- SEC adopts money market fund rule reforms

- Definitional changes increase pricing for some credit default swaps

- Revised regulations broaden the classification of commodity pool operators

- Private equity funds’ treatment of fees and expenses remains on the SEC’s radar

US Money Market Fund Reform

Not the good news you hoped for

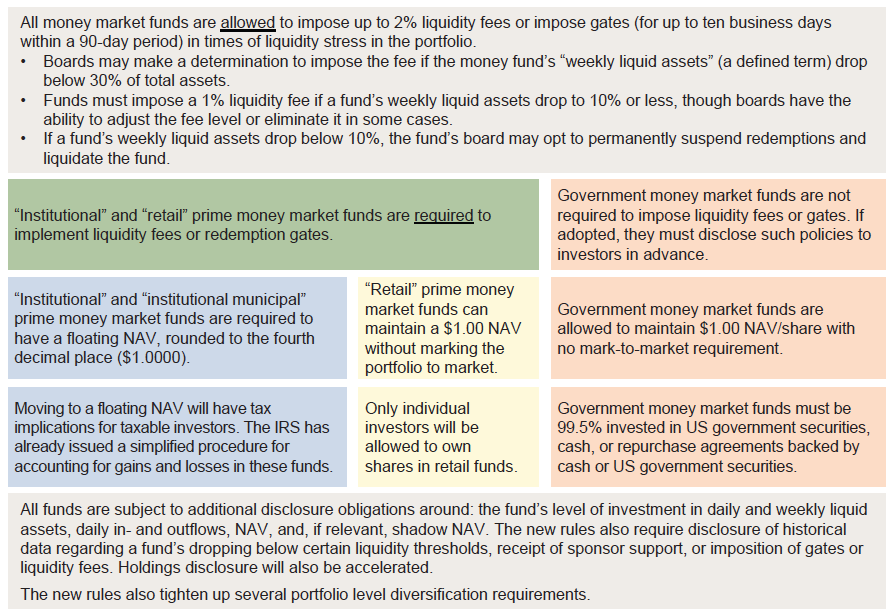

After several years of tussles among various regulators, investors, and managers, and after receiving more than 1,400 comments on its proposal, the SEC adopted amendments to money market fund (MMF) rules that promise to have a significant impact on these investment vehicles. Although the major reform requirements are close to two years away, managers are already preparing for the changes that significantly decrease institutional investor flexibility. The new MMF regulations reflect regulators’ focus on fighting systemic risk—a mandate that may prove to be just a frustrating game of “whack-a-mole” for those given this task.

What happened? In the United States, MMFs maintain stable net asset values of $1.00 per share through the use of amortized cost pricing. This approach came under fire after 2008 when a very large prime[1]Prime funds can own commercial paper, bank CDs, and other securities. MMF, Reserve Primary Fund, “broke the buck” and sent investors in prime funds across the industry scrambling for the exits.[2]According to an SEC staff report, investors withdrew nearly $500 billion in a roughly one-month period from prime MMFs during September–October 2008. In the same report, regulators highlighted a … Continue reading While the US financial regulatory approach has generally been to allow institutional investors more flexibility than their retail counterparts, the MMF amendments take the opposite tack. This reflects the SEC’s concerns that institutional investors are more likely to institute destabilizing “runs on the fund” than are retail investors.

Under the new MMF rules, institutional prime money funds will be required to maintain a floating net asset value (NAV) going forward. They are also subject to requirements to consider imposing gates or redemption fees on investors if their liquidity positioning declines. In contrast, retail prime MMFs will be permitted to continue to maintain a $1.00 per share NAV and have no gating or redemption fee requirements (Figure 1).

Figure 1. Summary of Select US Money Market Fund Amendments

Note: Most changes are subject to a two-year transition period.

For more thoughts on the investment implications of MMF reforms, please see Stephen Saint-Leger, “How Should Investors Respond to the SEC’s New Regulations Governing Money Market Funds?,” C|A Answers, August 5, 2014.

For more on recent changes to the securities lending industry and lending program management, please see Mary Cove et al., “Securities Lending: What a Difference Five Years Makes,” Cambridge Associates Research Report, 2013.

While these changes may meet regulatory objectives for reducing systemic risk, they limit investor choice in an already unattractive asset class. For large investors seeking a stable NAV product, government MMFs will become the registered fund option in the United States. In addition, these changes to MMF structure are already impacting areas including securities lending. In our conversations with market participants, lending agents are preparing for the time when prime MMFs must shift to floating NAV and add gating provisions. These attributes are incompatible with the needs of securities lenders seeking a liquid home for reinvested collateral. For now at least, lenders may need to move to government MMFs, a shift that will further erode already meager returns on collateral reinvestment and solidify lenders’ current preference for “value” approaches to lending.

Outside of the United States, a European proposal to address MMF risks stalled earlier this year. An eye-watering aspect of the proposal: European regulators sought to require stable NAV funds to hold a 3% capital buffer. In an environment characterized by virtually no return on MMF investments, 3% is a tall order. The European proposal was a bit of a surprise to market participants. It was initially expected that rules for the just under $1 trillion European MMF business would be parallel to the US regulatory regime (which governs more than $2.5 trillion in money fund assets), consistent with regulators’ desire to reduce regulatory arbitrage. With the US rules now finalized and European authorities expected to revisit MMF proposals later this year, MMF rules in the two regions could come into alignment.

Costs Are Rising

More changes in the swaps market

In early October, some credit derivatives began trading under a series of new definitions, and the changes may result in substantially higher prices for credit default swaps (CDS) associated with some securities, such as subordinated bank bonds. The definitional changes, issued by International Swaps and Derivatives Association, Inc. (ISDA), are the first major overhaul to these rules of the road since 2003. The new ISDA definitions reflect attempts to learn from recent sovereign debt crises and bank rescues that have sometimes left CDS holders out in the cold. The 2014 definitions also make changes that should help improve the liquidity of the CDS market by identifying the specific obligation that market participants can use to meet swap obligations.

One class of changes to credit derivatives under the 2014 definitions is to expand the types of actions that are treated as “credit events,” thereby triggering a payment under the contract. In fact, the 2014 definitions create a new class of credit event for financial institutions: a “government intervention.”[3]Interestingly, government intervention credit events may only apply to financials in Asia (including Japan), Australia, New Zealand, and Western Europe. These new terms don’t apply to emerging … Continue reading This recognizes as credit events government announcements or actions against a financial institution that result in a reduction of principal on the reference obligation, subordination of the reference debt, or mandatory transfers or conversions. The ISDA definitions also allow for the possibility of a credit event occurring in subordinated debt of a financial institution without simultaneously triggering an event in the senior debt. Taken together, these changes are intended to reflect the economic realities of continued government intervention in the financials sector.

ISDA also attempted to address some of the issues and concerns raised during the Greek debt crisis. When Greece announced a massive restructuring of its debt in 2012, it required holders to exchange outstanding debt for newly issued debt with lower face value and on less attractive terms. Under the 2014 definitions, ISDA establishes a protocol for settling obligations under a swap when the reference obligations have been expropriated or exchanged for paper that would not be eligible to be delivered under the existing swaps contracts. This update also provides that a member country exiting the euro will not automatically trigger a credit event, another concern raised periodically as the Eurozone saga unfolds.

In a bid to improve the liquidity and functioning of the swaps market, ISDA also established a form of standardization for commonly traded swaps. While counterparties may still independently designate a reference instrument for a swap, ISDA will be listing so-called standard reference obligations (SROs) for widely used swaps. SROs will be chosen by ISDA and will be the reference obligation for a particular entity within the designated part of a capital structure (e.g., senior obligation). Unless parties opt out of the SRO approach within a trade, it will be assumed that a swap is referencing the SRO for a particular credit.[4]Markit posts a list of designated SROs.

While all of these definitional changes are intended to improve the swaps market, they have also caused prices to rise in some swaps as those subject to the new definitions effectively cover a broader range of credit events than under the previous regime (and thus may be more valuable, in the same way that a property insurance policy that only covers “named perils”—specifically enumerated events such as fire and hail—is cheaper than a policy covering against damage from any cause). In discussions we have had with managers, some experienced significant increases in costs as these changes moved toward their final implementation dates. Additionally, counterparties had the ability to “opt in” to the new definitions on existing swaps. For affected swaps that are still subject to 2003 definitions, the disconnect between these instruments and others trading in the marketplace under the new definitions could lead to increased basis risk.[5]Basis risk arises when returns from a hedging instrument do not perfectly counteract the negative outcome that the investor attempted to hedge.

Are You Running a Commodity Pool?

Tread carefully if you are managing assets for multiple beneficial owners

In 2012 the US Commodities and Futures Trading Commission (CFTC) issued revised regulations that have had a big impact on determining which entities are commodity pool operators (CPOs). And it turns out that you could be one of them.

Historically, private funds were largely exempt under CFTC rules. However, two changes broadened the CFTC’s reach considerably. First, the CFTC eliminated a widely used exemption from registration for institutional funds. Second, as required by the post-crisis Dodd-Frank Act, CFTC expanded its definition of “commodity interest” to include swaps. Historically, managers of private funds (including hedge funds) that invested in futures or other derivatives and that were sold only to institutional investors were exempted from registration as CPOs. One theme of the Dodd-Frank Act is to require more disclosure from private funds. Consistent with that, CFTC eliminated the “institutional fund” exemption from registration.

One lingering concern is whether a non-profit or other investor that pools its assets will be treated as a CPO. In a “no-action” letter issued earlier this year and as highlighted in a recent Wall Street Journal article,[6]“Is Your Charity a Commodities Trader?” The Wall Street Journal, October 3, 2014. Text of the CFTC no-action letter is available at: … Continue reading the CFTC addressed questions about the status of a non-profit entity seeking to pool the investments of its retirement plans and its endowments. The non-profit expected to invest some portion with managers engaged in commodity trading and requested CFTC guidance on its status.

How could the non-profit be a CPO? The CFTC registration requirement is driven by two facts: (1) establishing a pooled investment vehicle that has (2) commodity interest exposure. It is important to note that an investor can have a commodity interest exposure directly or through commingled vehicles. Given the expanded definitions described above, investments in hedge funds, commodity futures funds, and other strategies that employ derivatives may give investors commodity interest exposure. Typically, the issue could boil down to whether the investor is operating a “pool.” This tends to be a fact-intensive exercise and, depending on the complexity of the entity, may require legal advice. For example, institutions that take in assets of area non-profits or that otherwise commingle assets with different beneficiaries may possibly be considered “pools.”

If this sounds like you, take a closer look. CFTC registration is not a quick process and can involve some significant ongoing compliance requirements. There are several available exemptions from registration and other ways to address these concerns.

Private Equity Funds Under Fire

The SEC says they take too much in fees, but perhaps you thought that already …

For more information, please see Mary Cove, Quarterly Regulatory Update, Cambridge Associates, May 2014.

As we noted in our first quarter regulatory review, the SEC has been vocal about its interest in stepping up enforcement activities with private funds. Some of the concerns SEC staff highlighted earlier in the year are ones that we have heard about in the past, including concerns about fee and expense sharing and the use of related parties as service providers. In a speech earlier this year, the Director of the SEC’s Office of Compliance Inspections and Examinations noted that in more than half of examinations of private equity (PE) firms, the SEC has identified issues related to fees and expenses.[7]Speech by Andrew J. Bowden, Director Office of Compliance Inspections and Examinations (SEC) to Private Equity International (PEI) Private Fund Compliance Forum 2014, May 6, 2014. The speech provides … Continue reading The treatment of fees and expenses continues to get regulatory scrutiny as highlighted by a series of recent reports of SEC enforcement action and changes in PE firms’ approach to fees and conflicts.[8]As an example, in September Lincolnshire Management agreed to pay $2.3 million to settle SEC charges regarding the misallocation of expenses between two funds. See: … Continue reading Most PE firms have only been registered with the SEC since 2012 and the agency is making an effort to examine 25% of all newly registered firms by the end of this year.

What types of fees do PE firms charge beyond management fees and carried interest? Firms may charge transaction fees, advisory fees, monitoring fees, or directors’ fees to portfolio companies. In many cases, managers will offset a fund’s management fees with some or all of the fees received from underlying portfolio companies. Firms also vary in their approach to costs of using affiliated service providers and external consultants or other unaffiliated service providers. In some cases, the portfolio manager may cover these costs. In others, investors are on the hook.

What types of practices have been the SEC’s focus? One is the use of operating partners. Although most limited partnership agreements provide for transaction, advisory, and other fee offsets against the management fee, payments to operating partners are generally not treated in that manner. The SEC has highlighted situations in which an operating partner shifts from being a paid employee of the management company to an employee of a portfolio company (paid by the portfolio company) as concerning.

The practice of “accelerating” monitoring fees is another area of focus. In effect, this practice allows a PE manager to receive all fees due under a multi-year contract if a portfolio company is sold, goes public, or is divested. In some cases management firms share these fees with investors, but with increasing scrutiny, several large private investment firms have announced changes in their practices. Apollo Global Management, Blackstone Group, and TPG have all recently announced changes in their policies around accounting for monitoring fees.[9]Mark Maremont and Mike Spector, “Blackstone to Curb Controversial Fee Practice,” The Wall Street Journal, October 7, 2014. Interestingly, in most cases, firms will implement the changes on a going-forward basis without making changes to current investments. In a move that acknowledged regulators will continue to focus on conflicts, Blackstone Group recently announced that its advisory business would become a standalone firm.

Many PE firms do not take other fee income. Of those that do, practices range significantly. In our review of fund documents, most firms disclose which fees, if any, are subject to offset against fees charged to fund investors. While we have certainly seen a trend toward managers offsetting 100% of the fees they earn, some firms are simultaneously shifting other expenses from the management company to fund investors. In other cases, an affiliate of the manager may provide services that are not subject to an offset provision. The lack of a widely accepted standard of disclosure for affiliated entities and the fees they earn from funds or portfolio companies adds to the complexity of due diligence. Our approach is to engage the manager, seeking to understand the economics of the relationship and how the manager ensures that the fund is getting fair market value for services provided by affiliates. All of this points to the fact that PE investing remains labor intensive and requires engaging in a dialogue with managers about their fee and expense allocation practices.

While the SEC spotlight on this fee and expense issue has seemingly caused some changes in PE firm behavior, we view this as an area that will continue to be challenging for investors to fully evaluate. For funds that go through our complete due diligence process, we review managers’ policies regarding management fee offsets, expense allocations, and similar issues, seeking to ensure that the policies are appropriate and deal with conflicts of interest. However, as we described earlier, PE firms vary in their complexity and approach to these issues. As a result, any evaluation of a manager’s approach to the allocation of fees and expenses must be undertaken on a case-by-case basis.

Footnotes