In This Edition

- Potential for regulation of systemically important players in the asset management industry

- An update on the Volcker Rule and bank holdings of CLOs

- Fragmentation in the global swaps market

- Regulations for private equity and hedge funds

- FATCA’s first deadline, and what’s to come

Sometimes It’s Good Not To Be “Important”

Large US investment managers are pushing hard to avoid more intensive oversight

Coming out of the 2008 financial crisis, regulators vowed to place a more intensive focus on systemically important financial institutions (SIFIs). In the United States, the Dodd-Frank Wall Street Reform and Consumer Protection Act established a super-regulator, the Financial Stability Oversight Council (FSOC), which is responsible for monitoring systemic risks and identifying SIFIs. SIFIs are potentially subject to “enhanced prudential oversight” by the Federal Reserve and higher capital requirements. To date, most of the designated SIFIs in the United States are large bank holding companies. In 2013 the FSOC turned its attention to “nonbank” financial companies and began the process of identifying systemically important firms outside of the bank holding companies. The first non-bank financial companies designated SIFIs were AIG, GE Capital, and Prudential Financial.

More recently, and controversially, regulators have begun to focus on identifying systemically important players in the asset management industry. The identity of firms that might be in the crosshairs has been the subject of considerable speculation, but a report late last year by the US Treasury’s Office of Financial Research describing ways the asset management industry could contribute to systemic instability provided some clues. The asset management industry and even some commissioners at the Securities and Exchange Commission (SEC) criticized the report. However, prudential regulators have forged ahead in evaluating the systemic importance of asset managers and funds. Following a similar track, the Financial Stability Board and the International Organization of Securities Commissions have proposed focusing on funds with more than $100 billion in assets under management as potentially systemically important. US-based firms Blackrock, Fidelity, PIMCO, and Vanguard all manage funds that exceed the threshold.

Asset managers are pushing back vigorously with common lines of defense, including that large funds can act as shock absorbers within the financial system and that smaller funds employing high degrees of leverage may well pose greater risks to the system. Since regulators had bank holding companies in mind when developing the systemic risk rules, the impact of a SIFI designation on a bank holding company or insurance company seems comparatively straightforward. However, it is difficult to imagine how regulators would implement “enhanced prudential regulation” for a highly regulated investment fund, especially an index fund. This appears to reinforce the idea that there are limits to the benefits of scale, even in highly scalable investments. While the head of the Investment Company Institute, a US-based funds industry association, has noted that designating a fund as a SIFI would make it less compelling for investors, it would seem that asset managers could certainly restructure their way out of this problem.

Number of Large US Mutual Funds by Size

As of March 31, 2014

Source: Morningstar.

Have We Seen This Movie Before?

An update on the Volcker Rule and bank holdings of CLOs

Under the Volcker Rule, US banks cannot hold collateralized loan obligations (CLOs) that include both leveraged loans and debt or that contain manager removal rights. US bank holdings of CLOs are estimated to be $70 billion and by some estimates US and foreign banks hold close to two-thirds of all CLOs rated AAA.

In early April, the Fed took one step toward reducing the impact of the Volcker Rule on banks holding non-compliant CLOs, announcing that it would extend by two years (to July 21, 2017) the conformance period for debt holdings under the Volcker Rule. According to industry sources, most of the older CLOs held by banks should have matured by the mid-year 2017 date.

However, banks holding CLOs issued after 2009 would likely need to divest these holdings over the next several years. Trade association the Loan Syndications and Trading Association (LSTA) was quick to highlight an estimate from the Office of the Comptroller of the Currency that forced selling of CLO notes could cost US banks up to $3.6 billion.[1]See “LSTA Responds to Fed Announcement of Treatment of CLOs Under Volcker Rule,” LSTA News, April 7, 2014. This issue can still be resolved in a number of ways, from banks encouraging CLO managers to bring holdings into compliance with Volcker to further action by regulators. And, ever resourceful, recent reports suggest banks are lending to hedge funds and others to help finance purchases of CLOs in an effort to support a secondary market in the debt that they may no longer be able to hold. Have we seen this movie before?

Swaps Regulations

The specter of regulatory arbitrage and the future of the “package trade”

While both US regulators and their European counterparts are committed to developing a similar regulatory framework for the swaps market, they are not on the same implementation schedule. To date, the US Commodity Futures Trading Commission (CFTC) has led the way in implementing over-the-counter derivatives regulation. This includes requiring more market transparency through data reporting requirements and pushing users toward trading standardized swaps on electronic platforms. In fact, in February the CFTC authorized the first batch of swaps that were required to be traded on newly established swaps execution facilities (SEFs).

In contrast, first quarter marked the first swaps data reporting deadlines for EU-based swaps participants. Swaps are not expected to be subject to mandatory trading until at least 2016.

Hence the return of the “regulatory arbitrage” phrase. According to a report by the Wall Street Journal, US banks have been busy making structural changes to their swaps agreements to avoid US swaps regulation.[2]See “A Foreign Affair for U.S. Banks’ Swaps,” Wall Street Journal, April 28, 2014. In this case, banks have reportedly stepped away from having a US entity guarantee a swap between non-US bank affiliates and other non-US entities. According to some reports, regulators in other jurisdictions have noted that regulatory differences are causing the global swaps markets to become more fragmented, clearly not a long-term goal of financial regulators. Investors that have exposure to the swaps market should keep track of this trend. Regulatory-driven dislocations in the swaps markets have the potential to cause price distortions and may also result in market participants taking on a different range of counterparty risk than in the past.

As the CFTC approved the first swaps contracts for mandatory trading on SEFs, they also provided some limited-time relief (through May 15, 2014, with phase-in rules) for market participants that employ complex, multi-step “package” trades.[3]A “package trade” is a trade that involves several different trades executed simultaneously with a single counterparty and priced as a single deal. Examples include a “swap curve” (package of … Continue reading Without this relief, a manager employing a package trade that includes a swap subject to mandatory execution on a SEF would not be able to get one-stop execution in the United States. According to a statement by CFTC Commissioner Scott O’Malia earlier this year, the CFTC’s Chief Economist estimated that package trades compose 50% of the notional volume of the rates market.[4]“Statement of Commissioner Scott D. O’Malia on Made Available-to-Trade Determination,” January 16, 2014. For investors employing managers that use complex derivatives trades as part of their strategy, the resolution of this issue bears watching as it appears that package trades make up a significant portion of the volume of rates trades and that unbundling the trades could cause costs to skyrocket. By how much? Citadel LLC filed a comment letter with the CFTC estimating that trading costs for package trades could potentially triple for market participants. And there is the possibility of additional legging in risk when trades are individually executed as parts of a combined trade.

Notes on Alternatives

More SEC scrutiny, alternative mutual funds, and parental liability for private equity funds

SEC Scrutiny. With most institutional-sized hedge fund and private equity managers required to register with the SEC, it was only a matter of time before the SEC dedicated resources to examining its new charges. According to recent reports, the SEC has established a unit to focus on these alternatives managers. The unit is reportedly co-headed by individuals with direct private equity and hedge fund experience, which should help the group move up what could otherwise be a significant learning curve.

At its 2014 Compliance Outreach Program, the SEC identified several areas of concern with private funds and their practices. Some of these we have heard in the past, including concerns about fee and expense sharing and the use of related parties as service providers. In fact, in a recent speech, the Director of the SEC’s Office of Compliance Inspections and Examinations noted that in their examinations of private equity advisers’ fees and expenses, they have identified “violations of law or material weaknesses in controls over 50% of the time.[5]“Spreading Sunshine in Private Equity” speech by Andrew J. Bowden, Director, Offi ce of Compliance Inspections and Examinations (SEC), May 6, 2014. The speech details the SEC’s concerns … Continue reading ” Given the trend toward co-investing in private equity, investors might note SEC staff’s focus on potential favoritism, including in how firms allocate access to co-investment deals.[6]Allocations of costs associated with deal flow among commingled vehicles, separate accounts, and co-investments were another issue highlighted by SEC staff. With respect to hedge funds, valuations and use of expert networks remain on the list. SEC staff also highlighted information sharing among hedge fund managers (collaborating on ideas) as another area they are reviewing.

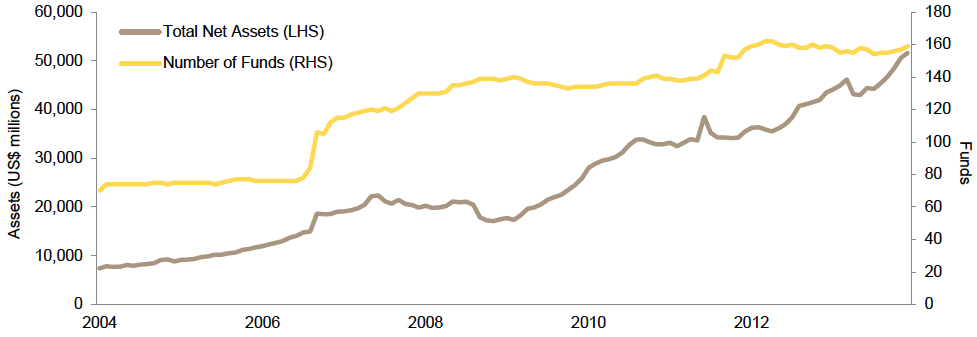

Alternative Mutual Funds. The SEC is taking a closer look at the practices of “alternative mutual funds.” The alternative mutual funds market is a fast-growing aggregation of many different types of funds and the SEC plans to focus on nontraditional bond strategies, long/short equity funds, multi-manager funds, and “market-neutral” funds. According to reports, the SEC plans to examine a small subset of funds over the summer and may follow up with further examinations of other funds in the segment. With this group of mutual funds growing rapidly and widely available to the investing public, it is no surprise that the regulator is taking a closer look at issues relating to liquidity, valuation, and use of leverage in the funds. The SEC staff has also noted their interest in ensuring that Boards of Directors who are responsible for the funds have enough knowledge to exercise appropriate oversight. For investors that can access traditionally structured funds, the “alternative” alternative funds would not be of interest. However, a growing number of managers are participating in this space and industry participants predict continued strong growth of these funds, albeit off a low base. Developments in the registered alternative mutual funds space bear watching as they have the potential to shift the business model for traditional hedge fund firms.

Alternative Mutual Funds: Total Net Assets and Number of Funds

February 29, 2004 – January 31, 2014

Source: Investment Company Institute.

Parental Liability for PE Funds. In a recent European Union case, the European Commission held a private equity manager (Goldman Sachs) liable for the anti-competitive behavior of a portfolio company (Prysmian). While this is not the first time that the Commission has looked through to a parent company in assessing fines for anti-competitive behavior, it may be a surprising result for US-based investors used to a high level of portfolio company liability protection provided at the fund level. It is for this reason that in the United States, private equity investors watched with interest last year’s Sun Capital[7]Sun Capital Partners III, LP et al v. New England Teamsters & Trucking Indus. Pension Fund, No. 12-2312, 2013 WL 3814984 (1st Cir. July 24, 2013). decision. In that case, the US Court of Appeals for the First Circuit held that a private equity fund may be jointly and severally liable for the unfunded pension obligations of its defunct portfolio company. In both of these cases, commentators point out that careful deal structuring could mitigate the potential for fund-level liability for portfolio company obligations.[8]With respect to the Sun Capital decision, see “Private Equity Funds Further Exposed to Portfolio Company Pension Plan Liabilities,” Client Alert News Flash, Latham & Watkins, Client Alert, … Continue reading This argues for continued vigilance in selecting managers.

FATCA Cometh

Though with yet another extension

The Foreign Account Tax and Compliance Act (FATCA) has been a long time in coming into effectiveness, having been enacted into law in 2010. May 5 marked the first deadline under the complex and controversial US tax compliance law. As a brief refresher, the purpose of FATCA is to reduce tax evasion by identifying and gathering information on US taxpayers that hold non-US accounts (i.e., that make investments through non-US entities). The way FATCA does this is by imposing a 30% withholding tax on any US-source payments (including gross proceeds, not just net gain) to a non-US entity that does not agree to comply with FATCA’s account identification, reporting, and withholding rules.

FATCA requires foreign financial institutions (FFIs) (unless they are subject to an exemption, this is tax law after all) to enter into an “FFI Agreement” with the IRS that requires:

- compliance with due diligence requirements intended to identify US account holders,

- annual reporting to the US Treasury on US accounts,

- compliance with other IRS information requests, and

- withholding payments to “recalcitrant” account holders.

FFIs that register with the IRS will receive an identification number, called a global intermediary identification number (GIIN), that provides proof of registration to withholding agents.

Privacy laws in some foreign jurisdictions that limit the ability of local financial institutions to share customer information with the IRS have added complexity to FATCA. As a solution, governments have entered into “intergovernmental agreements” (IGAs), which allow FFIs to either report information to their own tax authorities (Model 1 IGAs) or to the IRS (Model 2 IGAs) without running afoul of local law. Many jurisdictions that are common domiciles for offshore funds (British Virgin Islands and Cayman Islands, etc.) have entered into Model 1 IGAs with the IRS.[9]The Treasury maintains an updated list of jurisdictions with IGAs at www.treasury.gov/resource-center/tax-policy/treaties/Pages/FATCA-Archive.aspx.

While FATCA is intended to enforce US tax compliance, it can have a negative impact on investors that are themselves compliant. How? A non-compliant offshore domiciled fund is subject to the 30% withholding tax, which will diminish returns and, potentially, the capital of all investors, including investors that are themselves tax compliant. Managers we have spoken with over the last several years are very much aware of this law as the economic and reputational consequences of noncompliance could be significant.

FATCA is being rolled out over an extended period of time with the first major deadlines coming as of the end of this quarter—June 30, 2014. Some dates to keep in mind appear in the chart below.

FATCA Timeline

* Withholding is initially on “fixed or determinable, annual periodic income,” called “FDAP.”

In the near term, we expect that executing new investments in offshore funds might be a bit more complex as firms get used to new processes and paperwork designed to comply with FATCA. As usual, the best advice is to plan ahead! Existing investors may also receive documentation requests from managers over the second half of 2014 as firms begin to address the next level of due diligence requirements. As mentioned above, C|A’s business risk management team has been speaking with managers about their approach to FATCA compliance for several years. Our sense is that managers are very aware of the compliance challenges of FATCA and are anxious to get this right. We are also working to record and track firms’ self-reported FATCA status within our investment manager database. Given the complexities of FATCA compliance, it involves substantially more than a check-the-box exercise for us as well as for the managers themselves.

Finally, while the IRS has not granted the financial industry another wholesale deadline extension, they have softened FATCA’s blow a bit. In early May, the IRS announced that it will treat 2014 and 2015 as a transition period for purposes of IRS enforcement and administration of FATCA. This means that the IRS will grant market participants some relief from the brunt of a FATCA misstep if the entity has made “good faith efforts” to comply with the rules. In the same notice, the IRS granted FFIs some relief from the near-term FATCA due diligence and other requirements for new accounts opened between July 1, 2014, and January 1, 2015.

While FATCA is a US tax compliance regime, there are moves afoot to extend this type of reporting to taxpayers in other countries. A good example is the recent tax compliance agreement between the United Kingdom and Cayman Islands. This agreement is similar to US FATCA in that it seeks information from Cayman Islands–based financial institutions on accounts held by UK individuals and entities. Commentators have also noted that the Organisation for Economic Co-operation and Development is in the early stages of developing a proposal designed to establish an international standard for automatically sharing financial information between like-minded jurisdictions.

Footnotes