.P. Morgan GBI-EM Global Diversified, MSCI Emerging Markets, MSCI World, Russell 2000®, S&P 500, and S&P GSCI™ indexes.

Euro index performance chart includes performance for the Bloomberg Barclays Euro-Aggregate: Corporate, Bloomberg Barclays Pan-Euro High Yield, Citigroup EMU Govt Bonds, Citigroup Euro Broad Investment-Grade Bonds, Euribor 3-month, FTSE® EPRA/NAREIT Europe ex UK, J.P. Morgan ELMI+, J.P. Morgan GBI-EM Global Diversified, MSCI Emerging Markets, MSCI Europe, MSCI Europe ex UK, MSCI Europe Small-Cap, MSCI World ex EMU, MSCI World, and S&P GSCI™ indexes.

UK sterling index performance chart includes performance for the Bloomberg Barclays Sterling Aggregate: Corporate Bond, BofA Merrill Lynch Sterling High Yield, FTSE® 250, FTSE® All-Share, FTSE® British Government All Stocks, FTSE® British Government Index-Linked All Stocks, FTSE® EPRA/NAREIT UK RE, J.P. Morgan ELMI+, J.P. Morgan GBI-EM Global Diversified, LIBOR 3M GBP, MSCI Emerging Markets, MSCI Europe ex UK, MSCI World, MSCI World ex UK, and S&P GSCI™ indexes.

Valuation Exhibits

The composite normalized P/E ratio is calculated by dividing the inflation-adjusted index price by the simple average of three normalized earnings metrics: ten-year average real earnings (i.e., Shiller earnings), trend-line earnings, and return on equity–adjusted earnings. We have removed the bubble years 1998–2000 from our mean and standard deviation calculations. All data are monthly.

Fixed Income Yields

US fixed income yields reflect Bloomberg Barclays Municipal Bond Index, Bloomberg Barclays US Corporate High Yield Bond Index, Bloomberg Barclays US Corporate Investment-Grade Bond Index, and the ten-year Treasury.

European fixed income yields reflect the BofA Merrill Lynch Euro Corporate AA Bond Index, BofA Merrill Lynch Euro Corporate Bond Index, Bloomberg Barclays Pan-European Aggregate High Yield Bond Index, Bloomberg Twenty-Year European Government Bond Index (nominal), ten-year German bund, 20-year European Inflation Swaps (inflation expectations), and the real yield calculated as the difference between the inflation expectation and nominal yield.

UK sterling fixed income yields reflect the BofA Merrill Lynch Sterling Corporate AA Bond Index, BofA Merrill Lynch Sterling Corporate Bond Index, UK ten-year gilts, Bank of England 20-year nominal yields, and Bloomberg Generic UK 20-year inflation-linked (real) yields. Current UK 20-yr nominal yield data are as of July 30, 2018.